Workers Comp for Roofers in Louisiana [A Complete Guide]

![Workers Comp for Roofers in Louisiana [A Complete Guide]](https://selectriskgroup.com/wp-content/uploads/emplibot/Workers-Comp-for-Roofers-in-Louisiana-_A-Complete-Guide__1767049923-1030x589.jpeg)

Roofing is one of Louisiana’s most dangerous jobs, and workers comp for roofers in Louisiana isn’t optional-it’s the law. We at Select Risk Insurance Group know that protecting your team starts with understanding what coverage you actually need.

This guide walks you through Louisiana’s requirements, common roofing injuries, and how to keep your premiums reasonable without cutting corners on protection.

What Louisiana Actually Requires From Roofing Contractors

Louisiana’s workers compensation law is straightforward: if you have even one employee, you must carry coverage. No exceptions. The state does not issue exemption certificates or allow you to skip it based on company size or worker status.

Understanding Your Class Code and Rate Range

Louisiana Class Code 5551 for roofing contractors carries rates between 12.87 and 31.53 per $100 of payroll. This wide range exists because your actual premium depends on your total payroll, the specific roofing tasks you perform, and your accident history. Louisiana’s rates rank about 67% above the national average according to the National Council on Compensation Insurance, so understanding what drives your individual rate matters significantly.

Worker Classification Rules That Protect You

If you hire subcontractors or have workers classified as 1099 contractors but direct their work and provide support, they still qualify as employees under Louisiana law. Misclassifying them as independent contractors will not protect you from liability. The Louisiana Office of Workers’ Compensation Administration confirms that you can verify whether your contractors have active coverage using the Workers’ Compensation Coverage Verification Search-something you should do before they step on a job site.

