How Much Does Roofing Insurance Cost in Louisiana?

Roofing damage in Louisiana happens fast, and so do insurance claims. The cost of roofing insurance in Louisiana varies widely depending on your roof’s age, location, and materials-but most homeowners don’t know where to start when comparing quotes.

At Select Risk Insurance Group, we help Louisiana homeowners understand what they’ll actually pay for roof coverage and how to reduce those premiums without sacrificing protection.

What Drives Roofing Insurance Costs in Louisiana

Roof Age and Condition Shape Your Premium

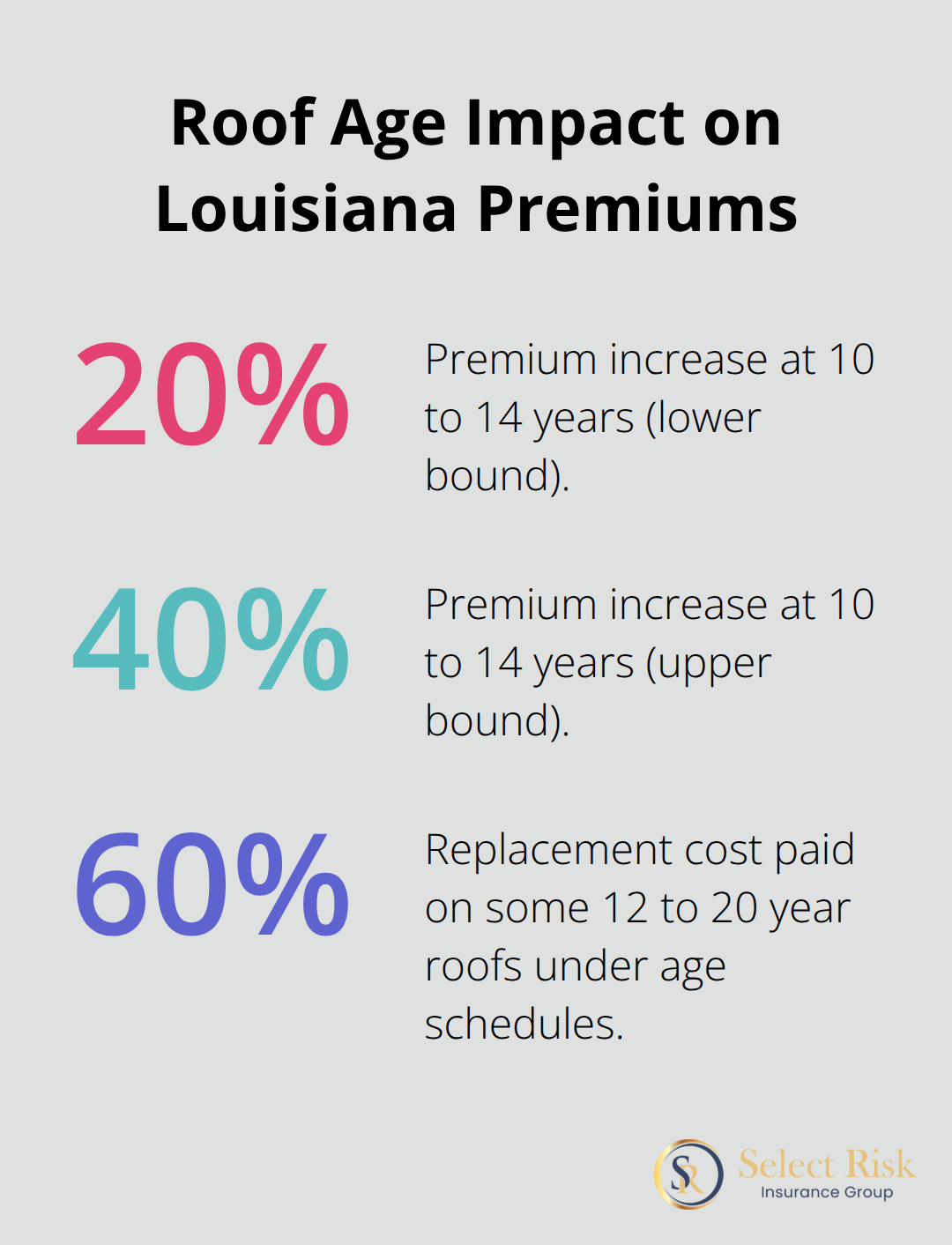

Your roof’s age is the single biggest factor insurers use to price your policy, and Louisiana carriers are more aggressive about it than most states. A roof that’s 10 to 14 years old typically sees a 20% to 40% premium increase compared to a newer roof, while roofs over 15 years old often receive Actual Cash Value payouts instead of Replacement Cost Value-meaning you absorb the depreciation when you file a claim. Insurers apply roof-payment schedules tied to age, sometimes paying only 60% of replacement costs for roofs in the 12 to 20-year range. If your roof shows poor condition with visible wear, cracked boots, or loose flashing, underwriting tightens further.

You should document your roof’s installation date with permits or contractor invoices and take dated photos of key areas at least annually. If your roof approaches 10 years old, a professional inspection protects you during renewal and shields you if an insurer questions the roof’s condition later.

Location and Weather Exposure Elevate Costs Significantly

Louisiana averages 3.2 major weather events per year, with hurricane season running June through November and peak activity hitting August through October. Coastal ZIP codes and parishes near the Gulf face much higher premiums because wind-driven rain and storm surge create genuine claim risk. Inland areas see lower premiums but still pay more than national averages due to the state’s overall weather profile. A homeowner in New Orleans or Terrebonne Parish will pay noticeably more than someone in Catahoula Parish, sometimes 30% to 50% higher depending on the exact location.

