Essential Insurance Coverages for Employed Truck Drivers

Employed truck drivers face unique insurance challenges that most people never consider. Company policies often leave significant gaps in protection.

We at Select Risk Insurance Group see drivers struggle with inadequate truck driver coverage daily. The right insurance strategy protects both your career and personal assets.

What Coverage Gaps Do Employed Drivers Face?

Company Insurance Limitations

Most trucking companies provide minimal coverage that meets federal requirements but exposes drivers to significant financial risks. The Federal Motor Carrier Safety Administration requires specific liability coverage amounts for interstate commerce, which increases for hazardous materials transport. These amounts prove insufficient when serious accidents occur, especially with rising medical costs and inflation that have outpaced federal insurance minimums since their establishment.

Company policies typically exclude coverage when drivers use their trucks for personal errands or operate without a trailer attached. This creates dangerous gaps during bobtail operations or personal use periods. Most employer-provided coverage does not extend to drivers’ personal vehicles or provide adequate medical coverage for work-related injuries beyond basic workers’ compensation requirements.

Personal Vehicle Coverage Challenges

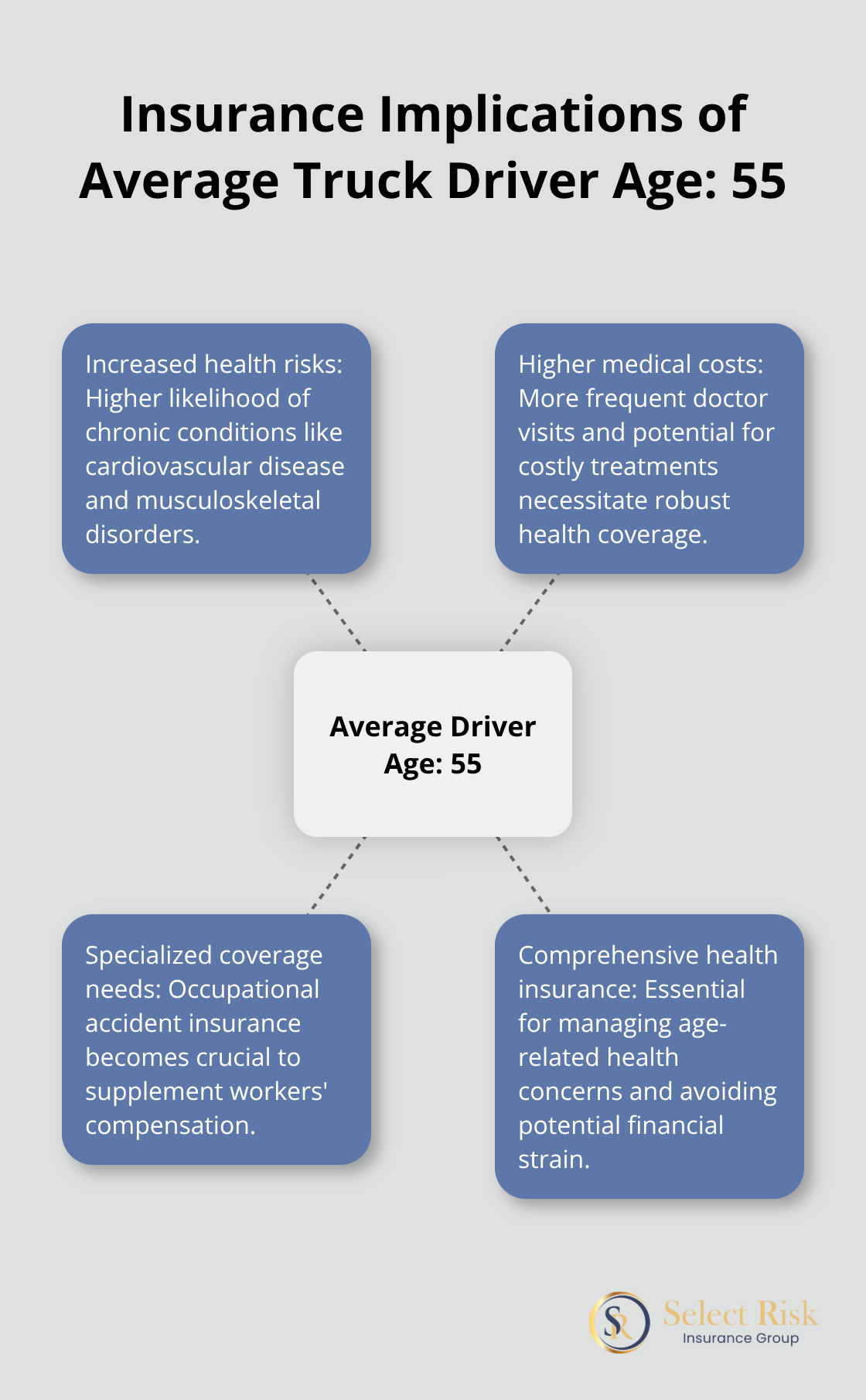

Employed drivers need personal auto insurance for their private vehicles, but standard policies often exclude commercial use entirely. Many drivers unknowingly violate their personal policy terms when they use personal vehicles for any work-related activities (including trips to terminals or paperwork handling). Personal injury protection becomes essential since company policies may not cover medical expenses adequately, and the average truck driver age of 55 years increases health insurance needs significantly.

State-Specific Requirements

State requirements vary dramatically, with some states demanding additional coverage beyond federal minimums. California and New Jersey impose tax penalties for lacking ACA-compliant health insurance, which affects drivers’ financial planning. Smart drivers secure comprehensive health insurance through marketplace plans or professional association groups, as the sedentary lifestyle and irregular hours increase risks of obesity, cardiovascular disease, and musculoskeletal disorders that require ongoing medical attention.

The gaps in standard coverage create a complex web of potential liabilities that employed drivers must address through strategic insurance planning. Understanding these vulnerabilities helps drivers identify which specific coverages they need to protect themselves comprehensively.

