What Insurance Does a Plumber Need in Louisiana?

Running a plumbing business in Louisiana means protecting yourself from real financial risks. Property damage claims, employee injuries, and equipment theft happen more often than you’d think.

At Select Risk Insurance Group, we’ve helped countless plumbers understand what insurance they actually need. The right coverage keeps your business standing when accidents occur.

What General Liability Insurance Actually Covers for Louisiana Plumbers

The Core Protection Your Business Needs

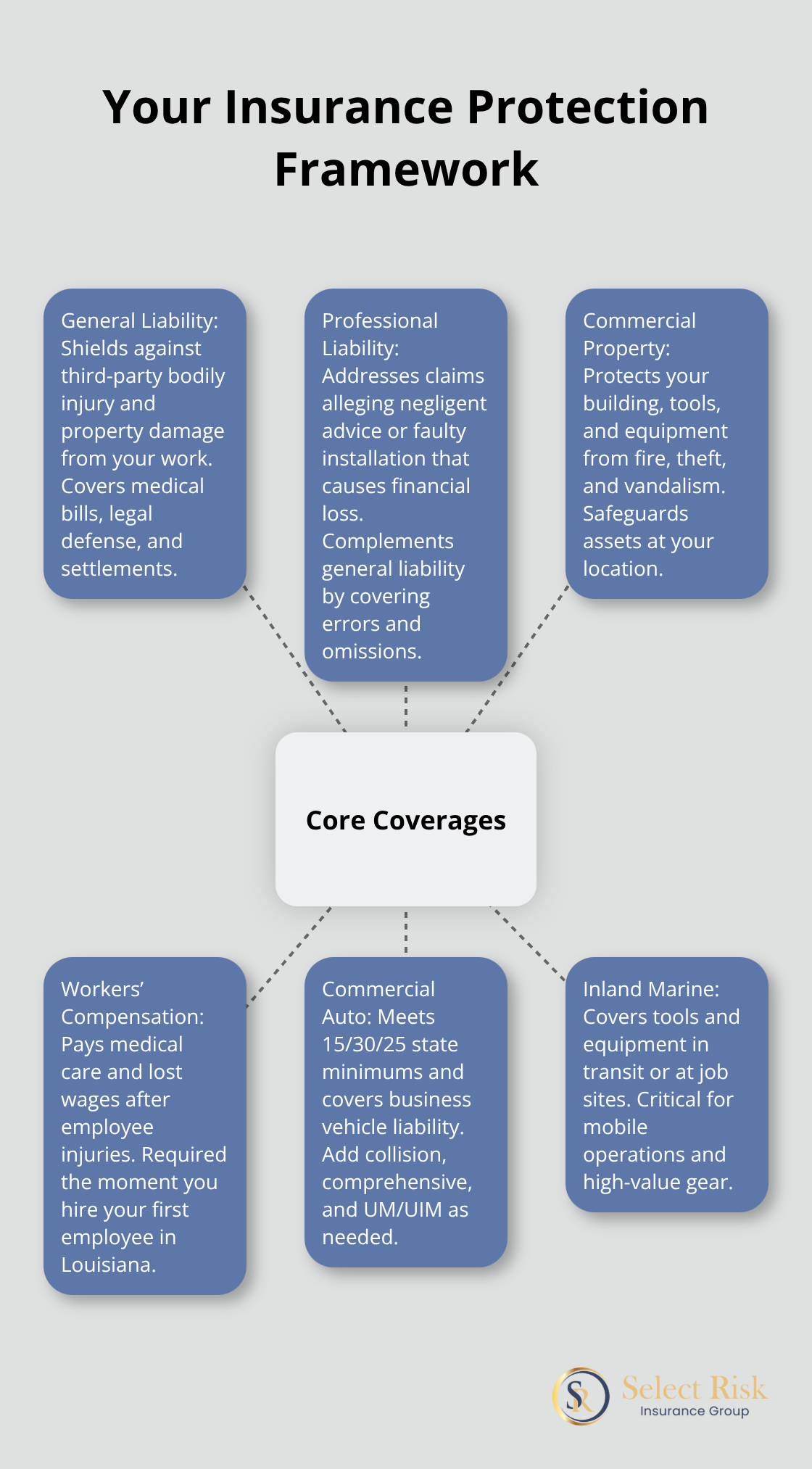

General liability insurance protects your plumbing business from third-party claims that arise directly from your work. When you accidentally flood a customer’s laundry room during a water line repair, or a visitor trips over your equipment at a job site and suffers a broken arm, general liability covers medical bills, legal fees, and settlement costs. Louisiana law requires plumbers to maintain a minimum aggregate limit of $500,000 for general liability and property damage coverage through an authorized insurer. This isn’t optional-it’s a licensing requirement enforced by the State Plumbing Board and License Authority.

Why Licensing Depends on Proof of Coverage

Without proof of this coverage, you won’t receive your master plumber or master natural gas fitter license. If your policy lapses, the board can deny renewal or revoke your license until you restore coverage. The state takes this requirement seriously because it protects customers and the public from financial exposure when plumbing work causes harm.

Property Damage Claims Happen More Often Than You Think

Property damage claims from plumbing work occur regularly in Louisiana. A faulty installation that causes water damage to drywall, flooring, or fixtures can trigger tens of thousands in repair costs. Professional liability insurance (also called errors and omissions coverage) fills a related gap by protecting against claims that your professional advice or installation work caused a customer’s financial loss through negligence. Many Louisiana plumbers skip this coverage, which means they face personal liability if a customer sues over a faulty repair.

Building Your Complete Protection Framework

Commercial property insurance complements general liability by protecting your own equipment, tools, and business location from fire, theft, and vandalism. The combination of general liability, professional liability, and property coverage creates the protection framework that serious plumbing operations require. These three layers work together to address both the risks you create for others and the risks that threaten your own assets.

Moving Forward With Your Coverage Strategy

Understanding what general liability covers is only the first step. Your plumbing business also faces specific risks from your employees and the vehicles you operate on job sites.