Claims History and Credit Score Impact Your Rate

Your claims history and credit score both influence what you’ll pay. Louisiana insurers pull both, and a single water damage or wind claim in the past three to five years can push premiums up 25% to 60%. Your credit score matters too-carriers treat it as a proxy for financial responsibility, and a lower score can add 10% to 20% to your annual cost. If you’ve had claims, focus on loss prevention going forward; if your credit needs work, that’s a separate financial priority, but it does affect insurance pricing.

Roofing Material Selection Offers Modest Savings

Type of roofing material affects pricing but less dramatically than age does. Asphalt shingles are the baseline; metal roofing and architectural shingles cost slightly more to insure but may qualify for small discounts on some policies. Impact-resistant materials certified to IBHS Fortified standards can reduce premiums by 5% to 15%, especially if you combine the upgrade with documentation and third-party certification. The real leverage with materials comes when you’re ready to replace your roof-that’s when upgrading to impact-resistant or Fortified standards makes financial sense for insurance savings and positions you well for your next renewal conversation.

What You’ll Actually Pay for Roofing Insurance in Louisiana

Louisiana Premiums Run Well Above the National Average

Louisiana homeowners pay significantly more for roofing coverage than most of the country. General liability insurance for roofing businesses costs $434 per month in Louisiana versus the national average of $389 per month, according to MoneyGeek’s December 2025 roofing insurance cost analysis. For homeowners policies, the gap widens even more when you factor in the state’s weather exposure and stricter underwriting. A typical homeowners insurance premium in Louisiana for a property with a roof aged 0 to 9 years in good condition ranges from $1,200 to $2,400 annually, but that number climbs sharply as your roof ages.