What Coverage Must Employed Drivers Secure Independently

Commercial Auto Liability Insurance

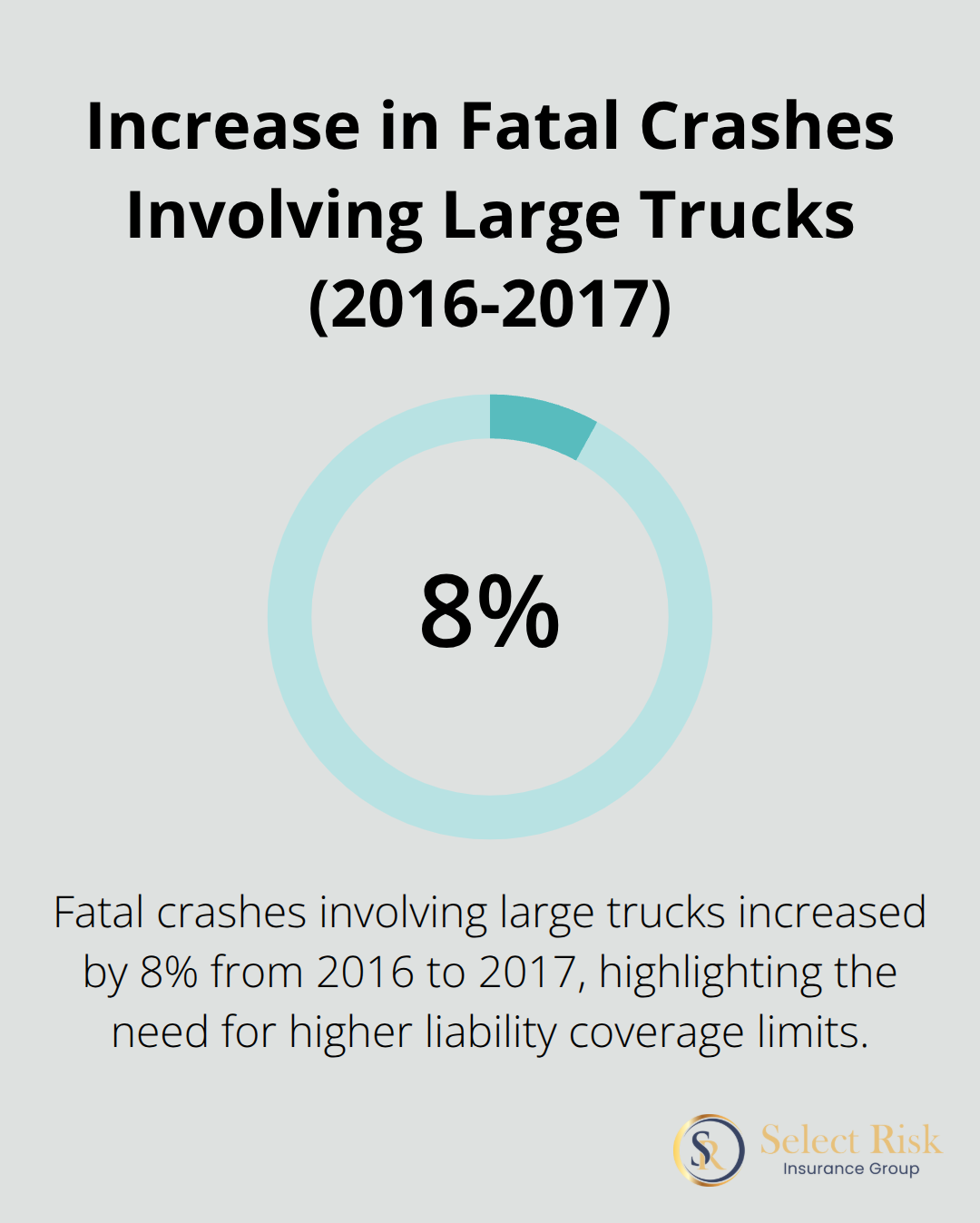

Federal minimums of $750,000 prove insufficient when serious accidents occur, with medical costs rising faster than required coverage amounts. Most trucking companies carry only minimum coverage, which leaves drivers personally liable for damages that exceed policy limits. Additional liability coverage through umbrella policies extends protection to $2 million or higher, especially important since fatal crashes involving large trucks increased by 8 percent from 2016 to 2017 according to federal safety data.

Smart employed truck drivers secure this coverage independently because company policies never provide adequate protection. The gap between federal requirements and actual accident costs continues to widen as medical expenses and property damage claims increase annually.

Physical Damage Coverage for Personal Vehicles

Standard auto policies exclude commercial use entirely, which creates problems for drivers who use personal vehicles for work-related activities. Drivers who visit terminals, handle paperwork trips, or conduct any work-related business violate their personal policy terms without realizing the consequences.

Specialized coverage addresses this gap by protecting personal vehicles during work-related use. This protection becomes essential when company policies fail to cover personal vehicle damage that occurs during employment activities (including commutes to different terminals or mandatory training sessions).

Occupational Accident Insurance

Workers’ compensation falls short of providing comprehensive protection for truck drivers, particularly given the average driver age of 55 years and higher health risks from sedentary work. This coverage provides income replacement and medical benefits that company policies typically limit or exclude entirely.

Professional association group plans offer cost-effective options for independent coverage. Marketplace plans provide ACA-compliant coverage that helps drivers avoid state tax penalties in California and New Jersey. The sedentary lifestyle and irregular hours increase risks of obesity, cardiovascular disease, and musculoskeletal disorders that require ongoing medical attention.

These three coverage types address the most significant gaps in employer-provided insurance, but additional protection options can further strengthen a driver’s financial security against unexpected risks. Understanding the claims process helps drivers navigate insurance matters more effectively when incidents occur.

What Extra Protection Should You Consider?

