Why Bobtail Insurance Matters for Independent Truckers

Independent truckers face significant financial risks when driving without a trailer attached. Bobtail insurance provides essential protection during these vulnerable periods.

At Select Risk Insurance Group, we see too many owner-operators operating without this coverage, exposing themselves to devastating liability claims. The right policy protects your personal assets and business investment when primary liability coverage doesn’t apply.

What Does Bobtail Insurance Actually Cover

Bobtail insurance activates when you operate your truck without a trailer and your primary liability coverage stops protection. This happens frequently during transitions between loads, drives home after deliveries, or trips to pickup locations. Your motor carrier’s primary liability policy only covers you while under dispatch with freight. The moment you disconnect that trailer and drive for personal reasons or between assignments, you enter a coverage gap that bobtail insurance fills. The Federal Motor Carrier Safety Administration provides comprehensive crash statistics for large trucks and buses, which makes this coverage essential rather than optional.

Coverage Gaps That Cost Truckers Everything

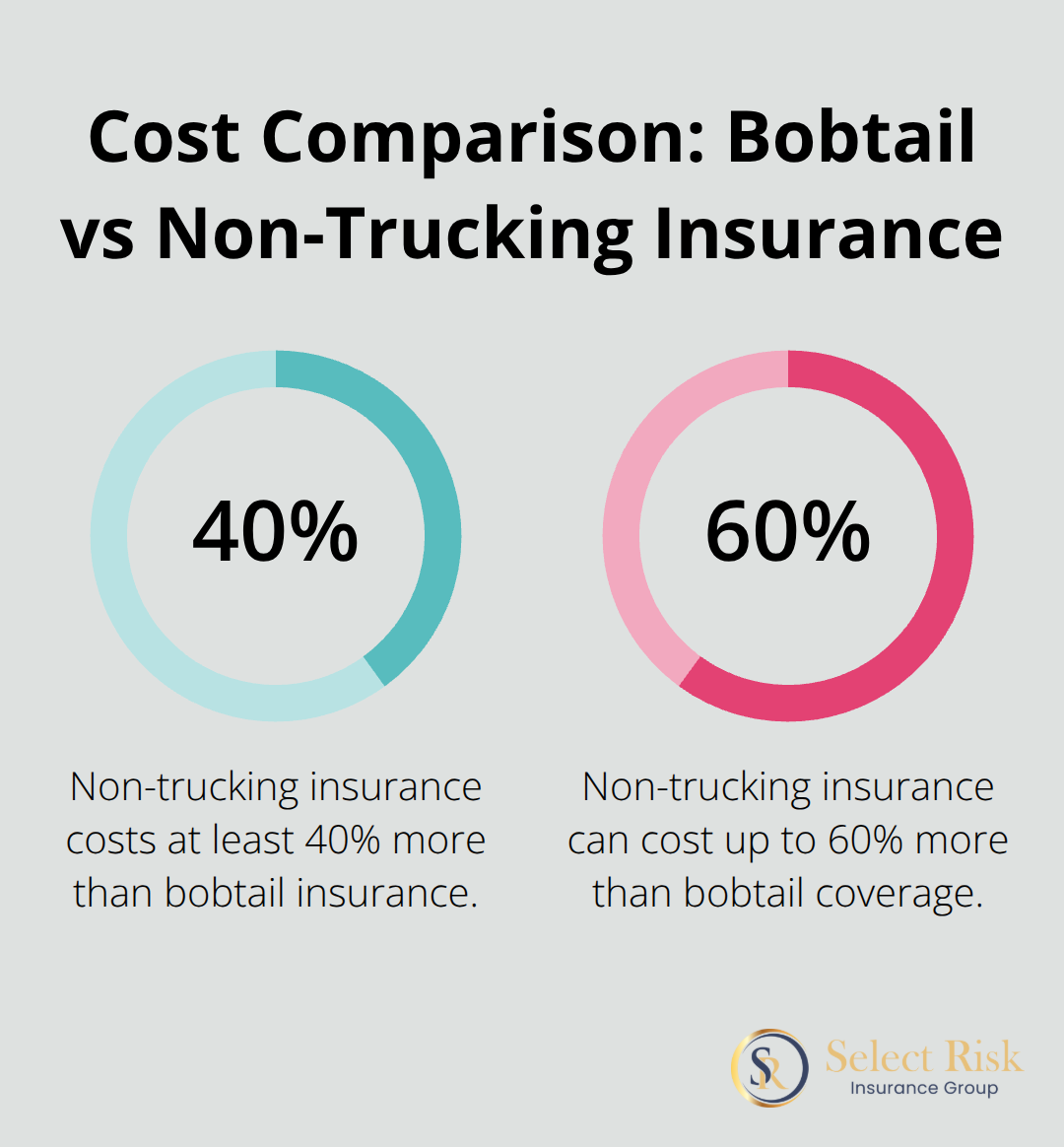

Deadhead insurance covers you when you pull an empty trailer under dispatch, while bobtail insurance protects you when no trailer attaches at all. Non-trucking liability insurance provides broader coverage for any personal use of your truck (whether a trailer attaches or not). This distinction matters because non-trucking policies cost 40-60% more than bobtail coverage but cover scenarios like weekend errands with your truck. Most independent truckers need bobtail insurance specifically because they rarely use their trucks for personal activities beyond drives home after work. The monthly cost difference between $35-40 for bobtail versus $60-80 for non-trucking insurance adds up to $300-500 annually.

