Best Insurance for Roofing Companies in Louisiana [2025]

![Best Insurance for Roofing Companies in Louisiana [2025]](https://selectriskgroup.com/wp-content/uploads/emplibot/Best-Insurance-for-Roofing-Companies-in-Louisiana-_2025__1766790632-1030x589.jpeg)

Roofing companies in Louisiana face unique insurance challenges that go beyond standard business coverage. Weather patterns, client demands, and state regulations create specific protection gaps that many contractors overlook.

We at Select Risk Insurance Group have helped dozens of roofing businesses find the right insurance solutions. This guide walks you through the essential coverage types your company needs to operate safely and legally.

Workers’ Compensation Insurance for Roofing Crews in Louisiana

Legal Requirements and Mandatory Coverage

Workers’ compensation is not optional in Louisiana if you have employees. The Louisiana Workforce Commission requires any roofing business with workers on payroll to carry coverage, and the state enforces this strictly. Non-compliance results in fines, license suspension from the Louisiana State Licensing Board for Contractors, and personal liability for work-related injuries. The coverage itself is straightforward: it pays for medical treatment, rehabilitation, and wage replacement when an employee gets hurt on the job. For roofing crews working at heights and handling heavy materials, this protection is essential.

Premium Costs and Payroll Factors

Annual costs typically range from $400 to $3,000 depending on your payroll size and claims history, according to industry data. A small residential operation with two to three employees might pay closer to $400 to $800 annually, while a mid-size commercial crew with ten employees could expect $2,000 to $3,000. The actual premium hinges on your projected payroll, the types of roofing work you perform, and whether you have filed claims in the past. Storm restoration work and high-risk projects push premiums upward because insurers view these jobs as higher-injury environments.

Worker Classification and Compliance

One critical detail: if you classify workers as 1099 independent contractors but treat them as employees through day-to-day management, Louisiana regulators and insurers may still require you to cover them under workers’ compensation. Misclassification exposes you to back-premium assessments and penalties, so align your worker classifications with how you actually supervise and control the work.

