Insurance for Small Construction Companies in Louisiana

Small construction companies in Louisiana face unique challenges that require specialized insurance protection. From hurricane season to complex job site risks, your business needs comprehensive coverage.

We at Select Risk Insurance Group understand the specific insurance needs of Louisiana contractors. This guide covers essential small construction company insurance Louisiana options and practical strategies to protect your business while managing costs effectively.

What Insurance Coverage Do Small Construction Companies Need?

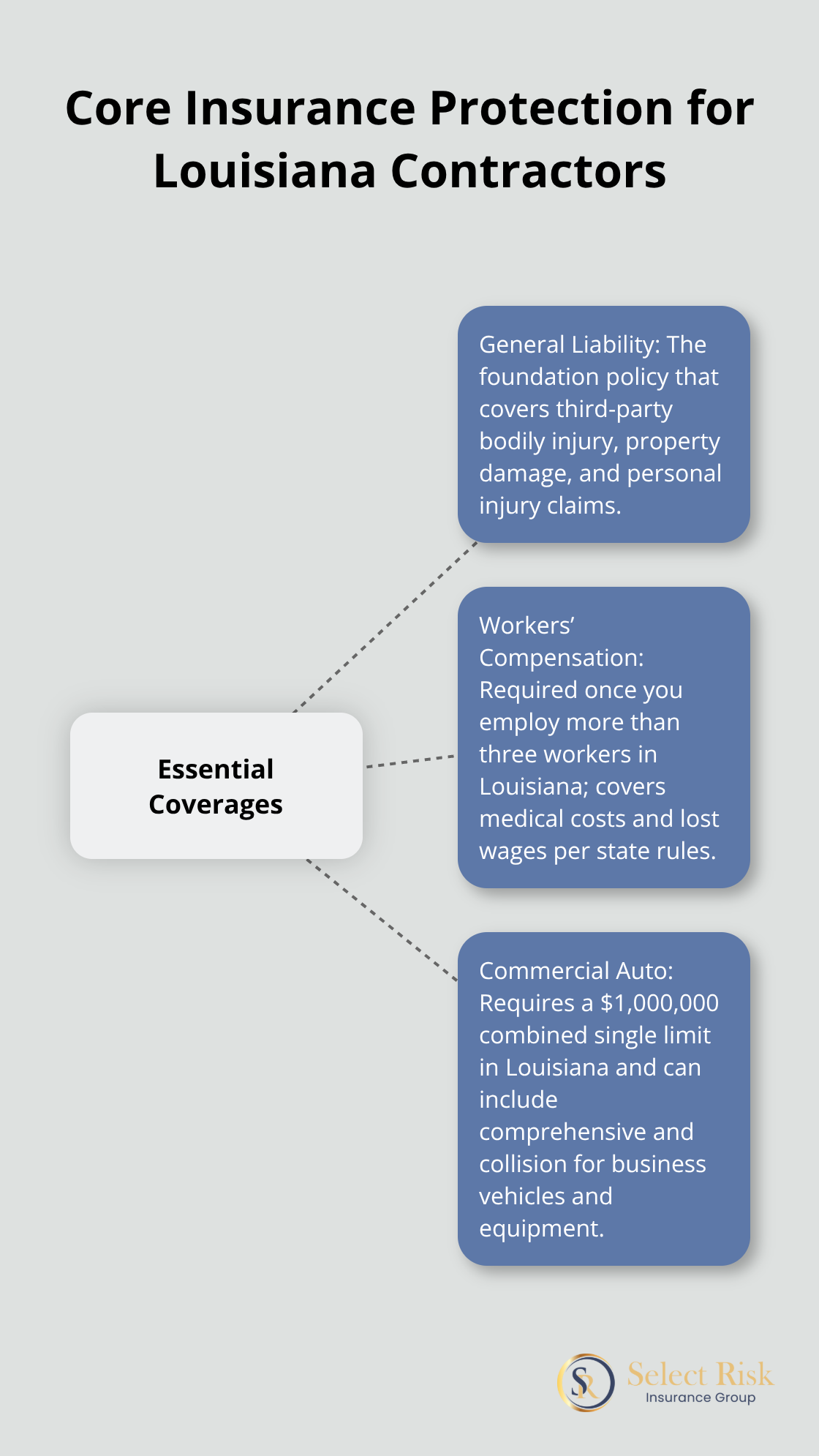

Louisiana contractors must secure three non-negotiable insurance types to operate legally and protect their businesses. General liability insurance stands as the foundation, with Louisiana requiring this essential coverage for licensed contractors. This coverage protects against property damage and bodily injury claims that can devastate small contractors financially. The average annual cost ranges from $500 to $1,500, but this investment prevents lawsuits that could bankrupt your company overnight.