Non-Trucking Liability Coverage

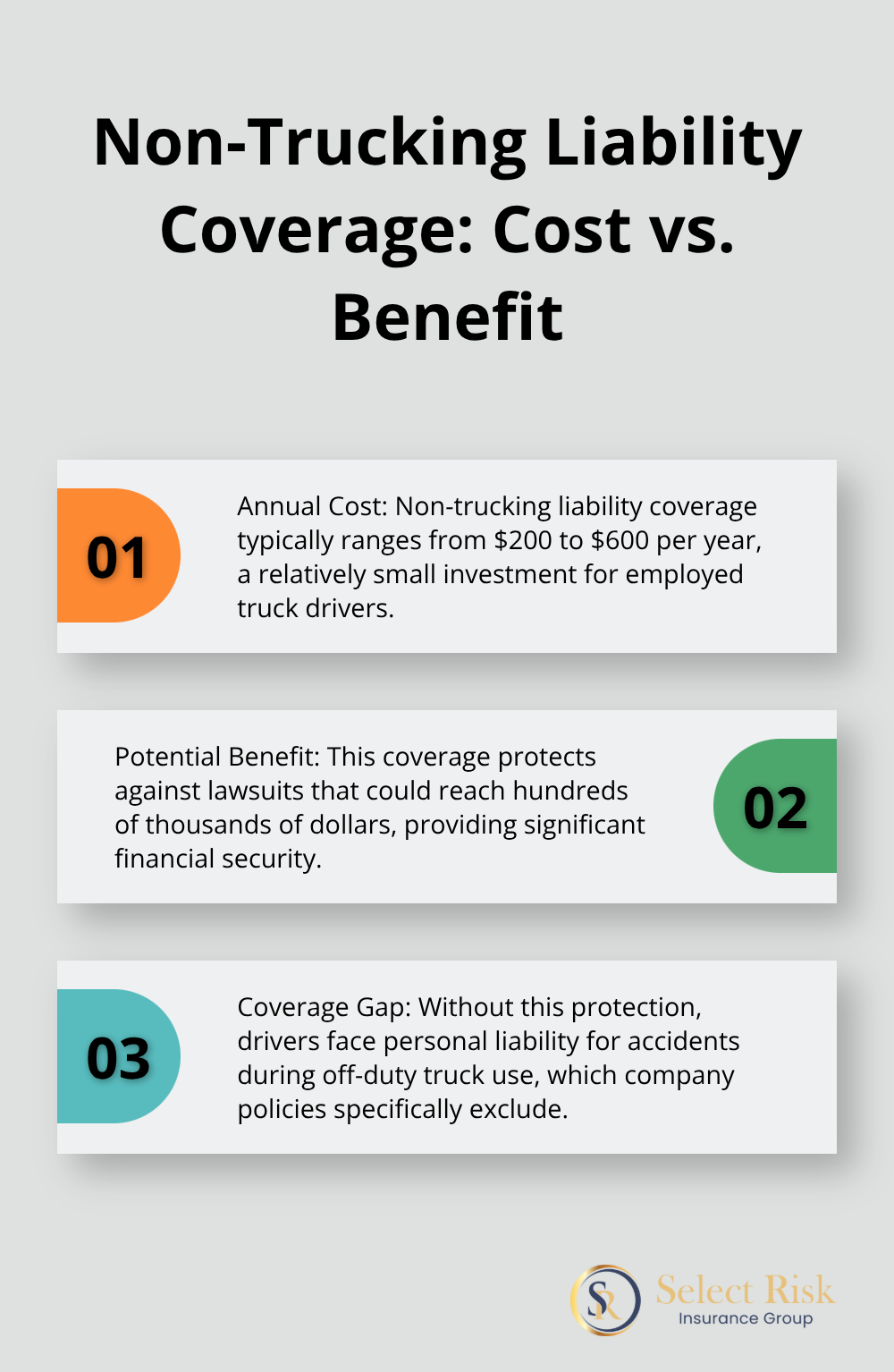

Most employed drivers operate their trucks for personal errands without realizing their company insurance excludes this usage entirely. Non-trucking liability coverage fills this gap by providing coverage for bodily injury and property damage when using the vehicle for personal activities like grocery shopping or medical appointments.

This coverage typically costs between $200 to $600 annually but protects against lawsuits that could reach hundreds of thousands of dollars. Without this protection, drivers face personal liability for accidents that occur during off-duty truck use, which company policies specifically exclude from coverage.

Enhanced Medical Protection

Medical payments coverage and personal injury protection extend beyond basic workers’ compensation requirements, which often prove inadequate for truck drivers. The Bureau of Labor Statistics reports truck drivers face higher injury rates than most occupations (with the average driver age of 55 years increasing medical needs significantly).

Medical payments coverage handles immediate medical expenses regardless of fault, while personal injury protection covers lost wages and essential services during recovery periods. These coverages cost approximately $100 to $300 annually but prevent drivers from depleting personal savings when injuries occur.

Standard company health plans often include high deductibles and limited coverage networks that leave drivers with substantial out-of-pocket expenses during medical emergencies.

Specialized Cargo Protection