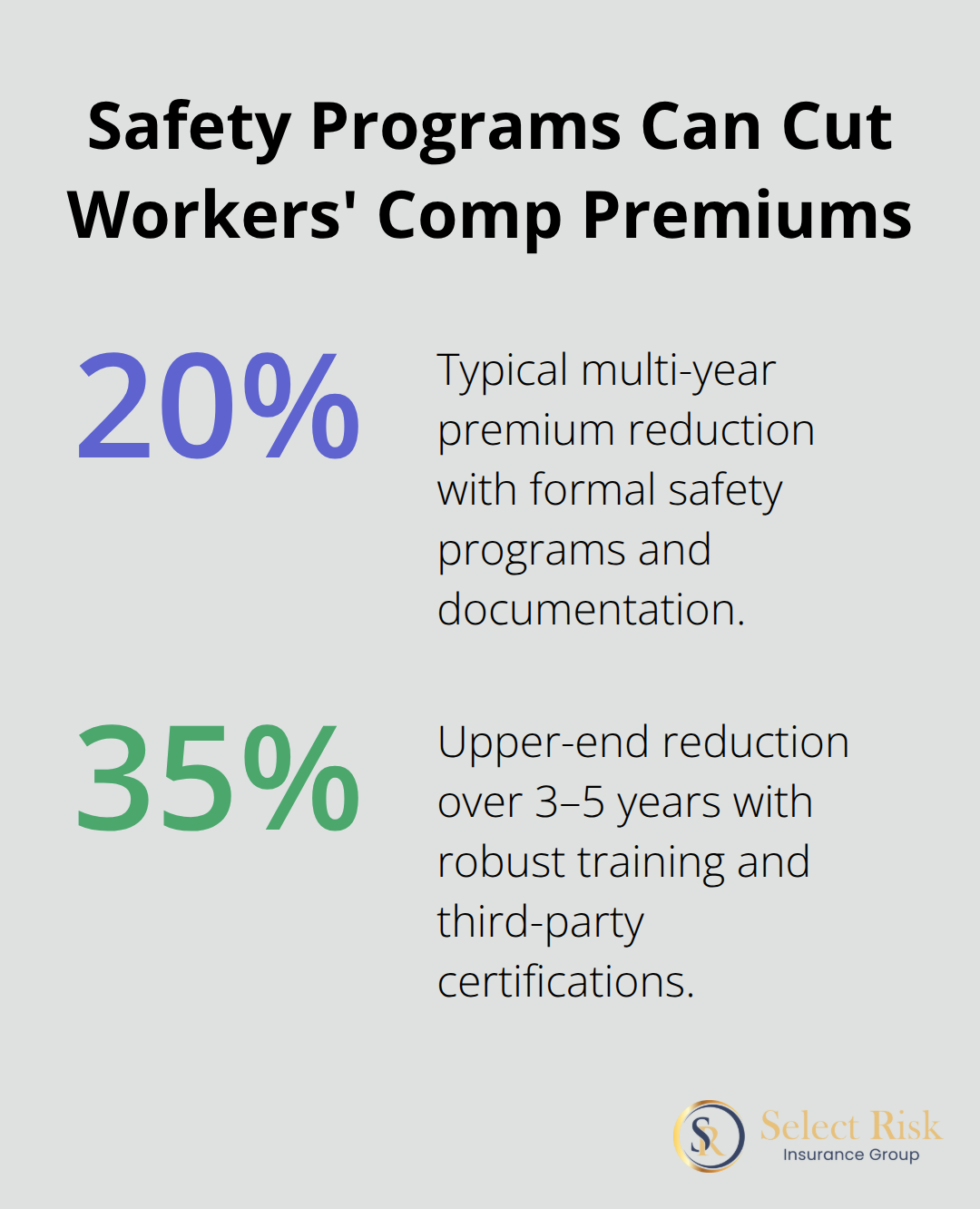

Safety Programs and Premium Reductions

Cost reduction is possible if you invest in safety. Roofing companies that implement formal OSHA training, obtain third-party safety certifications like ISNetworld or Avetta, and maintain detailed incident records can see premium reductions of 20 to 35 percent over three to five years according to U.S. Department of Labor findings. Your insurer will conduct an annual review of your operations and safety practices, so document everything: training attendance, incident reports, corrective actions, and equipment maintenance.

When you file a claim, a dedicated service representative manages the process and helps coordinate with medical providers. Certificates of Insurance can be issued the same day you request them, which speeds up project onboarding when clients require proof of coverage.

Weather Risk and Continuous Coverage

Louisiana’s weather patterns create injury risk year-round-from hurricane season through routine maintenance work-so maintaining continuous coverage without gaps protects both your crew and your business. Beyond workers’ compensation, your roofing operation also needs protection against third-party claims and property damage, which brings us to commercial general liability and the specialized coverages that shield your company from client lawsuits and weather-related losses.

Commercial General Liability and Property Coverage in Louisiana Roofing

What General Liability Actually Covers

General liability insurance protects your business from third-party claims that can destroy your finances. When a homeowner slips on your scaffolding or your crew damages a neighbor’s property during a roof replacement, general liability pays for medical expenses, property repairs, and legal defense costs. Louisiana requires roofing contractors to carry a minimum of $300,000 per occurrence and $600,000 aggregate, but this floor leaves you exposed. Most roofing companies operating in Louisiana carry $1,000,000 per occurrence and $2,000,000 aggregate because clients demand it and because a single lawsuit from a serious injury can exceed state minimums in weeks. The premium difference between $300,000 and $1,000,000 limits typically runs only $1,500 to $3,000 annually, making the upgrade practical for any contractor handling residential or commercial projects.

Extended Coverage for Weather-Related Failures

Your policy must include completed operations coverage with a three to five year extended reporting period, which protects you when a roof fails due to workmanship defects years after project completion. Louisiana’s weather patterns mean water intrusion claims surface long after your crew leaves the site, so this tail coverage is non-negotiable. Products liability within your general liability policy covers claims tied to roofing materials you install, protecting you if defective shingles or flashing cause damage to the structure. Add hurricane and windstorm endorsements specific to Louisiana’s coastal exposure, particularly if you operate in New Orleans, Metairie, or other high-risk zones.

