Why Every Handyman in Louisiana Needs Insurance

Louisiana handymen face serious legal and financial risks when operating without proper insurance coverage. State regulations require specific coverage types, and violations can result in hefty penalties.

At Select Risk Insurance Group, we see contractors lose thousands in lawsuits that handyman insurance Louisiana policies could have prevented. The right coverage protects your business and livelihood.

What Are Louisiana’s Legal Requirements for Handyman Insurance

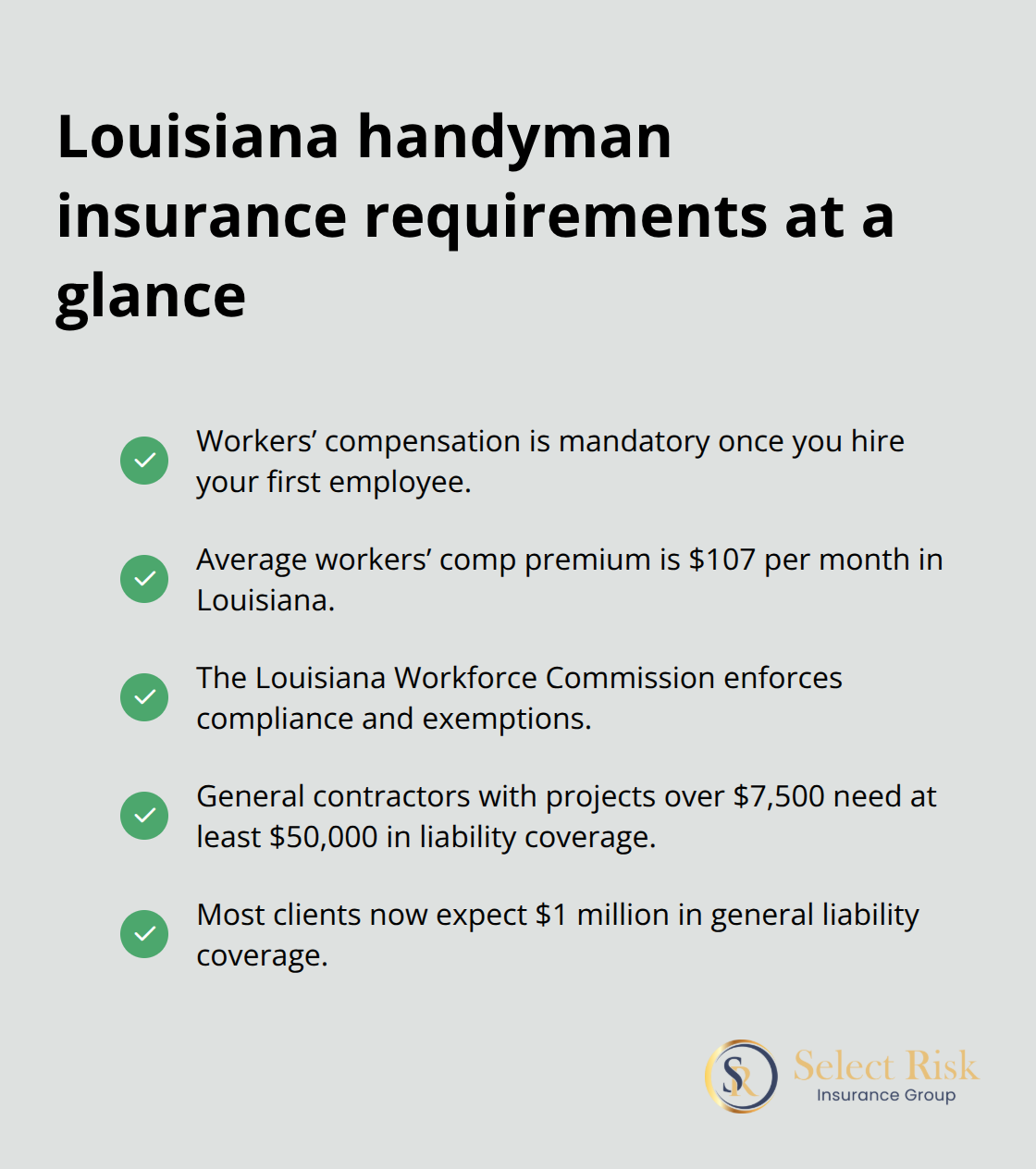

Louisiana handymen must comply with strict state insurance requirements that vary based on their business structure and services. Workers’ compensation insurance becomes mandatory when you hire your first employee, with Louisiana averaging $107 monthly for this coverage according to recent industry data. The Louisiana Workforce Commission enforces these requirements and ensures that both workers and business owners maintain compliance with policies or exemptions. General contractors who perform work valued over $7,500 must maintain minimum liability coverage of $50,000, though most clients now expect $1 million in coverage.