Roof Age Triggers Sharp Premium Jumps

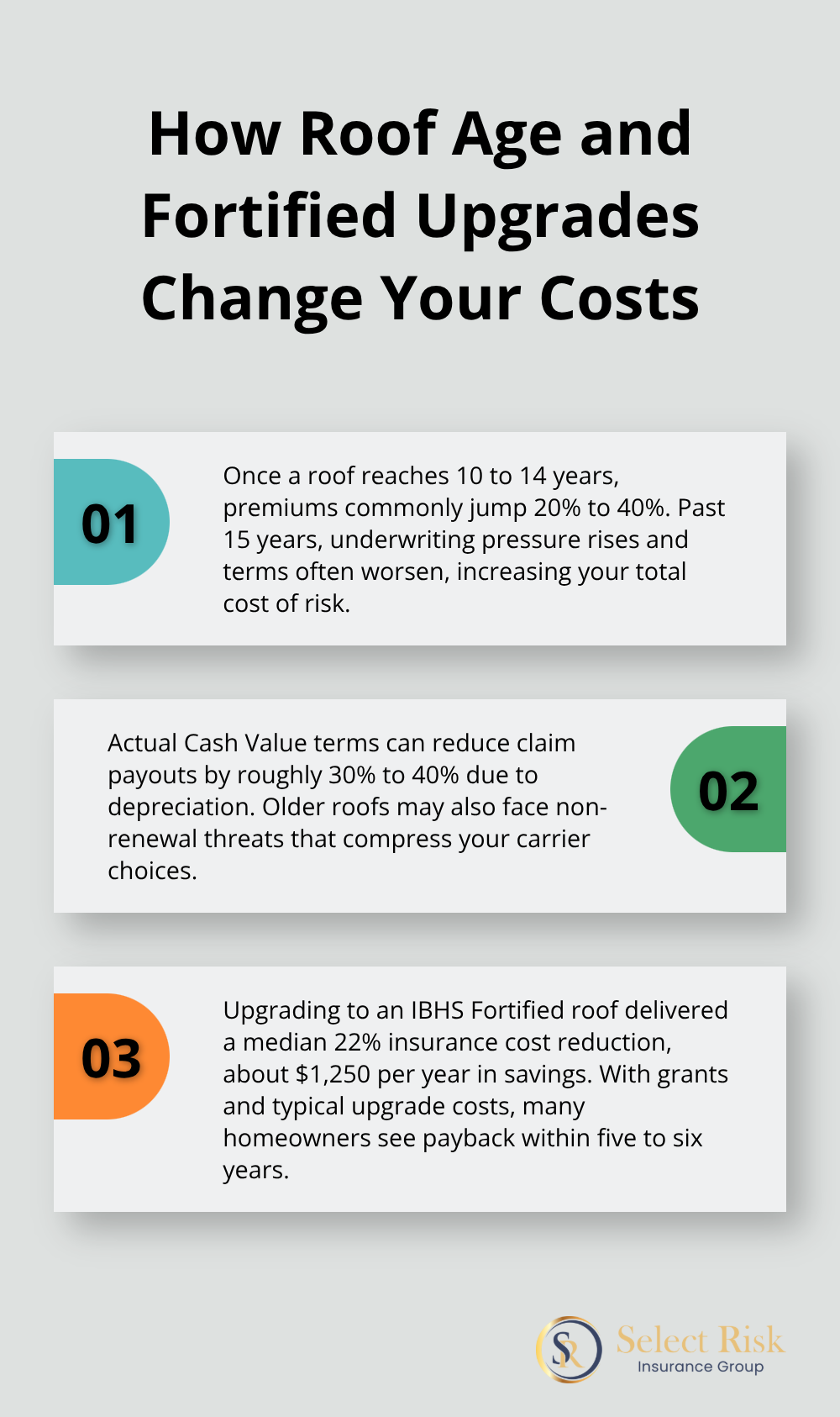

Once your roof hits 10 to 14 years, expect premiums to jump 20% to 40%. Roofs over 15 years old often trigger non-renewal threats or force carriers to apply Actual Cash Value terms, which means you lose 30% to 40% of your claim payout to depreciation. The Fortify Homes Program audit data reveals that homeowners who upgraded to IBHS Fortified roofs saw median insurance cost reductions of 22%, saving approximately $1,250 per year. That translates to annual premiums dropping from around $5,625 to $4,375 after certification, making the upgrade financially viable within 5 to 6 years when you factor in the $10,000 grant and typical upgrade costs of $16,229.

Additional Coverages Add Protection and Cost

Named-storm deductibles along the Gulf Coast typically run 2% to 5% of your Coverage A limit, which can mean $4,000 to $10,000 out of pocket on a $200,000 home before the insurer pays anything. Extended water-damage coverage and completed-operations liability endorsements add $150 to $400 annually but protect you against post-storm claims and long-tail water intrusion that shows up months after weather events. If you finance your home or carry a mortgage, your lender requires proof of adequate coverage, so you cannot skip these additions even if costs sting.