Equipment Protection Through Inland Marine Insurance

Tools and equipment on job sites face constant theft and weather damage in Louisiana, so inland marine insurance becomes essential rather than optional. This coverage protects ladders, power tools, scaffolding, compressors, and roofing materials both in transit and on-site, covering theft, vandalism, and weather damage at rates typically ranging from 1 to 3 percent of your equipment’s replacement value annually. For a contractor with $50,000 in mobile equipment, inland marine runs $500 to $1,500 per year and eliminates the financial hit when a hurricane or theft wipes out your tools. Louisiana experiences approximately 3.2 major weather events per year according to FEMA data, with claim frequency running roughly 35 percent higher than the national average, so weather-related equipment loss is a realistic risk, not a theoretical one.

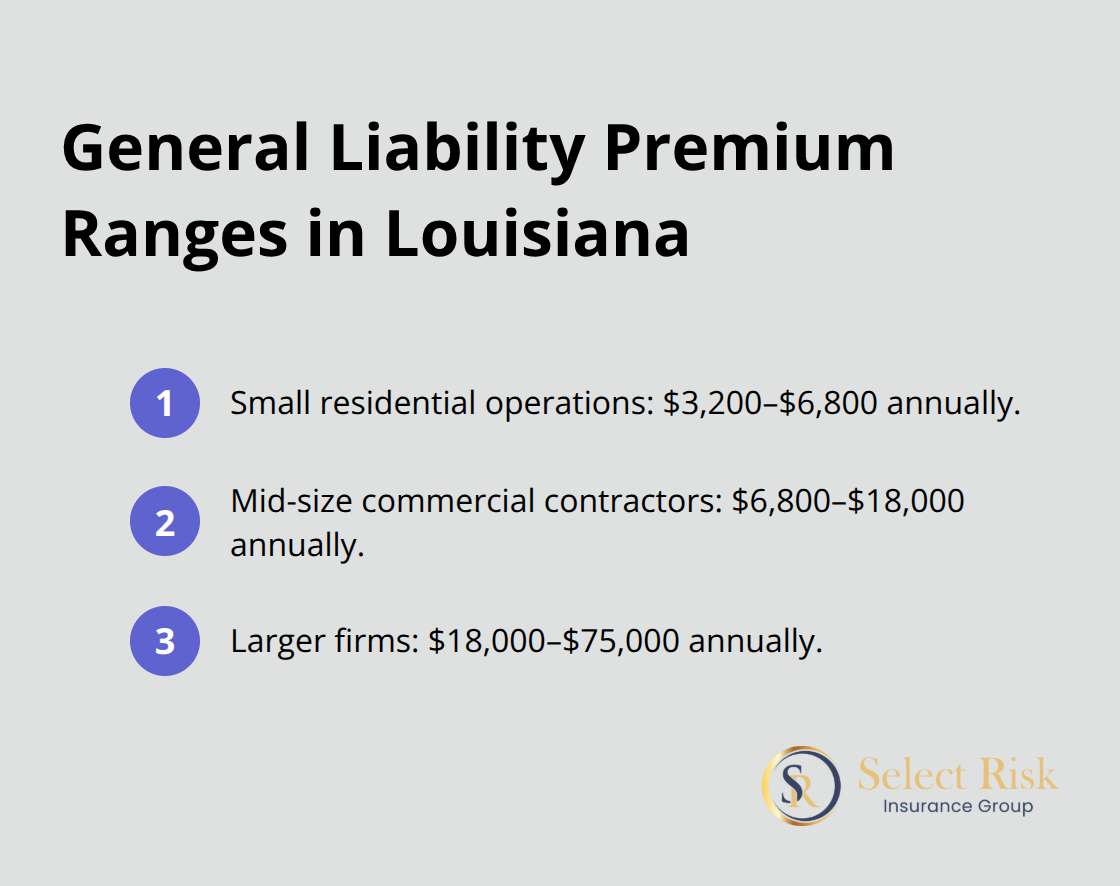

Understanding Premium Ranges and Rate Drivers

Premium ranges for standard limits of $1,000,000 per occurrence and $2,000,000 aggregate run $3,200 to $6,800 annually for small residential operations, $6,800 to $18,000 for mid-size commercial contractors, and $18,000 to $75,000 for larger firms. Location, claims history, and project type drive significant variation in your quote. Storm restoration work commands higher premiums because insurers price this work higher due to compressed timelines and elevated injury risk.

Request quotes from multiple carriers because Louisiana roofing rates vary substantially based on your specific project mix and operational footprint. Beyond general liability and equipment protection, roofing contractors in Louisiana also face specialized exposures that standard policies do not address-exposures that emerge from client contracts and the mobile nature of your operations.

