Roofing Contractor Insurance Requirements in Louisiana

Running a roofing business in Louisiana means navigating specific insurance requirements that protect your company, employees, and clients. Missing the right coverage can expose you to serious financial and legal risks.

At Select Risk Insurance Group, we help roofing contractors understand exactly what roofing contractor insurance requirements Louisiana mandates. This guide breaks down the coverage you need and the gaps most contractors overlook.

What Louisiana Actually Requires for Roofing Contractor Insurance

Louisiana enforces strict insurance mandates for roofing contractors, and the state has become increasingly aggressive about enforcement. The Louisiana State Licensing Board for Contractors performs random insurance audits that can suspend your license on the spot if you fail to maintain continuous coverage with no gaps during your license period. This isn’t a suggestion-it’s a legal requirement with teeth.

Minimum Coverage Amounts by Project Type

For residential roofing work, you must carry a minimum of $100,000 in general liability insurance and workers’ compensation coverage. Commercial roofing contractors operating on projects valued at $50,000 or more face steeper requirements: Louisiana mandates a minimum of $300,000 per occurrence and $600,000 aggregate in general liability, plus $100,000 in property damage coverage. Many contractors in Louisiana carry $1,000,000 per occurrence and $2,000,000 aggregate, which is the safer market standard and what most project owners actually expect to see on your Certificate of Insurance.