Employed drivers who occasionally handle cargo loading, securing, or documentation need cargo insurance protection even when they work for trucking companies. Motor truck cargo coverage protects against financial liability when freight gets damaged, stolen, or lost during transport operations.

This coverage becomes essential when company policies exclude driver liability for cargo handling activities or when drivers face personal lawsuits from cargo owners. Professional drivers should secure $100,000 minimum cargo coverage, which typically costs $400 to $800 annually (depending on freight types handled).

Final Thoughts

Employed truck drivers need comprehensive truck driver coverage that extends far beyond company-provided minimums. Commercial auto liability insurance, physical damage coverage for personal vehicles, and occupational accident insurance form the foundation of adequate protection. Non-trucking liability coverage, enhanced medical protection, and cargo insurance provide additional security against financial risks that employer policies exclude.

The complexity of trucking insurance requires expertise that most drivers lack. Professional agents understand the unique risks employed drivers face and can structure policies that address both personal and professional exposures. Annual policy evaluations help identify new coverage needs, adjust limits based on changing regulations, and take advantage of competitive pricing from different carriers.

We at Select Risk Insurance Group specialize in comprehensive insurance solutions for truck drivers and understand the specific challenges employed drivers encounter. Our independent agency represents multiple financially sound carriers (allowing us to customize coverage that fits your unique situation and budget). We provide the protection your career demands through tailored insurance strategies.