Beyond General Liability: The Coverage Gaps Most Roofers Miss

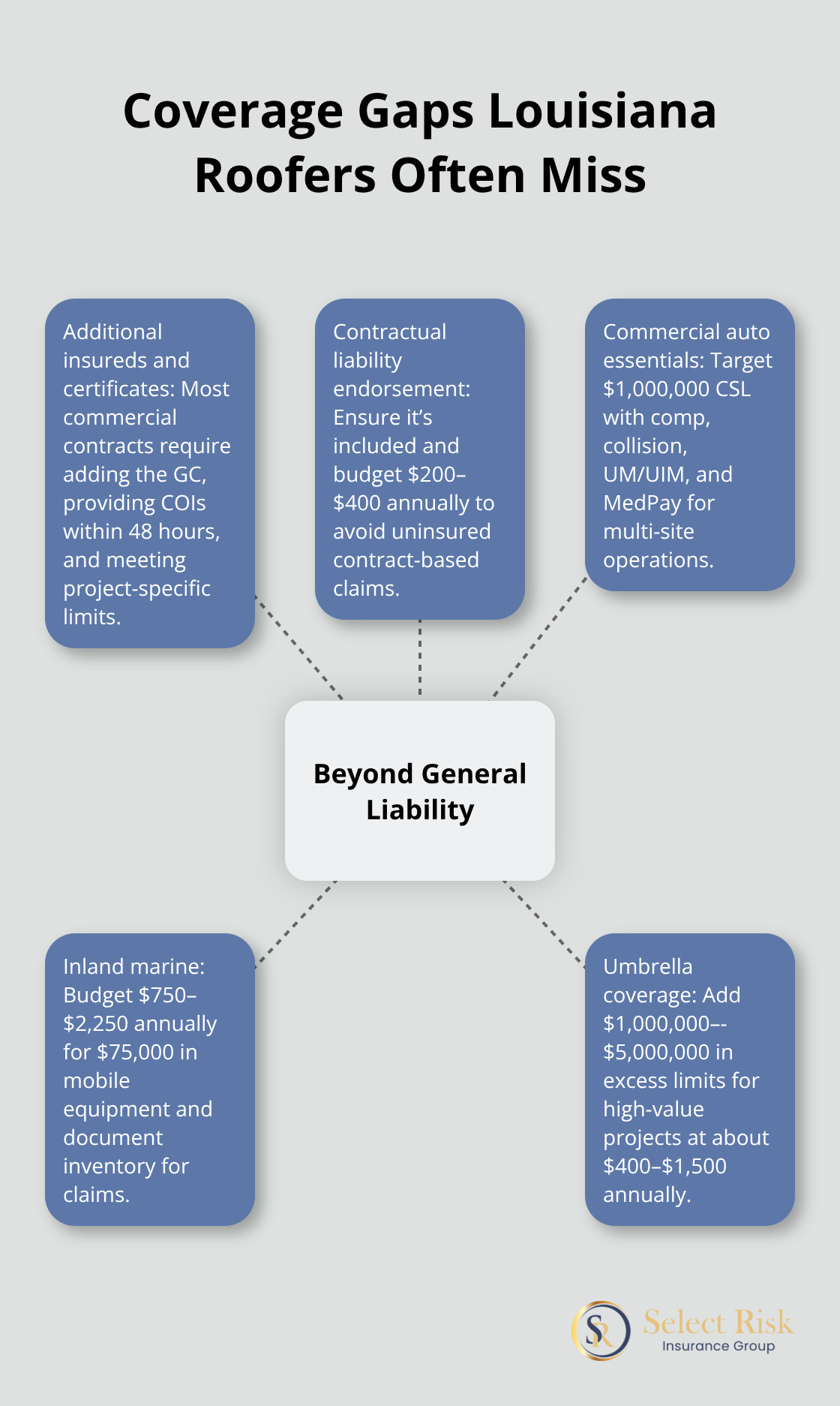

Contractual Liability and Additional Insured Requirements

Roofing contractors in Louisiana operate under client contracts that demand insurance coverage most standard policies don’t automatically provide. When a general contractor hires your crew for a commercial project, their contract almost always requires you to add them as an additional insured on your general liability policy, provide a certificate of insurance within 48 hours, and carry specific limits tied to the project value. Fail to meet these contractual demands and you lose the bid, or worse, you proceed without proper coverage and expose yourself to uninsured liability.