State Requirements Vary Significantly

No federal law mandates bobtail insurance, but your motor carrier lease agreement almost certainly requires it. States like California and Texas have stricter enforcement of continuous liability coverage, which makes bobtail insurance practically mandatory for legal operation. Many carriers require $1 million in bobtail coverage as a lease condition, and operation without it can void your lease agreement immediately. We recommend you maintain this coverage level because legal settlements for serious accidents routinely exceed $500,000, and your personal assets become vulnerable without adequate protection.

Real Financial Impact Without Coverage

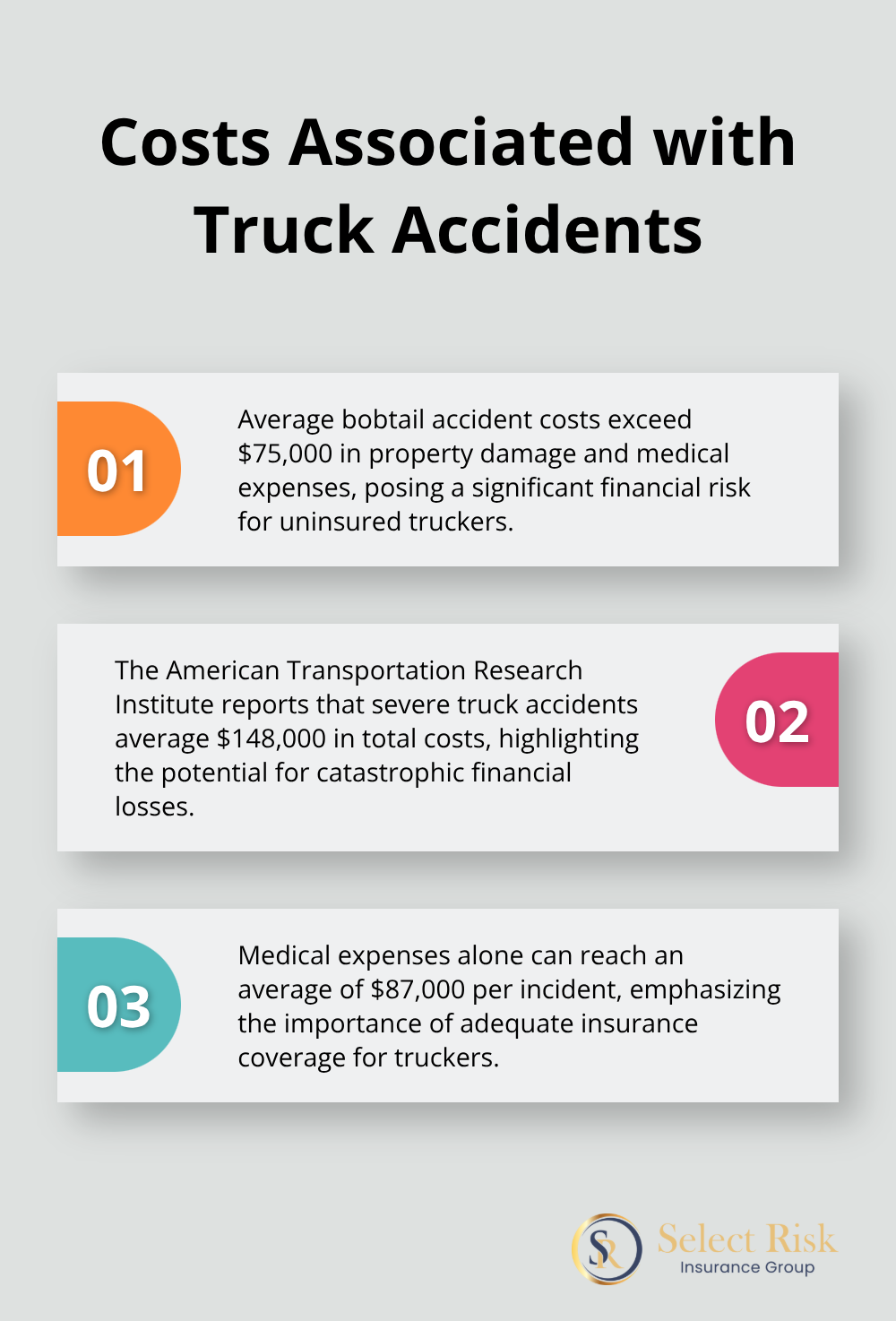

The average bobtail accident costs exceed $75,000 in property damage and medical expenses. Without proper coverage, these costs come directly from your personal assets and business savings. Independent truckers who operate without bobtail insurance face personal bankruptcy rates 3 times higher than those with adequate coverage. Your home, savings accounts, and business equipment all become targets for lawsuit settlements when you lack sufficient liability protection during bobtail operations.