General Liability Insurance Requirements

General liability insurance covers legal defense costs and damages from bodily injury, property damage, and personal injury claims. Louisiana contractors face strict minimum coverage requirements that protect both your business and clients. Claims in the construction industry have risen significantly over the past five years, making adequate coverage more important than ever. Companies without proper liability protection risk losing their business license and face personal financial liability for damages.

Workers’ Compensation Requirements

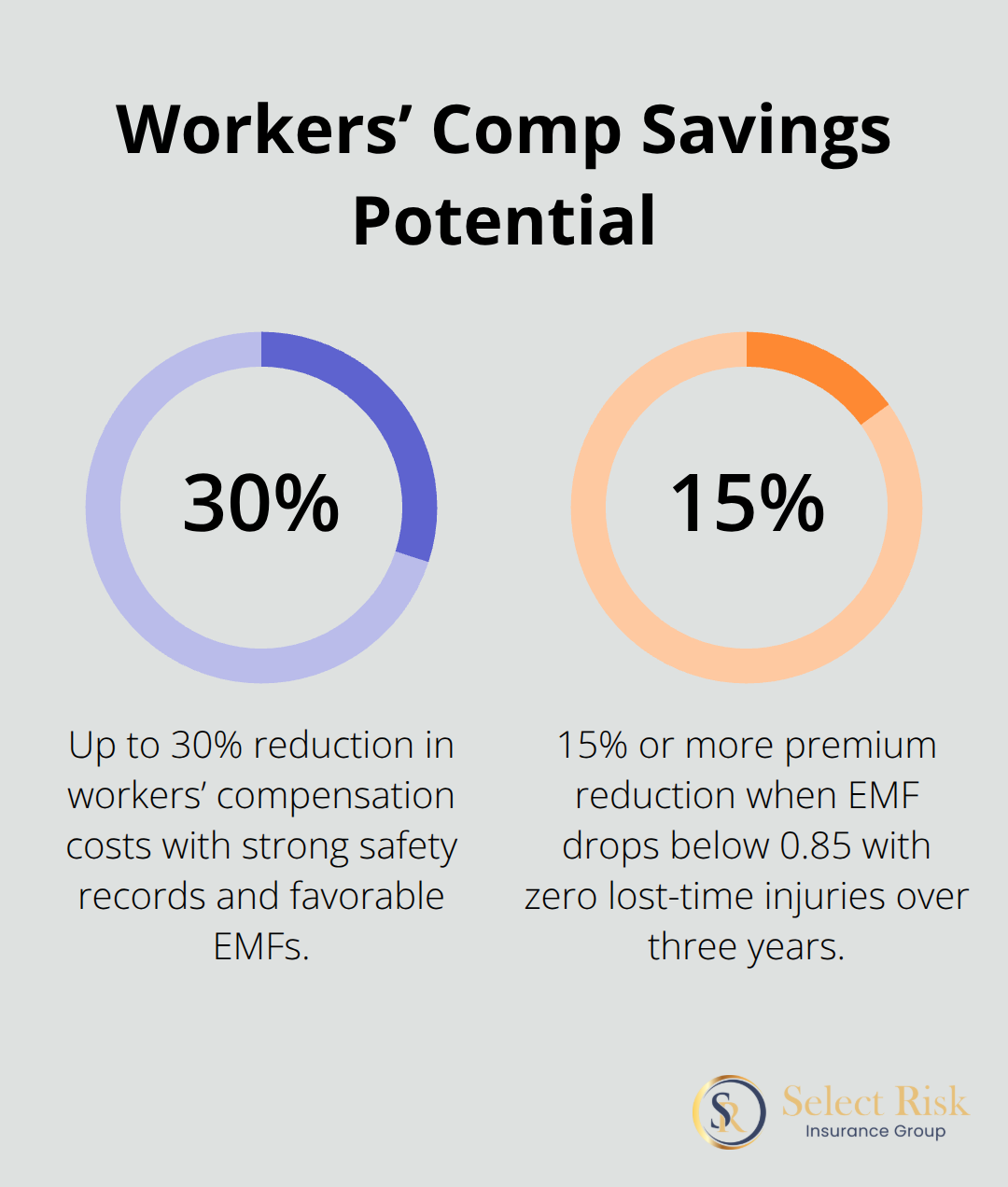

Workers’ compensation insurance becomes mandatory in Louisiana once you employ more than three workers. The state requires you to report workplace injuries to your carrier within 24 hours, making prompt coverage essential. Premiums vary significantly based on your industry classification and claims history, with high-risk construction activities facing steeper rates. Companies with strong safety records can reduce these costs by up to 30% through experience modification factors (EMFs that reward safe work practices).