Contractual liability coverage sits inside your general liability policy and covers claims that arise from contract terms you’ve agreed to, but only if your policy explicitly includes this endorsement. Many contractors discover too late that their policy excludes contractual liability, leaving them personally liable for damages their insurance won’t cover. Request contractual liability coverage when you quote your general liability policy, and verify the endorsement appears on your declarations page before you sign any client contract. The cost to add this coverage runs negligible-typically $200 to $400 annually-yet it’s the difference between a covered claim and financial ruin.

Louisiana’s civil law system applies pure comparative fault rules, meaning you can face liability for your percentage of fault even if the property owner contributed to the damage. This legal environment makes contractual liability protection non-negotiable for any roofing business that bids jobs above $50,000.

Commercial Auto Insurance for Mobile Operations

Your roofing operation requires commercial auto insurance to protect the vehicles that transport your crew and equipment across Louisiana’s 52,000 square miles. Louisiana roofing contractors need at least $1,000,000 in combined single limit commercial auto coverage, which protects your company vehicles, employee-driven personal vehicles used for business, and hired or borrowed equipment. This coverage includes comprehensive and collision protection, uninsured and underinsured motorist coverage, and medical payments to occupants-all essential when your crew travels between multiple job sites.

Premium costs typically run $1,200 to $3,500 annually depending on your vehicle count, driver records, and annual mileage, far less than the cost of a single vehicle accident liability claim. A contractor with three work trucks and two employee vehicles might budget $2,000 to $3,000 per year for adequate protection.

Equipment Protection and Inventory Documentation

Inland marine insurance protects tools, equipment, and materials in transit and stored on job sites, covering theft, weather damage, and vandalism. A contractor with $75,000 in mobile equipment should budget $750 to $2,250 annually for inland marine coverage, a modest investment against the reality of Louisiana’s 3.2 major weather events per year. Document your equipment inventory with serial numbers and photographs, then provide this list to your inland marine insurer to support claims if loss occurs. Louisiana experiences claim frequency roughly 35 percent higher than the national average, so weather-related equipment loss is a realistic risk, not a theoretical one.

Umbrella Coverage for High-Value Contracts

Consider commercial umbrella insurance if you carry high-value contracts or operate in multiple locations, as umbrella policies provide an additional $1,000,000 to $5,000,000 in liability coverage above your primary policies at rates often lower than increasing primary limits. Umbrella coverage typically costs $400 to $1,500 annually and becomes cost-effective whenever your primary general liability limits approach the policy maximum through claims or contract requirements. This extra layer of protection shields your business when a single claim exceeds your underlying policy limits, a scenario that occurs more frequently on commercial projects valued above $250,000.

Final Thoughts

Roofing contractors in Louisiana operate in a high-risk environment shaped by weather exposure, regulatory demands, and client contract requirements. The best insurance for roofing companies in Louisiana combines workers’ compensation, general liability with extended coverage for completed operations, commercial auto protection, and equipment insurance tailored to your specific project mix and operational footprint. Skipping any of these core coverages leaves your business vulnerable to financial loss, license suspension, and personal liability that can exceed your company’s annual revenue.

Selecting the right insurance partner matters as much as selecting the right coverage types. You need an agency that understands Louisiana’s roofing market, knows the state’s licensing requirements under Act 239 and Act 422, and can quote multiple carriers to find competitive rates aligned with your risk profile. We at Select Risk Insurance Group work with a variety of financially sound insurance companies, which allows us to offer comprehensive coverage at competitive prices rather than locking you into a single carrier’s rates and terms.

Start by documenting your current coverage and identifying gaps, then review your general liability declarations page to confirm contractual liability and completed operations endorsements appear on your policy. Verify your workers’ compensation limits match your payroll projections and that your commercial auto coverage reflects your actual vehicle count. Contact Select Risk Insurance Group to discuss your roofing operation’s specific insurance needs and receive a customized proposal that protects your crew, your equipment, and your business against Louisiana’s unique exposures.

![Workers Comp for Roofers in Louisiana [A Complete Guide]](https://selectriskgroup.com/wp-content/uploads/emplibot/Workers-Comp-for-Roofers-in-Louisiana-_A-Complete-Guide__1767049923-80x80.jpeg)