Municipal Requirements Add Another Layer of Complexity

Individual parishes and municipalities impose additional insurance requirements beyond state mandates. New Orleans requires handymen to carry $300,000 in general liability coverage for permits, while Baton Rouge mandates $500,000 for certain commercial projects. These local requirements change frequently, and handymen must verify current standards with each jurisdiction where they work. Many parishes also require certificate of insurance submission before permit approval (which creates delays for uninsured contractors).

Financial Penalties Can Destroy Your Business

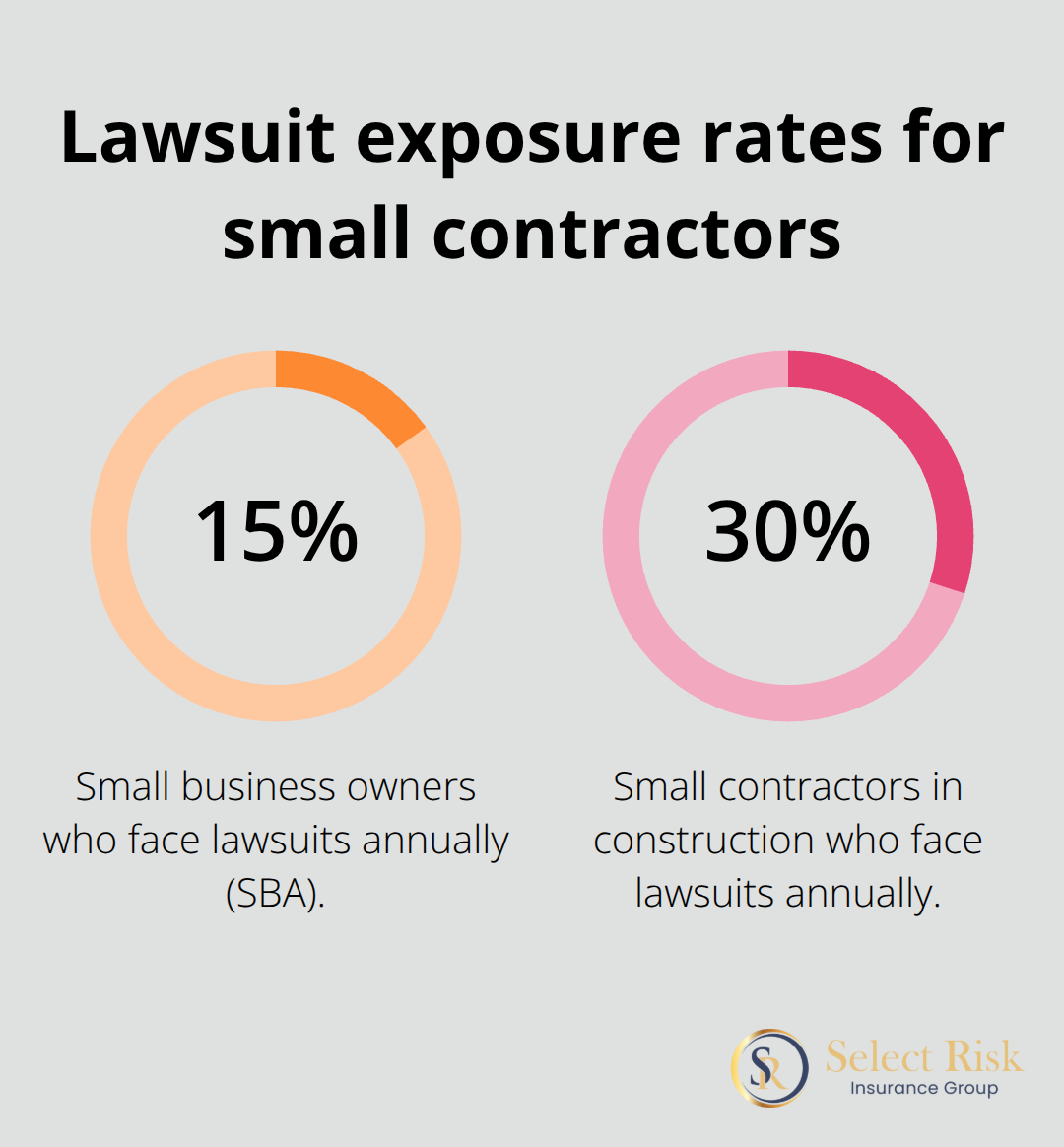

Operation without required coverage triggers severe financial consequences that compound quickly. The Louisiana Workforce Commission imposes fines that start at $1,000 for first-time workers’ compensation violations and escalate to $5,000 for repeat offenses. Parish violations carry additional penalties that range from $500 to $2,500 per incident. More damaging than fines, uninsured handymen face personal liability for all claims, with the average property damage lawsuit costing $15,000 to $50,000 in legal defense alone (according to industry reports). The Small Business Administration reports that 15% of small business owners face lawsuits annually, which makes compliance with insurance requirements a business survival issue rather than a regulatory checkbox.

These legal requirements represent just the foundation of protection that Louisiana handymen need. Beyond mandatory coverage, smart contractors invest in additional insurance types that shield them from the full spectrum of risks they face daily.

