The Average Cost of Plumbing Insurance in Louisiana

Plumbing businesses in Louisiana face real pressure when it comes to insurance costs. Rates vary significantly based on your operation size, experience, and the specific services you offer.

At Select Risk Insurance Group, we’ve helped countless plumbing contractors understand what they’re actually paying for and why. This guide breaks down the real numbers behind plumbing insurance cost in Louisiana and shows you how to find coverage that fits your budget.

What Plumbing Insurance Actually Covers

Plumbing contractors in Louisiana need to understand exactly what their insurance policies protect. General liability insurance is your first line of defense when you damage a customer’s property during an installation or repair. If you accidentally crack a tile floor while running a water line or cause water damage through a faulty connection, general liability covers the repair or replacement costs plus legal fees if the customer sues. In Louisiana, plumbing contractors pay an average of $363 per month for general liability coverage, according to MoneyGeek data, which is substantially higher than the statewide average of $118 per month for other industries. This premium reflects the real risk that plumbing work carries-water damage claims are frequent and expensive in Louisiana’s climate.

Tools and Equipment Need Their Own Protection

Your tools and equipment require dedicated coverage that goes beyond basic property insurance. Commercial property insurance protects your company vehicles, service trucks, and the contents inside them from fire, theft, and weather damage. In Louisiana, where hurricanes and severe storms strike regularly, this coverage becomes essential. If a storm damages your truck or the equipment stored inside it, standard property coverage helps you replace tools without draining your cash reserves. Many plumbing contractors overlook equipment breakdown coverage, which pays for repairs when your compressor, water heater testing equipment, or diagnostic tools fail unexpectedly. This coverage costs relatively little but prevents the frustration of losing expensive diagnostic equipment mid-job.

Workers Compensation Protects Your Team

Louisiana requires workers’ compensation insurance for any plumbing business with employees, and this is where many contractors face unexpected costs. Workers’ comp in Louisiana averages $64 per month for plumbing businesses and covers medical expenses, lost wages, and rehabilitation costs if an employee suffers an injury on the job. Plumbing work involves physical risks-falls from ladders, back injuries from heavy lifting, and burns from hot water create frequent claims. If you operate as a solo owner with no employees, you can submit a notarized affidavit of workers’ compensation exemption to the State Plumbing Board instead, but this exemption applies only to the owner-operator. The moment you hire your first employee, you must carry active coverage and maintain a current Certificate of Insurance filed with the board.

Professional Liability Covers Your Workmanship

Professional liability insurance, sometimes called errors and omissions coverage, protects you when your installation work fails and causes damage. Louisiana plumbing contractors pay about $90 per month for this coverage, which reimburses customers if your workmanship mistakes result in water leaks or system failures that damage their property. This protection matters because a single installation error can lead to thousands of dollars in water damage claims (especially in Louisiana’s humid climate where moisture problems compound quickly). Your liability exposure extends beyond the initial job-latent defects in your work can surface months or even years later, and professional liability covers those delayed claims.

Understanding these four coverage types-general liability, property, workers’ compensation, and professional liability-gives you a foundation for protecting your business. The next step involves recognizing what actually drives your costs up or down, which varies dramatically based on your specific operation.