Workers’ Compensation and Payroll Costs

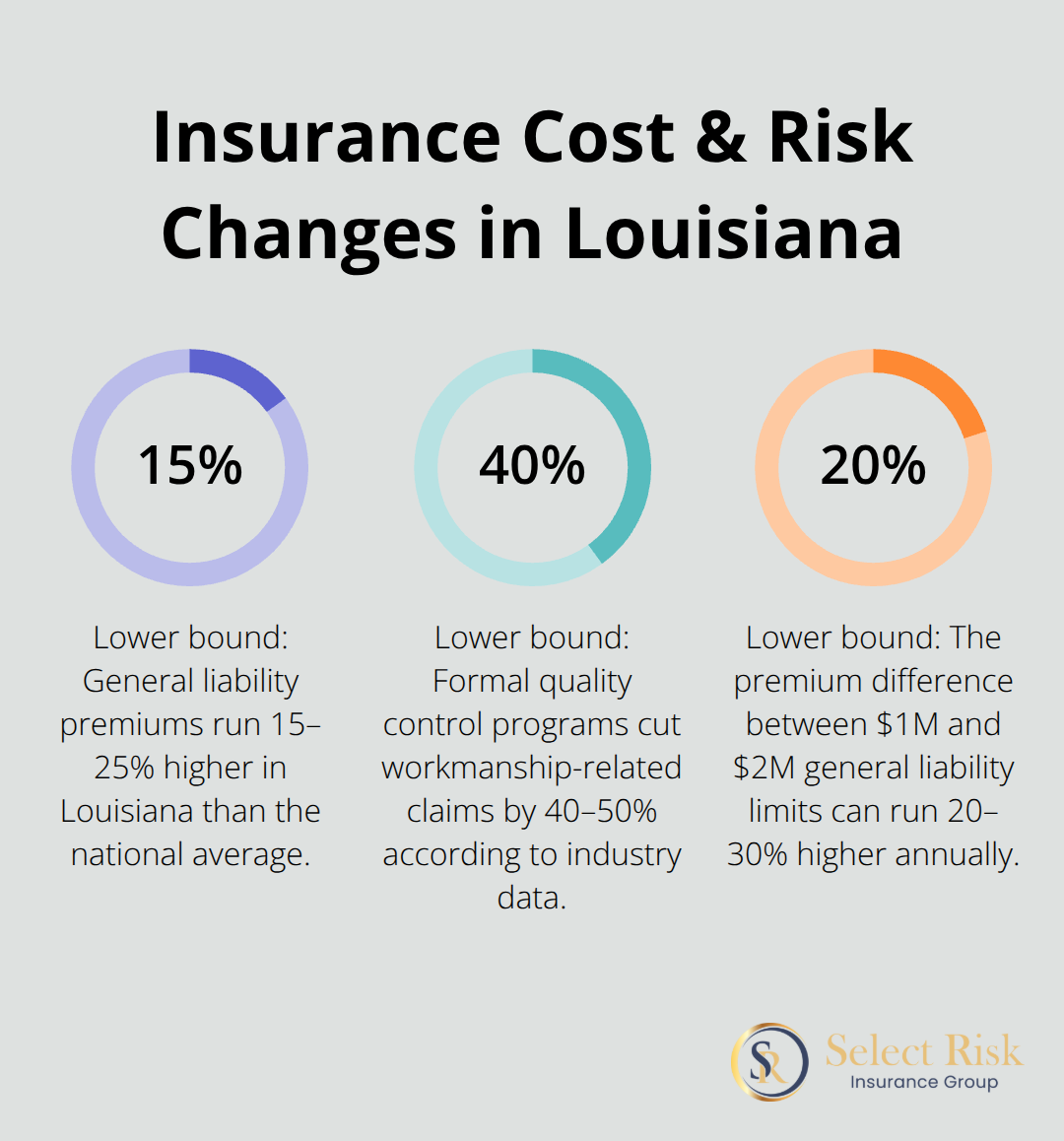

Workers’ compensation is mandatory if you have employees-no exceptions, no workarounds with 1099s if those workers resemble employees in practice. The annual cost typically ranges from $400 to $3,000 depending on your payroll size. General liability premiums run 15–25% higher in Louisiana than the national average due to hurricane exposure and a litigious environment, so budget $3,200 to $6,800 annually for small residential operations and $6,800 to $18,000 for mid-size commercial work.

License Approval and Proof of Coverage

Starting January 1, 2026, Louisiana introduces a new residential roofing license classification under Act 422, and anyone who bids on or performs residential roofing work valued at $7,500 or more must hold this license or an existing residential construction license. The licensing board requires you to submit proof of general liability and workers’ compensation coverage via email to insurance@lslbc.louisiana.gov before your license receives approval. Certificates of Insurance must remain current throughout your license period-no gaps allowed.

Hurricane Exposure and Required Endorsements

Louisiana’s hurricane-prone climate creates distinct liability exposures; FEMA reports an average of 3.2 major weather events per year during the June 1–November 30 hurricane season, which means your policy must include hurricane and windstorm endorsements. Completed operations coverage is also essential because claims can arise months or even years after a project ends. The Louisiana State Licensing Board requires endorsements for additional insured status, primary and non-contributory language, and waiver of subrogation on most commercial projects.

Public and Federal Project Requirements

Public projects and contracts with local parishes or municipalities often push general liability requirements to $2–$5 million, so verify specific requirements before you bid. Federal projects introduce Miller Act bonding requirements for contracts over $150,000, plus Defense Base Act workers’ compensation if you work on military installations. Understanding these escalating requirements before you submit a bid prevents costly coverage gaps and protects your ability to complete the work.