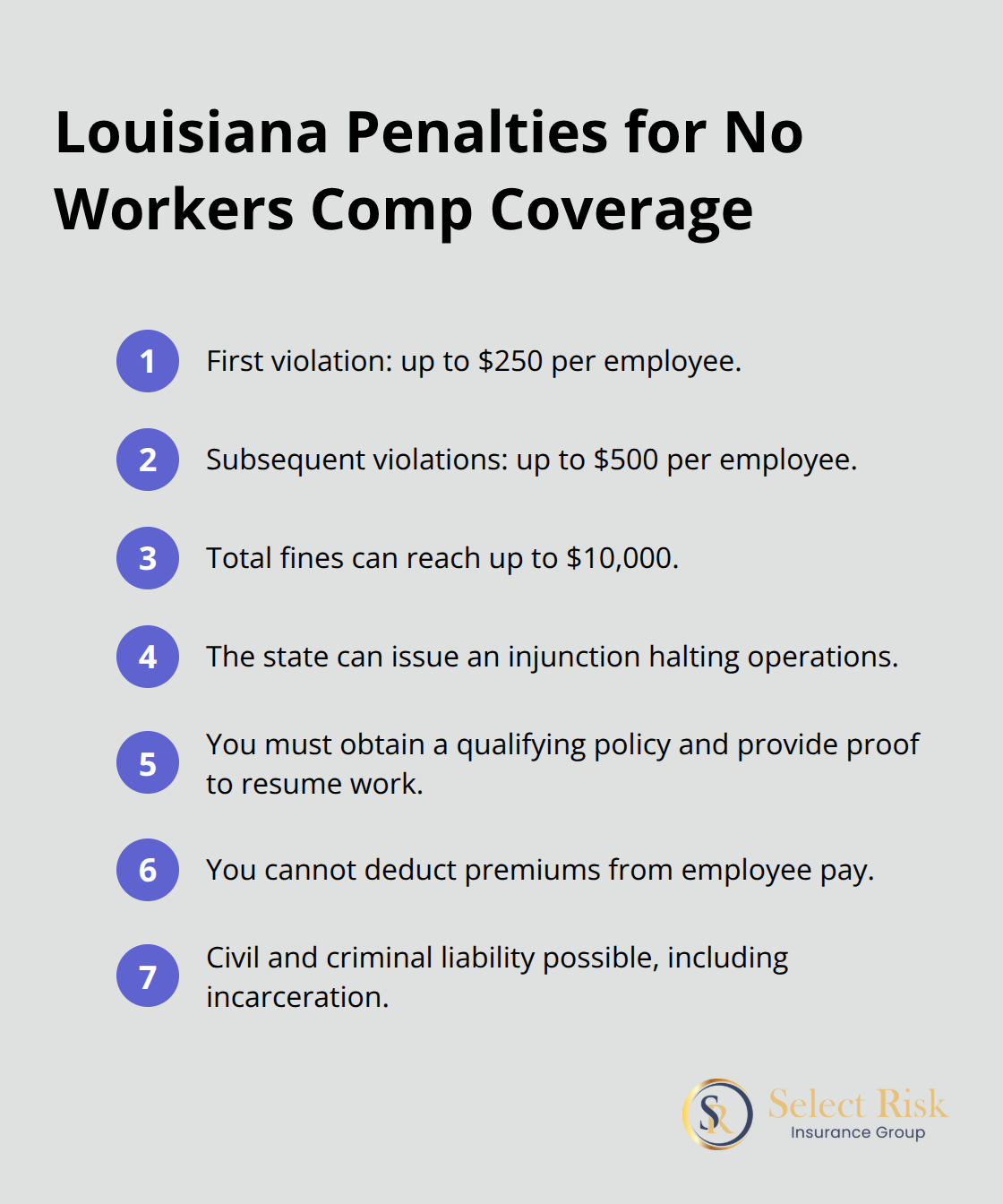

Penalties for Operating Without Coverage

The penalties are serious enough that ignoring this requirement is reckless. Louisiana imposes fines up to $250 per employee for a first violation, $500 per employee for subsequent violations, and up to $10,000 total. Worse, the state can issue an injunction that halts your business operations until you obtain a qualifying policy and provide proof.

You cannot withhold premiums from employee pay to offset costs-doing so creates civil and criminal liability, including potential incarceration.

Managing Your Costs Without Cutting Corners

Cost is a real concern, but you have options to manage expenses. A strong safety program that demonstrates fewer workplace incidents lowers your Experience Modification Rate, which directly reduces premiums. Pay As You Go plans align your monthly payments with actual payroll, improving cashflow. Shopping across Louisiana’s 35+ workers comp providers lets you compare rates side-by-side rather than accepting the first quote. An independent agency can represent multiple carriers and help you find coverage that fits your operation and budget.

Understanding these requirements sets the foundation, but knowing what injuries your team faces on the job helps you select the right coverage limits and protection levels.