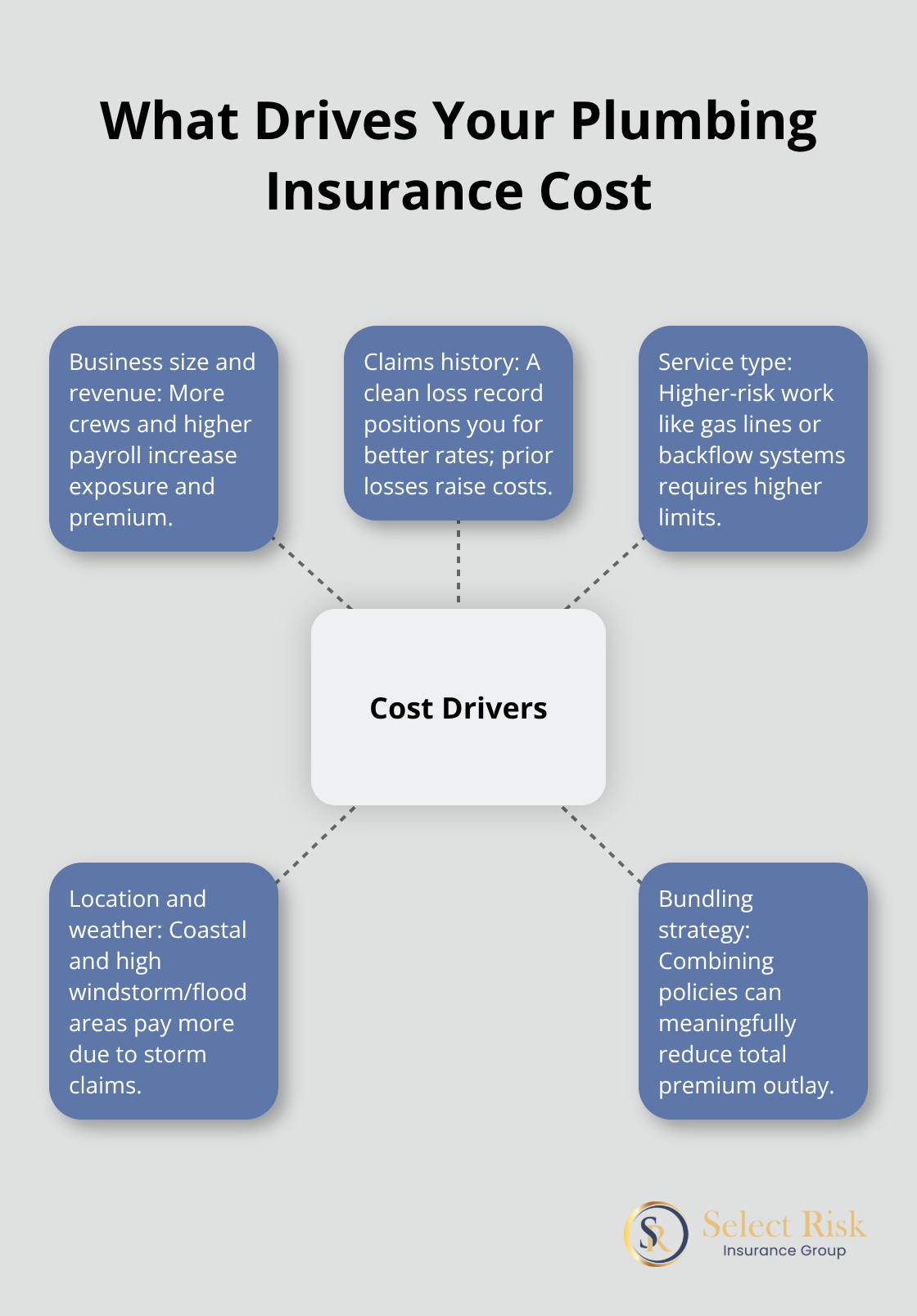

What Drives Your Insurance Costs Up or Down

Insurance companies don’t calculate your plumbing premium randomly, and rates vary significantly from one contractor to the next in Louisiana. Your rate depends on measurable factors tied directly to your operation’s risk profile. Business size matters enormously because a solo operator with no employees faces completely different risk exposure than a contractor running a crew of five technicians. A business generating $150,000 in annual revenue typically pays less than one generating $500,000, simply because higher revenue correlates with more jobs, more customer interactions, and more opportunities for claims. MoneyGeek’s analysis uses a standard small plumbing business profile with two employees and $150,000 in payroll to compare rates nationwide, and this profile sits at the lower end of the pricing spectrum. If you run a larger operation with multiple crews, higher payroll, and more complex projects like commercial installations or backflow prevention work, your premiums scale upward accordingly.

Your Claims History Shapes Your Rate

Your track record influences your premium just as much as your current size. Insurance companies pull your loss history and claims record, and a clean record without prior claims can save you 10 to 15 percent compared to contractors with previous losses. If you filed water damage claims in the past or had workers’ compensation incidents, insurers view you as higher risk and charge accordingly. Staying claim-free for three to five years demonstrates responsible operations and positions you for better rates at renewal.

Service Type Determines Your Risk Category

The specific services you offer reshape your premium significantly. General plumbing repairs and installations carry baseline risk, but adding services like gas line work, backflow prevention systems, or commercial water system installations pushes you into higher-risk categories. These expanded services demand greater general liability limits (often $2 million or more) and higher premiums to match the increased exposure.