What Coverage You Actually Need to Operate Legally

General Liability: The Foundation of Your Protection

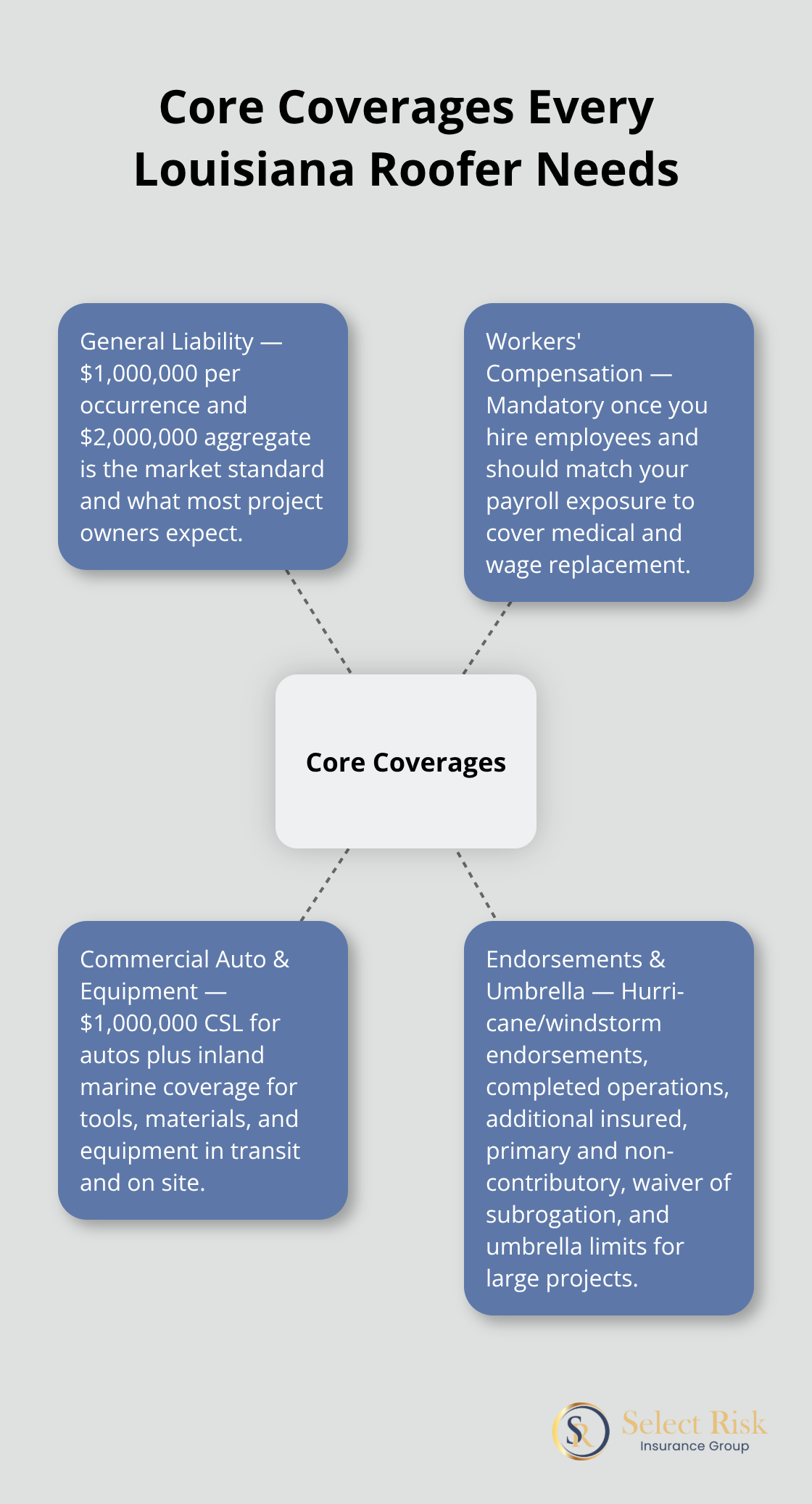

General liability insurance protects your business when someone gets injured on a job site or your work damages a client’s property. Louisiana roofing contractors commonly carry $1,000,000 per occurrence and $2,000,000 aggregate-this is the standard that project owners expect to see on your Certificate of Insurance. Anything below this puts you at a competitive disadvantage and signals to clients that you’re underinsured.

The National Association of Roofing Contractors emphasizes that completed operations coverage is non-negotiable for roofing work because claims surface months or years after a project finishes. Your policy must also include hurricane and windstorm endorsements given Louisiana’s climate, where FEMA reports an average of 3.2 major weather events annually. Additional insured endorsements, primary and non-contributory language, and waiver of subrogation clauses are contractual requirements on most commercial jobs. Without these endorsements, clients will reject your bid or demand you add them at your expense during the project timeline.

Workers’ Compensation and Equipment Protection

Workers’ compensation covers medical treatment, rehabilitation, and wage replacement for employees injured on the job, and Louisiana makes this mandatory the moment you hire your first employee. The annual cost ranges from $400 to $3,000 depending on payroll size, making it one of your most predictable business expenses. Property and equipment coverage through inland marine insurance protects your roofing tools, power tools, ladders, scaffolding, safety gear, and materials both in transit and on site against theft, vandalism, and damage.