What Injuries Do Roofers Face and What Does Workers Comp Actually Cover

Falls From Heights: The Leading Roofing Hazard

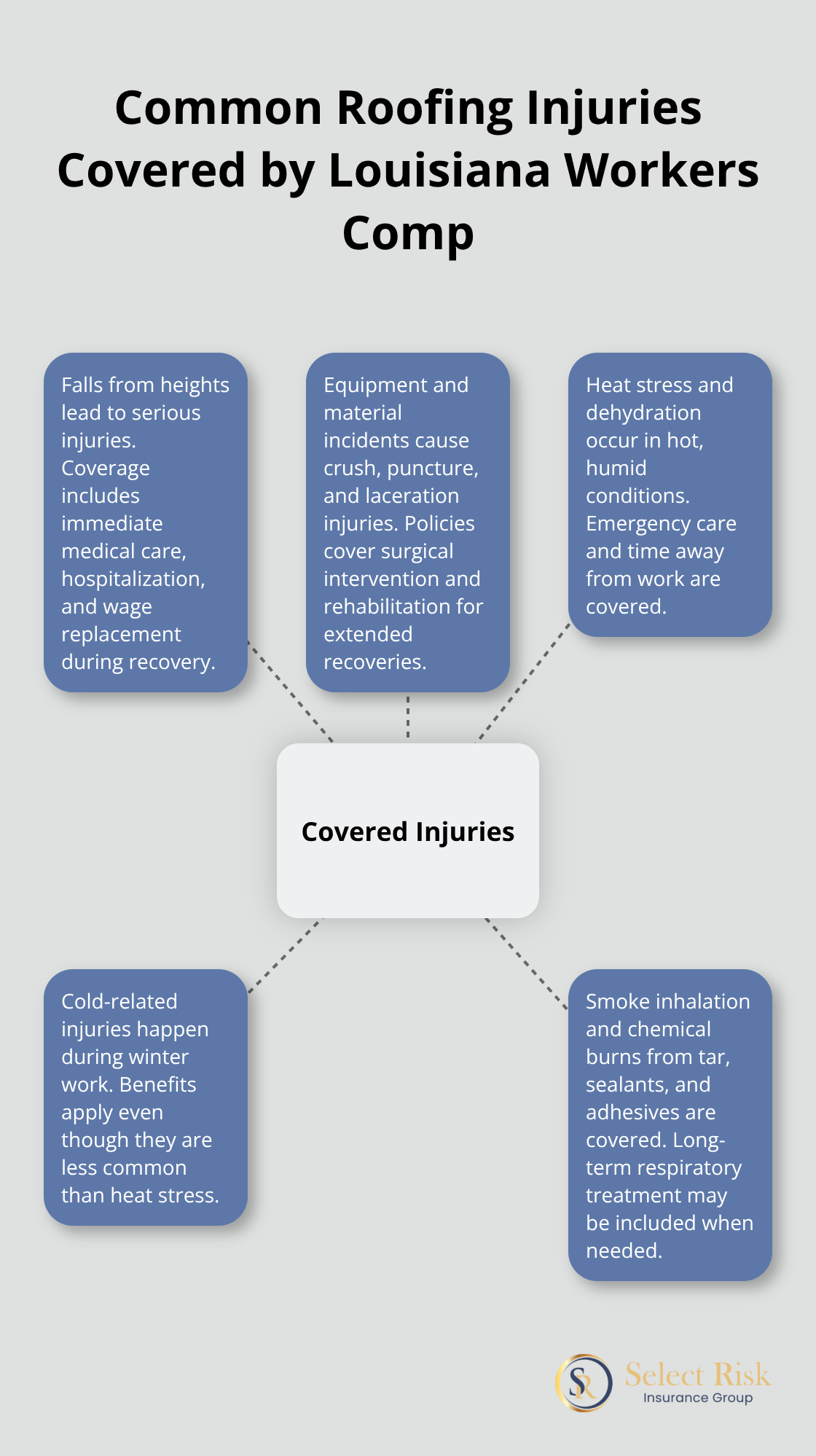

Falls from heights dominate roofing injury statistics, and Louisiana’s workers compensation system covers them fully regardless of fault. Construction industry data shows falls account for roughly one-third of all serious workplace injuries, with roofers facing exponentially higher risk than most other trades. A roofer who slips on wet shingles during a storm, loses footing on a ladder, or falls through a skylight receives immediate medical coverage, hospitalization costs, and wage replacement while recovering. Louisiana’s no-fault system means your employee doesn’t need to prove negligence to receive benefits, and you don’t face a lawsuit for providing the coverage required by law.

Equipment and Material-Related Injuries

Beyond falls, roofers encounter crush injuries from dropped materials, puncture wounds from nails and fasteners, and lacerations from metal flashing or roofing edges. Equipment-related incidents involving pneumatic nailers, power saws, and other tools frequently result in severe hand and finger injuries that require extended rehabilitation. Workers comp covers all surgical intervention, physical therapy, and lost wages during recovery periods that can stretch months or longer.

Heat Stress and Weather-Related Conditions

Weather-related conditions in Louisiana create additional hazards that workers comp addresses directly. Heat exhaustion and dehydration occur regularly during Louisiana’s hot, humid summers when roofers work in direct sunlight on surfaces that absorb and radiate extreme temperatures. A roofer experiencing heat stroke or severe dehydration needs immediate medical intervention, and workers comp covers emergency care, physician visits, and time away from work during recovery. Cold-related injuries, while less common than heat stress, still occur during winter months when roofers work on exposed roofs without adequate protection. Smoke inhalation and chemical burns from roofing materials like tar, sealants, and adhesives represent another category of injuries that workers comp covers completely, including long-term respiratory treatment if needed.

Coverage Limits and Benefit Structure

Your coverage limits should reflect the reality of roofing work. Louisiana workers comp provides unlimited medical benefits for work-related injuries, meaning there’s no cap on treatment costs, surgeries, or rehabilitation services your injured employee receives. Wage replacement typically covers two-thirds of the employee’s average weekly wage during temporary disability, continuing until they return to work or reach maximum medical improvement. For permanent disabilities (like a roofer who loses fingers or develops chronic back problems from a fall), disability benefits continue long-term or become permanent depending on the injury severity.