Commercial Vehicle Protection

Commercial auto insurance protects any vehicle used for business purposes, requiring a $1,000,000 combined single limit for bodily injury and property damage in Louisiana. This includes owned, leased, and rented vehicles that transport equipment to job sites. The coverage extends beyond basic liability to include comprehensive and collision protection for expensive construction vehicles and equipment.

These three insurance types form the foundation of protection, but Louisiana’s unique environmental challenges create additional risks that smart contractors address proactively.

How Do You Protect Your Louisiana Construction Business From Risks?

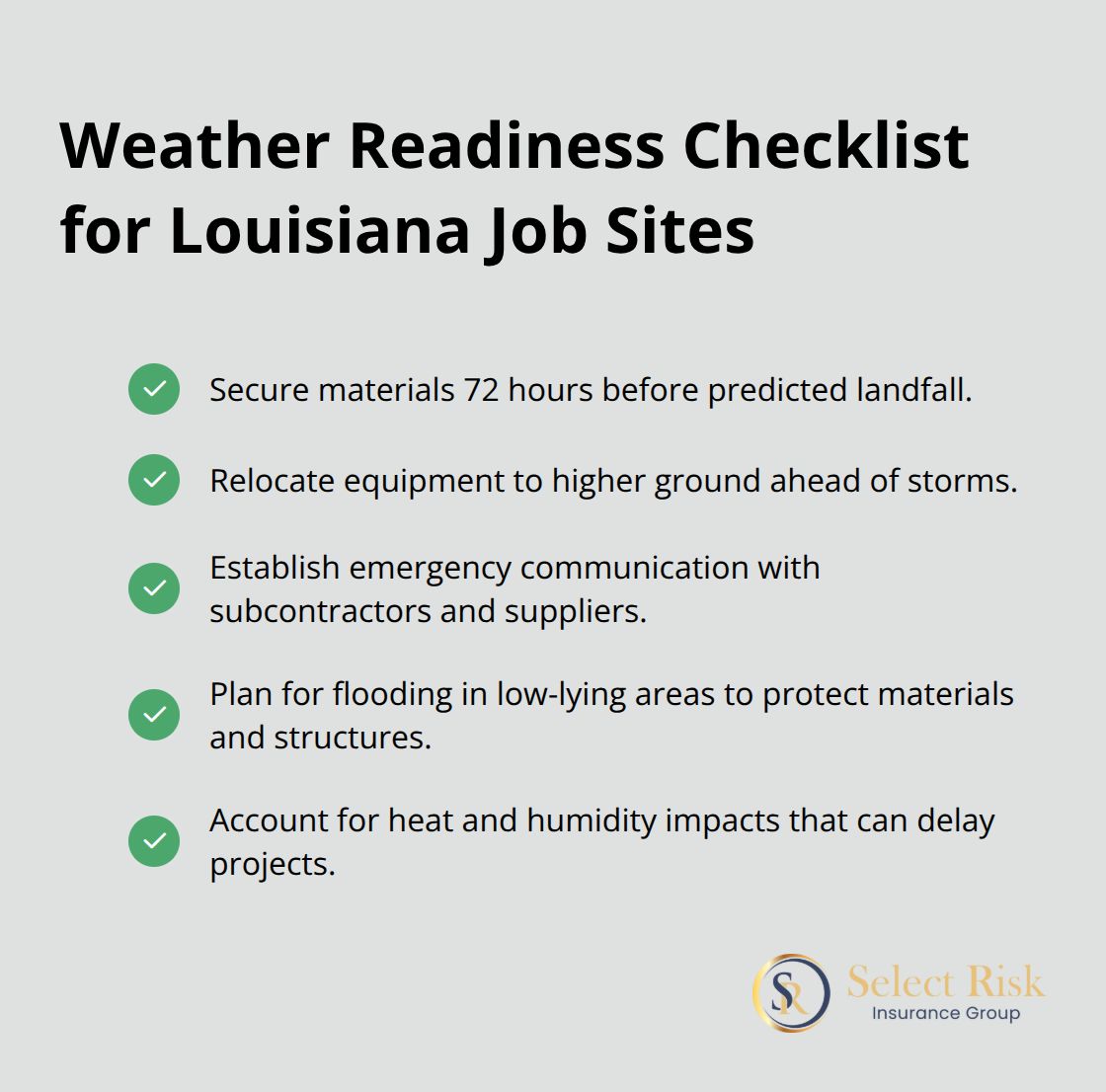

Louisiana construction companies face relentless environmental challenges that can destroy projects and bankrupt businesses. Hurricane season runs from June through November, with peak activity in August and September that threatens every job site across the state. From 1980-2024, there were 106 confirmed weather/climate disaster events with losses exceeding $1 billion each to affect Louisiana. Companies near coastal areas pay higher insurance premiums due to these elevated risks, but smart contractors implement comprehensive weather preparedness strategies that reduce both premiums and project delays.