Commercial Auto and Umbrella Coverage

Commercial auto insurance with limits of $1,000,000 Combined Single Limit covers bodily injury and property damage when you use company vehicles for work. Comprehensive and collision coverage protects against theft and damage to the vehicles themselves. For high-value commercial projects, umbrella policies provide additional liability limits beyond your primary coverage and offer broad protection that covers legal defense costs, often meeting contractual liability requirements from clients at a lower cost than raising your base limits.

Securing these coverages upfront prevents gaps that could suspend your license or leave you personally liable for claims that should have been covered. The next section examines the specific coverage gaps that most Louisiana roofing contractors overlook-and how those oversights can derail your business.

Common Coverage Gaps That Cost Louisiana Roofing Contractors Money

The General Liability Trap

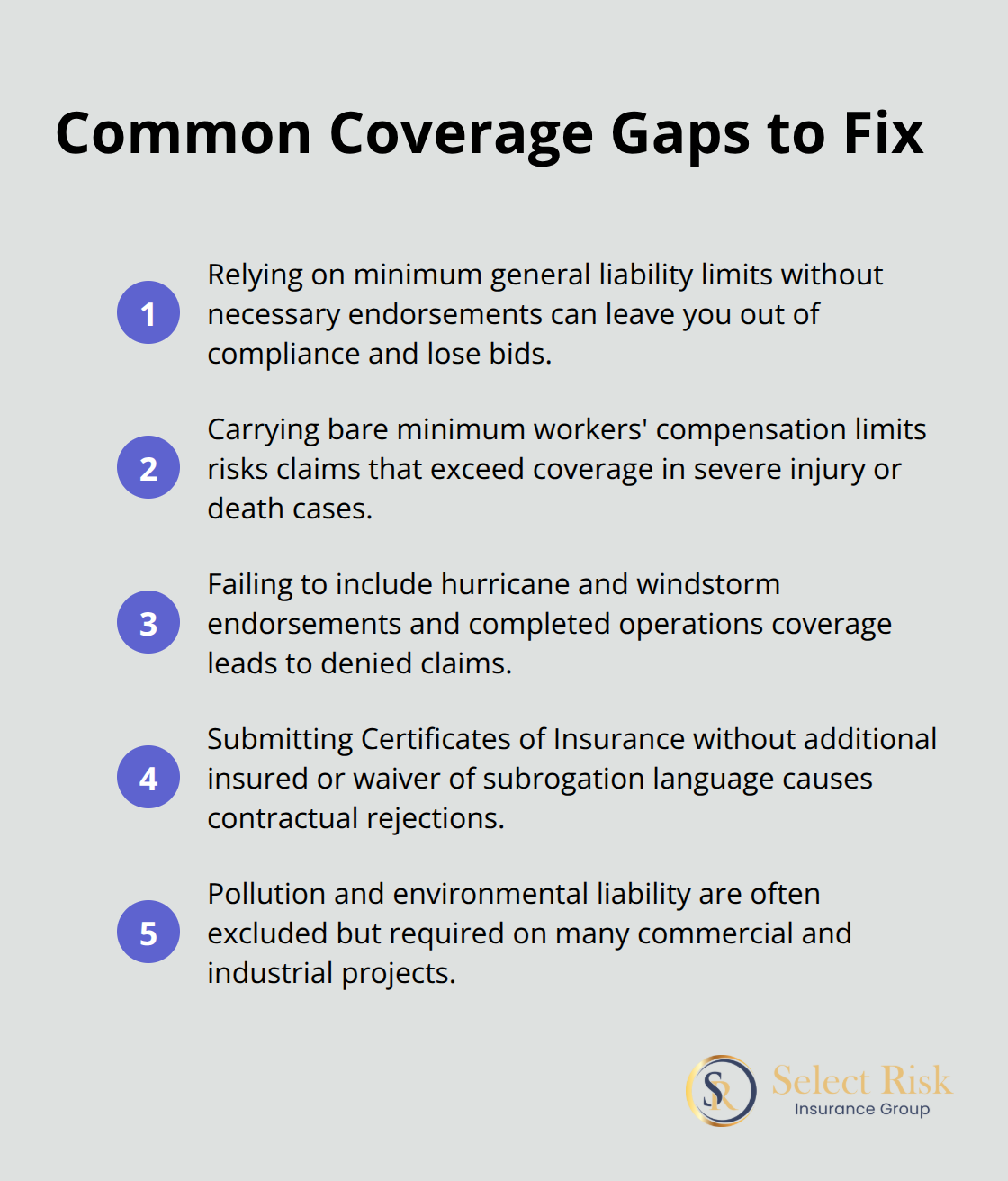

Most Louisiana roofing contractors carry general liability insurance that meets the minimum state requirement, then stop and assume they’re protected. The National Association of Roofing Contractors found that formal quality control programs cut workmanship-related claims by 40–50%, yet contractors who skip documented safety protocols and comprehensive endorsements pay higher premiums and lose bids to better-insured competitors. Your general liability limits sound adequate until a high-value commercial project arrives and the contract requires $2–5 million in coverage-this happens regularly on public and municipal jobs in Louisiana.

You then face a choice: decline the work, scramble to add umbrella coverage mid-bid, or operate outside your coverage limits and expose yourself personally to liability.

If you regularly bid on commercial work or public contracts, carry $2–5 million in general liability from the start. The premium difference between $1 million and $2 million coverage runs 20–30% higher annually, but losing a single mid-size project costs far more.

Workers’ Compensation Limits That Fall Short

You must carry workers’ compensation if you have employees, and the state conducts random audits that can suspend your license immediately for non-compliance. However, many contractors carry the bare minimum $500,000/$500,000/$500,000 limits and assume that covers their exposure. Louisiana’s litigious environment and high injury rates in roofing work mean claims often exceed standard limits, especially when permanent disability or death occurs on a job site.

Missing Endorsements and Specialized Coverage