Location and Weather Exposure Add Costs

Louisiana’s coastal geography and hurricane exposure affect rates substantially. Contractors operating in parishes with higher windstorm or flood risk pay premiums that reflect that exposure. Your service area directly influences what insurers charge because storm damage and water intrusion claims spike in high-risk zones.

Bundling Policies Cuts Your Total Cost

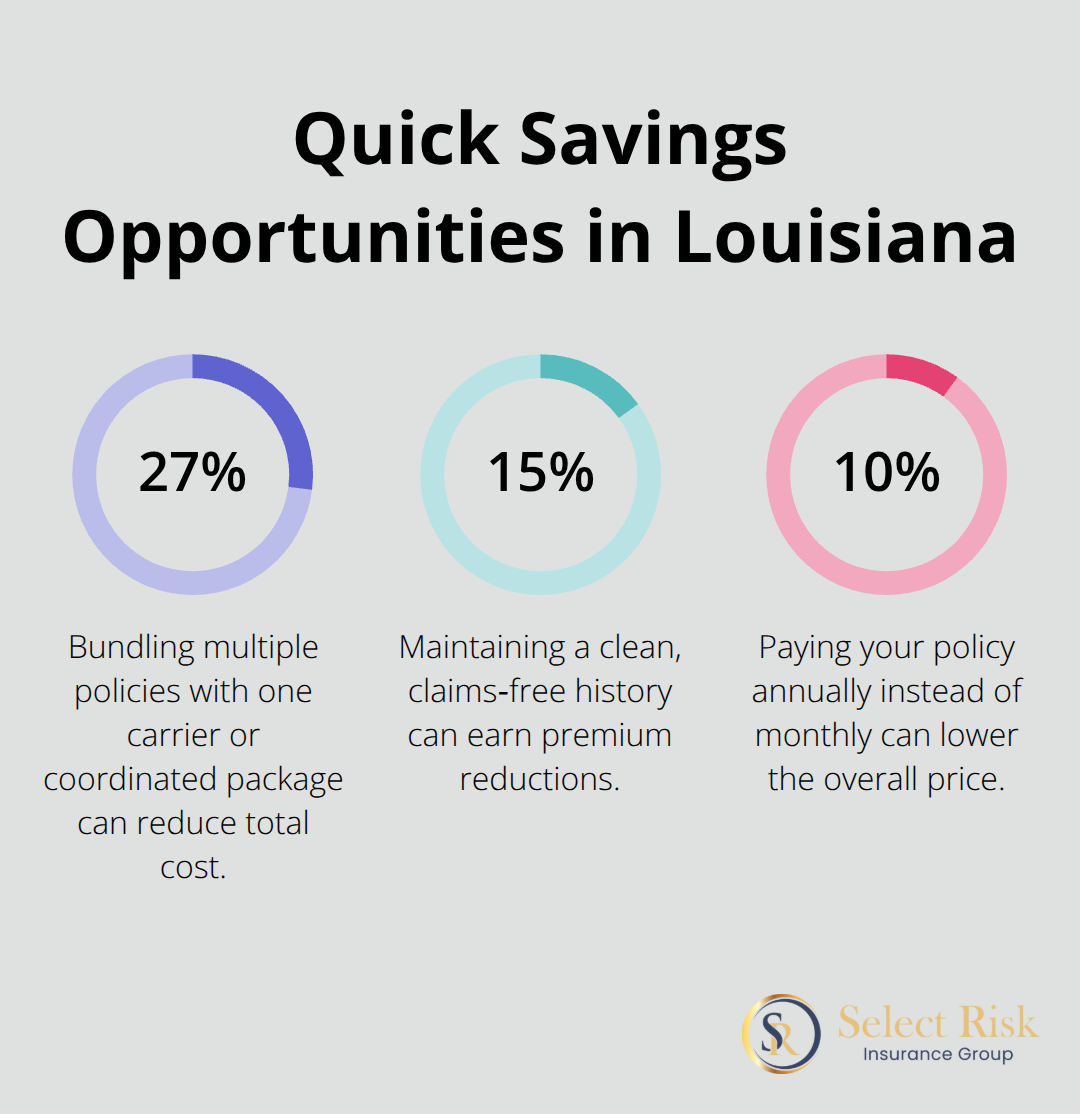

Combining your policies together typically reduces your total cost by 19 to 27 percent compared to buying general liability, workers’ compensation, and professional liability separately. This strategy represents one of the most effective cost-reduction approaches available to you. When you consolidate coverages with one carrier or through an independent agent who can coordinate multiple policies, you unlock substantial savings that add up year after year.