Weather-Related Risk Management

Hurricane protocols must include material security 72 hours before predicted landfall, equipment relocation to higher ground, and emergency communication systems with all subcontractors and suppliers. Severe flooding affects low-lying areas throughout Louisiana, which damages construction materials and incomplete structures regularly. High temperatures and humidity negatively impact construction materials, which leads to project delays and additional costs that insurance may not cover.

Job Site Safety Program Implementation

Construction safety programs directly impact your bottom line through reduced workers’ compensation claims and lower experience modification factors. The Louisiana Workforce Commission reports that companies with structured safety training programs experience fewer workplace injuries compared to those without formal protocols. Daily safety briefings, mandatory hard hat and safety harness policies, and weekly equipment inspections create measurable results that insurance carriers recognize through premium discounts for companies with excellent safety records.

Louisiana License and Bond Compliance

Louisiana contractors must maintain active licenses through the State Licensing Board for Contractors, with residential contractors requiring $15,000 bonds and commercial contractors needing $50,000 bonds minimum. Your license status directly affects insurance availability and pricing, as carriers view unlicensed contractors as unacceptable risks. Clean disciplinary records with the licensing board prevent insurance complications and keep your business eligible for preferred carrier programs that offer better rates and coverage options.

These risk management strategies form the foundation for cost-effective insurance solutions that protect your business while maximizing your budget. General liability insurance serves as the foundation of business protection, covering third-party claims for bodily injury, property damage, and legal fees. Professional liability insurance covers mistakes in your work, such as incorrect electrical installations that cause damage weeks later.

How Can Small Construction Companies Save Money on Insurance?

Smart construction companies in Louisiana save 15-25% annually when they bundle general liability, workers’ compensation, and commercial auto insurance with a single carrier. Insurance companies offer substantial multi-policy discounts because bundled accounts generate higher retention rates and lower administrative costs. The National Association of Insurance Commissioners reports that businesses with bundled policies experience faster claims processing and simplified billing, which reduces your administrative burden significantly. Companies that maintain all coverage with one carrier also receive priority service during hurricane season when claims volume spikes across Louisiana.

Bundle Multiple Policies for Maximum Savings

Multi-policy discounts reward contractors who consolidate their insurance needs with one carrier. Carriers prefer bundled accounts because they reduce customer acquisition costs and increase policy retention rates. Louisiana construction companies that bundle three or more policies typically receive discounts of 10-20% on their total premiums. This approach also simplifies your renewal process and creates a single point of contact for all claims and policy questions.

Independent Agents Deliver Better Results

Independent agents represent multiple insurance carriers, which gives you access to competitive quotes that captive agents cannot provide. Price differences of 20-40% for identical coverage limits appear regularly when you compare quotes from three different carriers. Independent agents understand Louisiana’s unique construction risks and can match your specific needs with carriers that specialize in construction coverage. The Louisiana Department of Insurance recommends that contractors obtain multiple quotes annually because carrier pricing strategies change frequently, and companies that switch carriers every 2-3 years save an average of $3,000 annually on premiums.

Claims Management Controls Your Premiums

Your experience modification factor determines workers’ compensation premiums based on your claims history compared to similar Louisiana construction companies. Companies with zero lost-time injuries over three years can achieve EMF ratings below 0.85, which reduces premiums by 15% or more. Document every incident immediately, implement return-to-work programs for injured employees, and challenge incorrect claim classifications that inflate your EMF. On-the-job safety and health protection remains a top priority, and contractors who actively manage their safety records see measurable premium reductions within 12-18 months after they implement comprehensive safety programs.

Final Thoughts

Small construction company insurance Louisiana requirements focus on three essential coverage types that protect your business from financial disaster. General liability insurance protects you from property damage and bodily injury claims, while workers’ compensation coverage becomes mandatory once you employ more than three workers. Commercial auto insurance protects your vehicles and equipment with the required $1,000,000 combined single limit.

Annual policy reviews prevent coverage gaps that develop as your business grows and Louisiana’s insurance landscape changes. The National Association of Insurance Commissioners recommends yearly policy assessments to align your coverage with current business operations and risk exposure. Companies that review their policies annually find cost-saving opportunities and coverage improvements that protect their bottom line.

Your next step involves partnering with experienced insurance professionals who understand Louisiana’s unique construction risks. We at Select Risk Insurance Group work with multiple insurance companies to provide comprehensive coverage at competitive prices for Louisiana contractors. Our team specializes in building relationships through personalized insurance solutions that protect your construction business from hurricane season through year-round operations.