Hurricane and windstorm endorsements aren’t optional in Louisiana, where FEMA documents an average of 3.2 major weather events annually, yet contractors frequently discover their standard policies exclude wind damage during claims. Completed operations coverage lapses when contractors assume their policy ends the day they finish a project, then face claims for roof failures months or years later when coverage has already expired.

Additional insured endorsements, waiver of subrogation clauses, and primary and non-contributory language are contractual requirements on most commercial jobs, but contractors sometimes submit Certificates of Insurance without these endorsements. Clients then reject bids or demand expensive additions during the project. Pollution liability and contractor liability for environmental damage are increasingly common requirements on commercial and industrial projects, yet most basic policies exclude them entirely.

How to Close the Gaps

An independent agency audits your coverage against your actual project types and contract requirements, then builds your policy to match reality instead of just meeting minimums. This approach prevents the costly oversights that derail roofing businesses in Louisiana.

Final Thoughts

Running a roofing business in Louisiana requires more than meeting minimum insurance thresholds. The roofing contractor insurance requirements Louisiana mandates have tightened significantly, especially with the new residential roofing license classification taking effect January 1, 2026, and mandatory permitting starting August 1, 2025. Contractors who treat insurance as a checkbox rather than a strategic business tool consistently lose bids, face license suspensions, or discover mid-project that their coverage falls short of contract requirements.

The essential coverage you need includes general liability at $1,000,000 per occurrence and $2,000,000 aggregate, workers’ compensation matching your payroll size, commercial auto insurance with $1,000,000 Combined Single Limit, and specialized endorsements for hurricane exposure, completed operations, and additional insured status. These aren’t suggestions from industry groups-they represent the practical minimums that Louisiana project owners expect and that protect your business from the specific risks roofing work creates in this state.

An independent insurance agency represents multiple carriers and understands Louisiana’s regulatory landscape, allowing them to build policies that match your business instead of forcing you into standard packages that miss critical exposures.

If you’re uncertain whether your current policies meet Louisiana’s requirements or whether you’re carrying the right limits for your project mix, contact Select Risk Insurance Group today for a comprehensive review. We audit your coverage, identify gaps before they cost you money or licenses, and secure competitive rates across multiple carriers to align your insurance with your real-world operations.