Workers’ Compensation Insurance in Louisiana

The Legal Requirement You Cannot Ignore

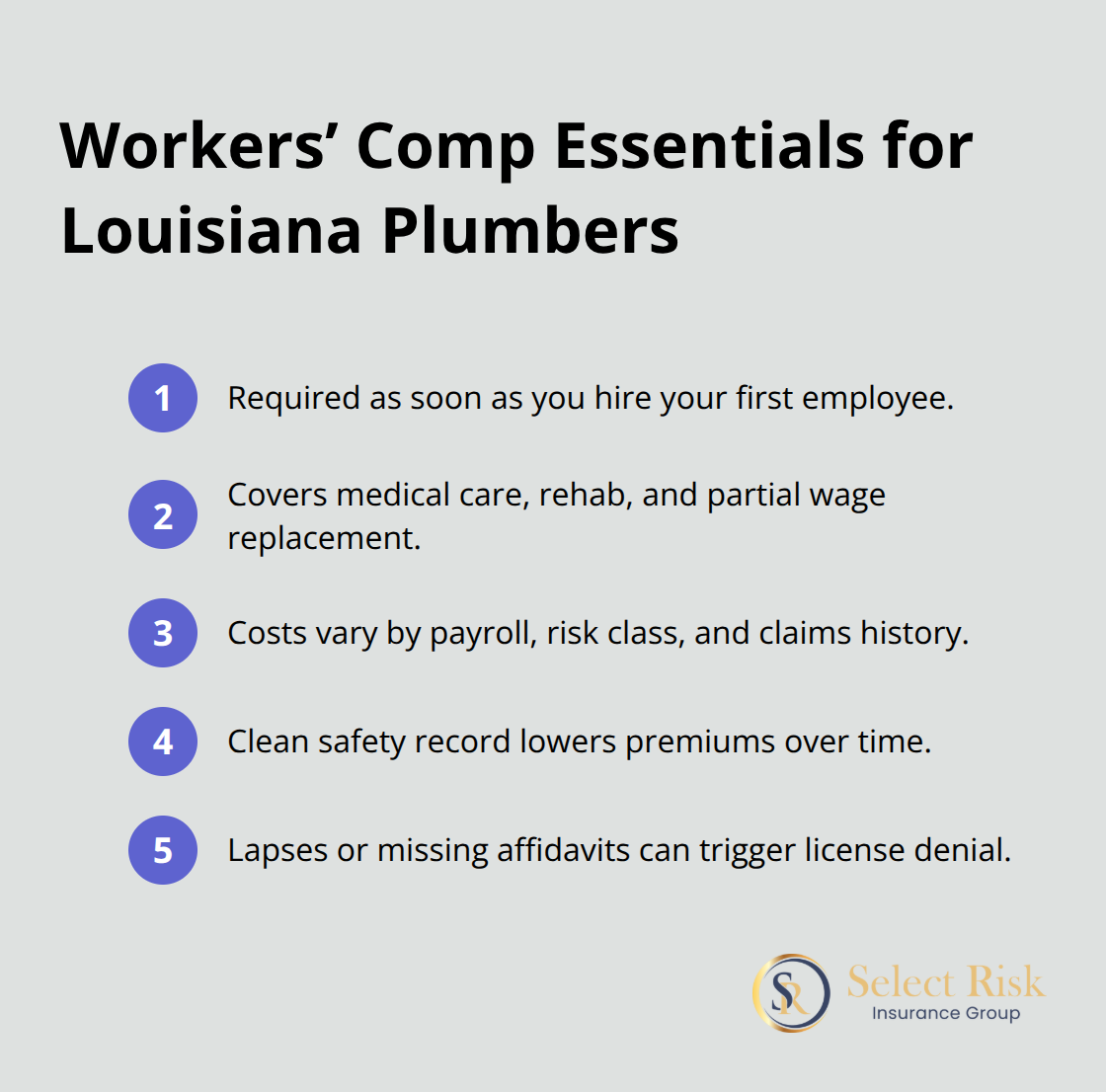

Louisiana mandates workers’ compensation coverage the moment you hire your first employee. This requirement comes directly from state law and the State Plumbing Board and License Authority-it’s not optional. If you operate as a sole proprietor with no employees, you can submit a notarized affidavit of workers’ compensation exemption instead, but this affidavit expires on December 31 of each license year and requires renewal annually. The board will deny your license renewal or revoke your active license if you fail to maintain current coverage or provide the required documentation.

What Workers’ Compensation Actually Pays

When an employee gets injured on a job site, workers’ compensation covers medical treatment, rehabilitation costs, and a portion of lost wages during recovery. A plumber who suffers a severe back injury while installing a water heater receives payment for surgery, physical therapy, and wage replacement while healing. Louisiana law requires employers to carry this coverage because medical bills and lost income can devastate both workers and small businesses. Without this protection, you face personal liability for employee injuries and potential financial collapse.

How Your Claims History Affects Your Costs

The cost of workers’ compensation varies based on your payroll, the specific job classifications, and your claims history. Plumbing ranks as a higher-risk trade, so premiums reflect that reality. However, maintaining a clean claims record directly reduces your rates over time. Investing in job site safety and proper employee training pays dividends in lower insurance costs year after year. Many plumbers wrongly assume that workers’ comp is purely an expense, when it actually protects your business from catastrophic financial loss when accidents happen.

Avoiding License Suspension Through Compliance

Lapses in coverage create serious consequences. We’ve observed plumbing businesses lose their licenses because they let coverage lapse or missed the renewal deadline on their exemption affidavit-a situation that is entirely preventable. Staying compliant means maintaining current coverage and submitting required documentation on time. The administrative burden is minimal compared to the cost of losing your license and the ability to operate.