Documentation and Claims Management

The key actionable here is documenting everything immediately after an injury occurs. Photograph the accident scene, gather witness statements from coworkers, note weather conditions and equipment involved, and file the claim within the timeframe Louisiana requires. Delayed reporting weakens your claim position and creates complications for your employee’s benefits. Establish an injury reporting protocol with your crew before accidents happen, assign one person responsibility for documentation, and ensure every supervisor knows the procedure. This preparation transforms a chaotic emergency into a managed process that protects both your employee and your business.

With a clear picture of what injuries your team faces and how coverage protects them, the next step is finding the right provider and structuring your policy to keep premiums manageable while maintaining full protection.

How to Get Workers Comp Coverage That Fits Your Roofing Operation

Gather Your Information Before You Shop

Finding workers comp coverage in Louisiana requires more strategy than calling the first insurer you find. Louisiana has over 35 authorized workers comp carriers, and their rates for roofing contractors vary dramatically based on underwriting criteria that extend far beyond your payroll number. Start by collecting your payroll documentation, detailing the specific roofing services you perform (residential, commercial, storm damage repair, gutter work), and pulling your loss history for the past three to five years. This information determines your Experience Modification Rate, which directly multiplies your base rate. A roofer with no claims in five years might pay 0.85 times the base rate, while one with multiple incidents pays 1.25 or higher.

Compare Quotes Across Multiple Carriers

When you contact carriers or work with an independent agency, they source quotes from multiple insurers simultaneously, letting you compare side-by-side rather than shopping one at a time. This approach reveals the actual range of available pricing for your specific operation. Pay As You Go plans deserve serious consideration because they align your monthly premium payments with actual payroll rather than requiring large upfront deposits, which improves cashflow for seasonal roofing businesses that experience income fluctuations.