What Do Accidents Really Cost Independent Truckers

Independent truckers without bobtail insurance face catastrophic financial exposure that extends far beyond vehicle repairs. The American Transportation Research Institute reports that severe truck accidents average $148,000 in total costs, with medical expenses alone reaching $87,000 per incident. When you operate without coverage and cause injury to multiple people, settlements frequently exceed $500,000.

Personal injury attorneys specifically target truckers because they know owner-operators often carry substantial personal assets (homes, savings, and equipment). Your personal net worth becomes the settlement pool when insurance coverage falls short.

Personal Assets Face Direct Legal Attack

Courts routinely award judgments that exceed $1 million against uninsured truckers who cause serious accidents. Your home equity, retirement accounts, business equipment, and future earnings all face seizure through legal proceedings. The National Safety Council documents that 4,965 large trucks were involved in fatal crashes during 2020, and surviving victims or families pursue aggressive legal action against drivers and their assets.

Independent truckers who operate without adequate bobtail coverage lose their homes in 23% of major liability cases according to trucking industry legal data. Bankruptcy becomes the only option for many owner-operators who face judgments that exceed their insurance limits.

Real Settlement Cases That End Careers

A 2019 case in Texas resulted in a $90 million judgment against an uninsured owner-operator who struck a family vehicle while bobtailing home after a delivery. The trucker lost his home, retirement savings, and had wages garnished for eight years. Another incident in Florida saw a $890,000 settlement when a bobtailing truck rear-ended a vehicle at a traffic light (causing permanent disabilities to the occupants).

These settlements demonstrate why $1 million in bobtail coverage represents the minimum acceptable protection level for serious independent truckers who want to preserve their financial future.

How Insurance Companies Calculate Your Risk

Insurance carriers evaluate multiple factors when they determine your bobtail insurance rates and coverage options. Your driving record, truck value, and operational patterns all influence premium calculations.

How Do You Choose the Right Bobtail Policy

Most independent truckers make costly mistakes when they select bobtail insurance because they focus only on monthly premiums instead of coverage quality and carrier reliability. Your coverage limits should start at $1 million minimum, though coverage amounts can go higher if you wish to purchase more liability. Deductible options typically range from $1,000 to $10,000, and a $2,500 deductible saves approximately 15-20% on annual premiums while it keeps out-of-pocket costs manageable for most truckers.

Carrier Financial Strength Matters More Than Price

Progressive Commercial and Great West Casualty dominate the bobtail insurance market with A+ financial ratings from AM Best, but their rates can differ by 30-40% for identical coverage. National General and CNA also offer competitive bobtail policies, though their approval processes take longer and require more documentation. Never choose a carrier with less than an A- rating regardless of price savings, because financially weak insurers delay claim payments and sometimes deny legitimate claims to preserve cash flow. The National Association of Insurance Commissioners tracks complaint ratios, and carriers with ratios above 1.5 generate significantly more customer disputes than industry averages.

Policy Features That Separate Winners from Disasters

Your bobtail policy should include automatic coverage extensions for emergency situations, 24-hour claim reports, and coverage for hired or borrowed trucks when your primary vehicle requires repairs. Avoid policies with restrictive geographic limitations or those that exclude coverage during specific weather conditions, because these restrictions often void coverage when you need protection most. The best policies provide coverage for towing and emergency roadside assistance (which saves $200-400 annually compared to separate service purchases). Monthly payment options cost 8-12% more annually than six-month premium payments, but the cash flow flexibility often justifies this expense for independent truckers who manage tight budgets.