Protecting Your Workforce and Your Bottom Line

Workers’ compensation protects both your employees and your business. Your workforce gains financial security when injuries occur, and your business gains protection from personal liability claims. This coverage also demonstrates to customers and potential clients that you operate a professional, responsible plumbing operation. With workers’ compensation in place, you can focus on the work itself rather than worrying about catastrophic injury costs. Your employees and your business vehicles represent your most significant operational assets, and the next section covers how to protect the vehicles that carry your team to job sites across Louisiana.

Commercial Auto Insurance and Tools Coverage

Meeting Louisiana’s Vehicle Requirements

Your service vehicles operate as mobile job sites, and Louisiana law mandates minimum auto liability limits of 15/30/25 for all business vehicles. This translates to $15,000 per person, $30,000 per accident for bodily injury, and $25,000 for property damage. Standard personal auto insurance explicitly excludes business use, so operating a work vehicle under a personal policy leaves you uninsured and violates state law. Commercial auto insurance covers liability when your vehicle causes injury or property damage, collision and comprehensive protection for your own vehicle, and uninsured or underinsured motorist coverage when other drivers lack adequate insurance.

Protecting Against Mobile Operation Risks

Louisiana plumbing work involves constant travel between job sites, emergency calls at odd hours, and equipment-loaded vehicles that present higher accident risk than typical business vehicles. Your commercial auto policy should also cover hired and non-owned vehicles if you occasionally rent equipment or allow employees to use personal vehicles for business purposes. The state plumbing board requires proof that service vehicles display permanent signage on both sides with your business name, physical address, phone number, and license number in at least 2-inch lettering.

A vehicle liability certificate must be on file with the board, or you can submit a copy of your proof of insurance card for each service vehicle in lieu of a separate certificate. Many plumbers overlook this documentation requirement and face enforcement fees when the board discovers missing certificates.

Safeguarding Your Equipment Investment

Tools and equipment represent significant capital investment, and commercial property insurance may not fully cover portable items you transport between job sites. Inland marine insurance specifically protects equipment and tools from theft, damage, and loss while in transit or at job sites. Drain cameras, pipe wrenches, diagnostic equipment, and specialized tools can total tens of thousands of dollars, and losing this equipment to theft or damage halts operations and forces expensive replacement. An inland marine policy covers your equipment whether it sits in your truck overnight, gets stolen from a job site, or gets damaged during transport. This coverage is separate from general liability and property insurance because it addresses the unique exposure of mobile operations. Many plumbing businesses operate without this protection and absorb losses directly when theft or damage occurs. The cost of inland marine coverage is modest compared to replacing a stolen drain camera or set of specialized tools, yet most plumbers either skip it or remain unaware the coverage exists. Request quotes that include inland marine protection alongside your commercial auto and general liability policies to ensure complete coverage for your mobile operation.

Conclusion

Running a plumbing business in Louisiana requires understanding what insurance a plumber needs to operate legally and protect against real financial exposure. General liability with a $500,000 aggregate limit protects you from third-party claims, workers’ compensation covers employee injuries and is mandatory the moment you hire staff, and commercial auto insurance meets state minimum requirements while protecting your mobile operations. Inland marine coverage safeguards your equipment investment, and professional liability fills gaps that general liability alone cannot address.

We at Select Risk Insurance Group represent multiple financially sound insurance carriers, which allows us to compare coverage options and pricing across different companies rather than locking you into a single insurer. This approach helps you avoid protection gaps and find competitive rates that fit your budget. Our team has guided countless Louisiana plumbing businesses through the insurance landscape and understands the licensing requirements from the State Plumbing Board and License Authority.

Contact Select Risk Insurance Group to discuss your specific business needs and obtain quotes that address general liability, workers’ compensation, commercial auto, property coverage, and inland marine protection. Our agents review your current operations, identify coverage gaps, and explain how each policy protects your business. We handle the administrative details so you can focus on running your plumbing operation.