Implement Safety programs That Reduce Premiums

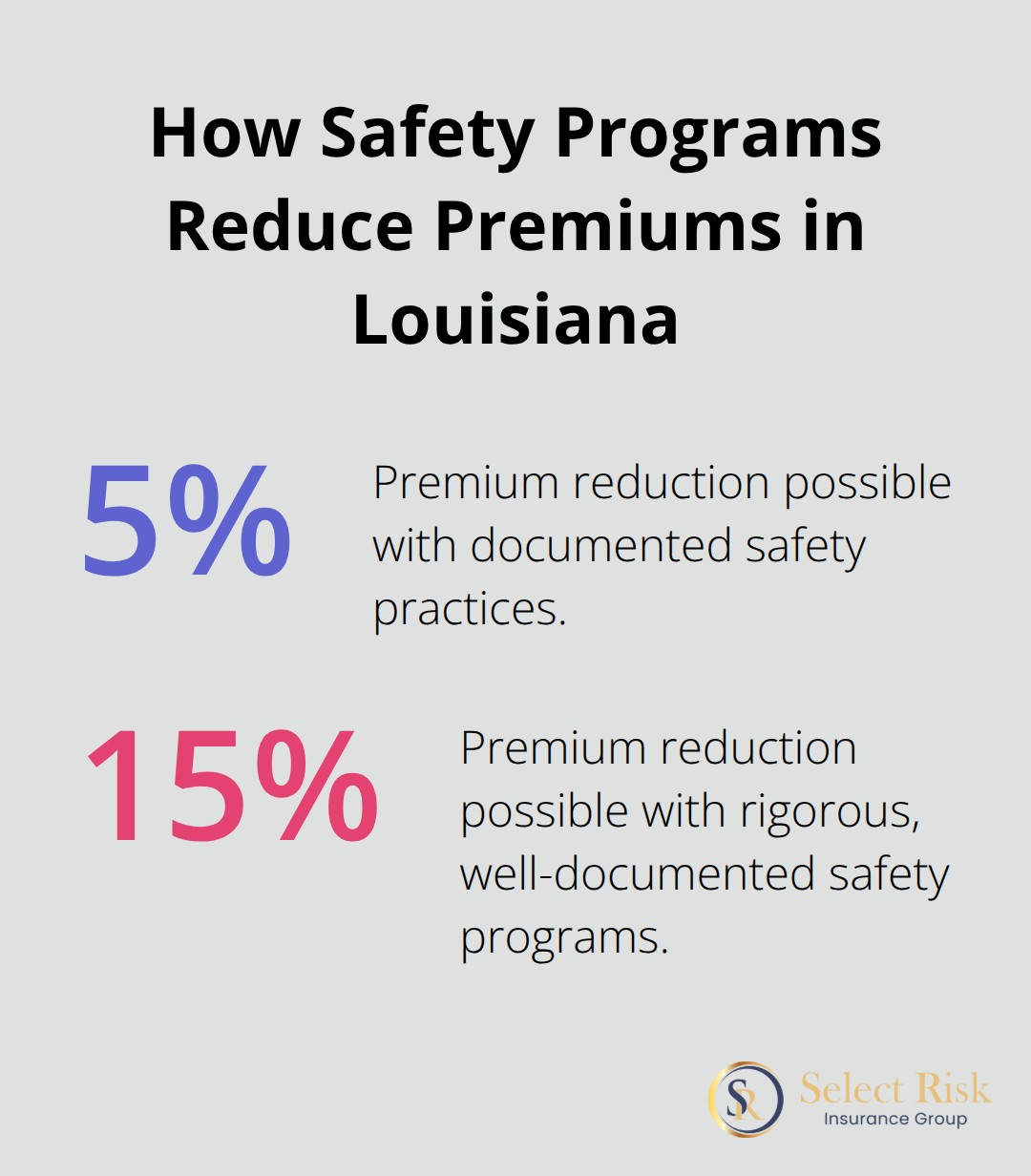

Safety programs directly reduce what you pay, and this isn’t theoretical-demonstrating fewer workplace incidents lowers your EMR and premium costs. Implement a documented daily safety briefing before crews start work, require fall protection equipment on all jobs above six feet, and maintain written records of near-misses and corrective actions. Carriers reward this documentation through policy credits that can reduce your premium by five to fifteen percent depending on program rigor.

File Claims Promptly and Document Everything

After an injury occurs, file your claim immediately rather than waiting to see if the worker recovers on their own. Louisiana requires prompt reporting, and delayed claims create complications for benefit processing and weaken your position with the insurer. Assign one crew member responsibility for documentation at every job site-photograph the scene, record witness statements, note equipment involved, and photograph the injured worker’s wounds or the accident location before cleanup. This preparation transforms an emergency into a manageable process.

Work with an Independent Agency for Better Advocacy

When you work with an independent agency representing multiple carriers, they handle claims filing on your behalf and can advocate for your business during the underwriting process, which matters when your loss history is mixed or your operation involves higher-risk work like storm damage repairs or commercial roofing on multi-story buildings. An independent agency based in Louisiana, like Select Risk Insurance Group, understands the state’s specific requirements and carrier preferences, giving you an advantage in negotiations and claims management.

Final Thoughts

Workers comp for roofers in Louisiana protects your team and your business simultaneously. The law requires it, the risks demand it, and the financial consequences of operating without it are severe enough to shut down your operation. What matters now is moving from understanding the requirement to actually securing coverage that fits your roofing operation.

Your immediate action involves gathering your payroll records, documenting the specific services you perform, and pulling your loss history for the past three to five years. Contact multiple carriers or work with an independent agency to compare quotes side-by-side rather than accepting the first offer. Pay As You Go plans improve your cashflow during seasonal fluctuations by aligning your monthly payments with actual payroll.

We at Select Risk Insurance Group represent multiple carriers throughout Louisiana, which means we source quotes from different insurers and present you with actual options rather than a single recommendation. Our team handles claims filing on your behalf and advocates for your business during underwriting, which matters when your loss history is mixed or your work involves higher-risk projects like storm damage repairs. Contact Select Risk Insurance Group to start your quote process today.

![Best Insurance for Roofing Companies in Louisiana [2025]](https://selectriskgroup.com/wp-content/uploads/emplibot/Best-Insurance-for-Roofing-Companies-in-Louisiana-_2025__1766790632-80x80.jpeg)