Rate Comparison Strategies That Save Money

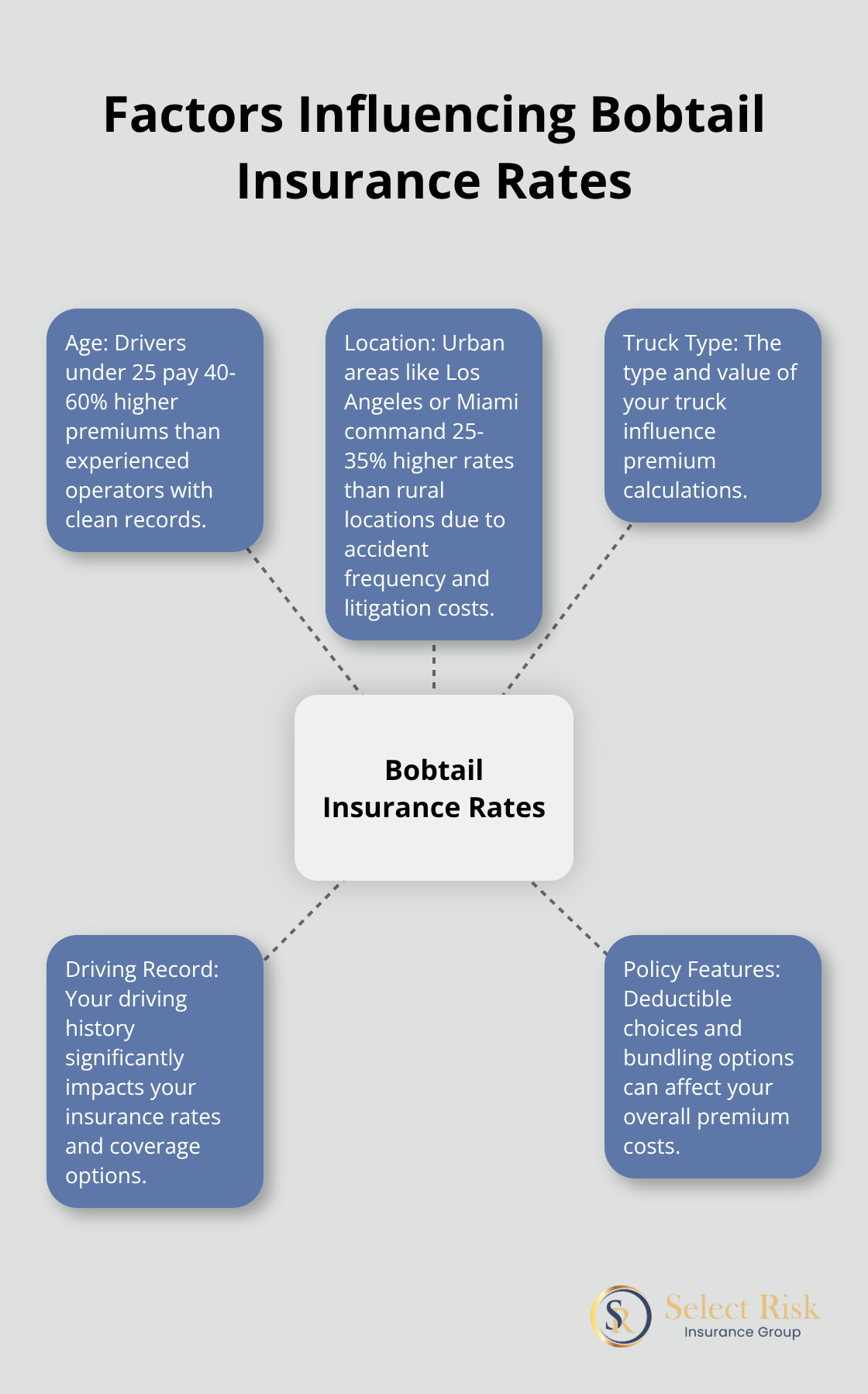

Shop quotes from at least five carriers because bobtail insurance rates vary dramatically between companies for identical coverage. Your age, location, and truck type influence premium calculations more than most truckers realize. Drivers under 25 pay 40-60% higher premiums than experienced operators with clean records. Urban areas like Los Angeles or Miami command 25-35% higher rates than rural locations due to accident frequency and litigation costs. Bundling bobtail coverage with your physical damage insurance often reduces total premiums by 10-15% compared to separate policies from different carriers.

Final Thoughts

Bobtail insurance represents the difference between financial survival and bankruptcy for independent truckers. This coverage protects your personal assets from devastating liability claims that destroy decades of hard work. Monthly costs of $35-40 provide protection worth hundreds of thousands of dollars when accidents occur during non-dispatch operations.

Multiple carriers offer different rates for identical coverage, so you must request quotes from at least five insurers. Focus on carriers with A- ratings or higher from AM Best to avoid claim payment delays. Compare coverage limits, deductibles, and policy features rather than price alone (because cheap policies often exclude critical protections).

Independent truckers who maintain adequate bobtail insurance build stronger relationships with carriers and qualify for better freight opportunities. This coverage maintains your ability to operate legally under motor carrier lease agreements and preserves business continuity when unexpected incidents occur. At Select Risk Insurance Group, we help Louisiana truckers navigate these complex insurance decisions through personalized service and access to multiple reputable carriers, so contact our team to compare options that protect your trucking business and personal assets.