Understanding these cost drivers positions you to make smarter decisions about your coverage structure. The next step involves learning where to find competitive quotes and which discounts actually apply to your specific operation.

How to Find Affordable Plumbing Insurance in Louisiana

Shopping for plumbing insurance in Louisiana requires a strategic approach because rates fluctuate dramatically between carriers. The Hartford, NEXT Insurance, and Simply Business consistently offer competitive pricing for Louisiana plumbing contractors, but your actual quote depends on how well each insurer understands your specific operation. You need quotes from at least three different carriers to reveal the real price range in your market and avoid overpaying simply because you didn’t compare options.

Most carriers provide online quote tools that take 10 to 15 minutes to complete, asking about your business size, service types, claims history, and coverage limits. Online quotes give you a starting point, but phone conversations with underwriters often uncover discounts or coverage adjustments you won’t find on a website. When you call, ask explicitly whether the insurer offers discounts for safety training, multi-policy bundling, or claims-free histories because many carriers don’t advertise these reductions prominently. One tactical advantage: you save money when you pay your annual premium upfront rather than monthly, which adds up to hundreds of dollars annually on a plumbing business policy.

Independent Agents Access Broader Markets

An independent insurance agent representing multiple carriers can compare 15 to 20 different companies simultaneously, something you cannot do alone. This access matters because rates vary wildly between insurers for identical coverage, and an agent’s relationships with underwriters sometimes unlock better pricing than you’d receive applying directly. Independent agents also understand Louisiana-specific risks like coastal windstorm exposure and can structure your coverage to address local hazards without overbuying unnecessary protection.

When you select an agent, verify they have experience with plumbing contractors specifically because agents familiar with your industry understand the coverages you actually need and which carriers specialize in trades. Ask whether they handle claims support and how quickly they respond to questions, since service quality becomes critical when you file a claim and need fast resolution. An independent agency in your region brings local market knowledge and can meet with you in person to review your operation and discuss coverage details face-to-face.

Bundling Policies Unlocks Real Savings

You reduce your total cost when you combine general liability, workers’ compensation, and professional liability into a single package through one carrier or coordinated policies. This bundling discount represents the single most impactful cost reduction available to plumbing contractors in Louisiana. Beyond the discount percentage, bundling simplifies your administration because renewals happen simultaneously, reducing the chance you’ll miss a deadline or let coverage lapse.

Request bundled quotes explicitly and compare the combined price against individual policy quotes to confirm the savings. Some carriers also offer discounts for higher deductibles on property coverage, allowing you to reduce premiums if you increase your equipment deductible from $1,000 to $2,500 or $3,000-a strategy that works well if you maintain emergency reserves to cover tool replacement costs.

Final Thoughts

Plumbing insurance cost in Louisiana depends on factors you can measure and control. Your business size, claims history, service offerings, and location shape what you pay, but bundling policies typically saves you 19 to 27 percent compared to purchasing coverage separately. Paying annually instead of monthly adds another 5 to 10 percent in savings, reducing your annual insurance expense by hundreds of dollars without cutting coverage.

Adequate general liability, professional liability, workers’ compensation, and property insurance protects your finances and allows you to operate with confidence. Louisiana’s climate and regulatory environment demand this protection because storm damage and water intrusion claims happen frequently, and the State Plumbing Board requires active Certificates of Insurance on file before you can legally operate. Your coverage becomes your foundation for growth because it allows you to take on larger projects, hire employees, and expand your service offerings without exposing yourself to catastrophic risk.

Contact at least three carriers or work with an independent agent who can access multiple companies simultaneously to find competitive plumbing insurance cost in Louisiana. When you request quotes, ask about bundling discounts, claims-free reductions, and annual payment savings explicitly because these reductions often aren’t advertised. Select Risk Insurance Group based in Lafayette can compare coverage options across multiple carriers and help you structure a policy that matches your specific operation and budget.