Smart Strategies Lower Your Total Cost

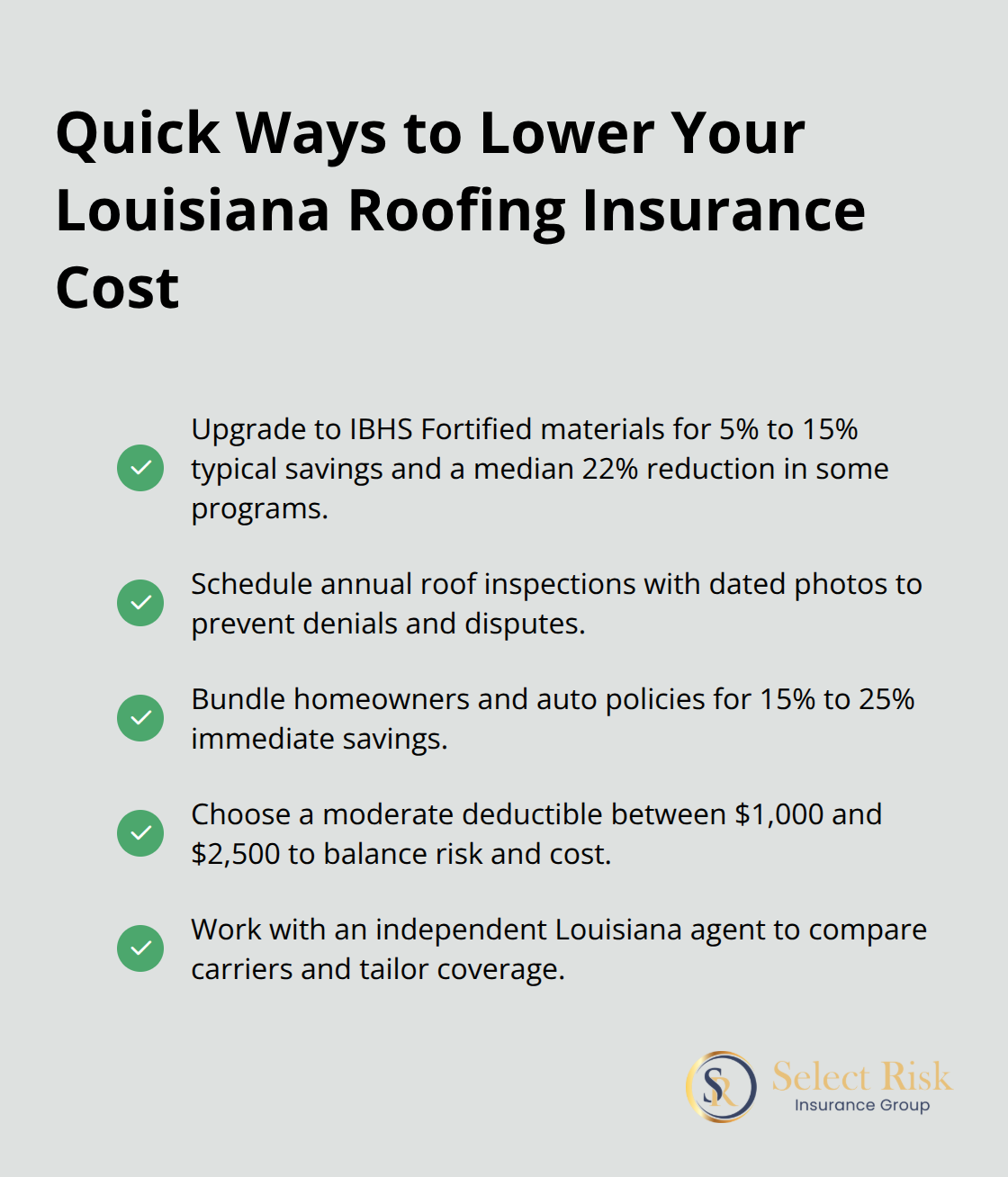

Louisiana’s weather risk-averaging 3.2 major events yearly-means you cannot safely use high deductibles without exposing yourself to real financial hardship during hurricane season. Try a moderate deductible of $1,000 to $2,500, bundle your homeowners and auto policies for 15% to 25% savings, and invest in annual roof inspections with documented photos. That documentation costs $150 to $300 but often prevents coverage denials and supports faster claim approval, paying for itself after a single claim. When you’re ready to explore your specific options and compare quotes from multiple carriers, working with an independent agent who understands Louisiana’s unique exposures makes all the difference in finding the right coverage at the right price.

How to Cut Your Louisiana Roofing Insurance Costs

Upgrade to Impact-Resistant Roofing Materials

Impact-resistant roofing materials certified to IBHS Fortified standards deliver real premium reductions-typically 5% to 15% depending on your carrier and location. The Fortify Homes Program audit data shows that homeowners who upgraded to Fortified roofs saw median insurance cost reductions of 22%, translating to savings of approximately $1,250 per year. The leverage only works if you complete the upgrade and obtain third-party certification; your insurer needs documented proof that your roof meets Fortified standards before applying any discount. When you factor in the $10,000 state grant and median upgrade costs of $16,229, your out-of-pocket cost drops to roughly $6,229, and the annual insurance savings of $1,250 recover that investment in under five years. If your roof approaches 10 years old or already exceeds it, upgrading to Fortified standards serves as a direct financial strategy for lowering your premiums.

Document Your Roof Maintenance and Inspections

Annual inspections protect your premium in two critical ways. First, they catch early damage-cracked boots, loose flashing, deteriorated counter-flashings-before claims occur, and that loss prevention history signals to underwriters that you take ownership seriously. Second, dated photos and inspection reports become your defense against wear-and-tear denials or coverage disputes; when a carrier questions whether your roof’s condition justifies renewal, you have proof. A professional spring inspection costs $150 to $300 but often prevents a $1,000-plus premium increase or non-renewal threat.

Bundle Policies for Immediate Savings

Bundling your homeowners and auto policies delivers 15% to 25% in savings according to industry data, and that discount applies immediately without waiting for a renewal cycle. Most carriers reward customers who consolidate multiple lines of coverage, making this one of the fastest ways to reduce your total insurance expense. The savings compound when you combine bundling with other cost-reduction strategies like higher deductibles or documented roof maintenance.

Work With an Independent Agent

An independent agent who represents multiple carriers and understands Louisiana’s weather exposures can compare how different insurers price your specific risk profile, identify which carriers reward Fortified upgrades or strong inspection records, and negotiate deductibles and limits that match your actual exposure rather than pushing you toward overpriced standard packages. Select Risk Insurance Group, based in Lafayette, represents a variety of financially sound insurance companies, allowing them to offer comprehensive coverage at competitive prices tailored to Louisiana homeowners’ unique needs.

Final Thoughts

Your roof’s age, location, and condition drive the cost of roofing insurance in Louisiana more than almost any other factor. Weather exposure pushes premiums higher here than across most of the country, and carriers apply strict underwriting standards that reward documentation and proactive maintenance. You control several levers to reduce what you pay: upgrading to impact-resistant materials cuts premiums by 5% to 15%, annual inspections with dated photos prevent coverage disputes, and bundling policies delivers 15% to 25% in immediate savings.

Getting an accurate quote requires more than plugging numbers into an online form. Your specific roof age, location within Louisiana, claims history, and the exact coverage limits your lender requires all shape your final premium. Comparing quotes from multiple carriers reveals how differently insurers price Louisiana’s weather risk, and that variation can mean hundreds of dollars in annual savings.

Gather your roof’s installation date, take current photos of key areas, and pull your recent claims history so you can provide accurate information to agents. Visit Select Risk Insurance Group to connect with their team in Lafayette and receive personalized quotes that reflect Louisiana’s unique insurance landscape.

![Best Insurance for Roofing Companies in Louisiana [2025]](https://selectriskgroup.com/wp-content/uploads/emplibot/Best-Insurance-for-Roofing-Companies-in-Louisiana-_2025__1766790632-80x80.jpeg)