Which Insurance Policies Should Handymen Carry

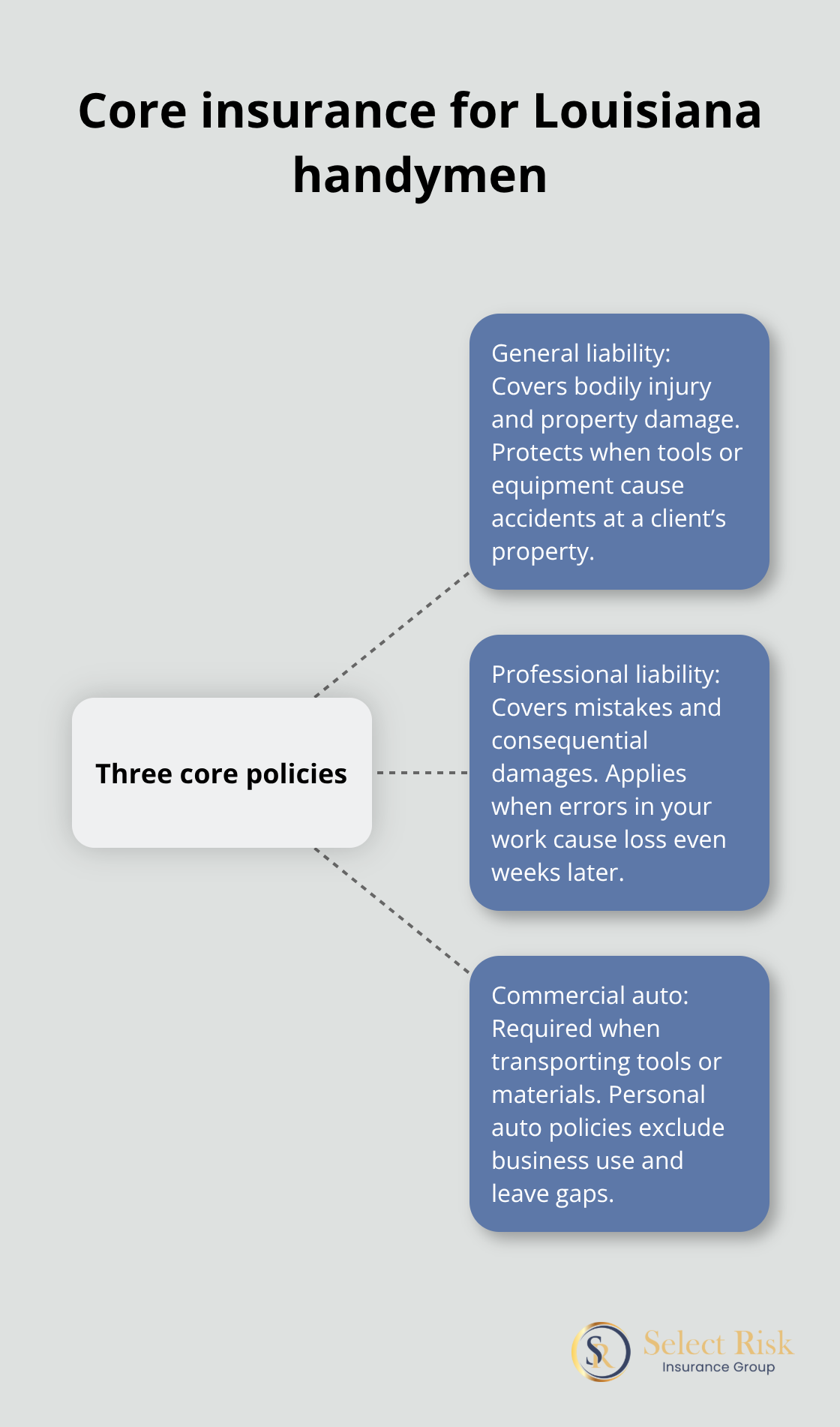

Louisiana handymen need three core insurance types that protect against the most common and expensive claims. General liability insurance stands as the foundation and covers bodily injury and property damage claims. This coverage protects when your ladder damages a client’s roof or when someone trips over your tools.

Professional liability insurance covers mistakes in your work, such as incorrect electrical installations that cause damage weeks later. Commercial auto insurance becomes mandatory when you transport tools and materials, as personal auto policies exclude business use and leave you exposed to significant liability gaps.

General Liability Coverage Forms Your Primary Defense

General liability insurance can cost as little as $19 per month for some businesses in Louisiana and covers the majority of handyman claims. This policy handles slip-and-fall accidents, property damage from your work, and advertising injury claims. The standard $1 million per occurrence limit satisfies most client requirements, though larger commercial projects may demand $2 million coverage. Products and completed operations coverage within your general liability policy protects against damage that appears after project completion, which represents a major risk for handymen. Without this coverage, a faulty repair that causes water damage months later could result in tens of thousands in personal liability.

Professional Liability Protects Against Work Errors

Professional liability insurance averages $61 monthly in Louisiana and covers errors in service delivery that general liability excludes. This coverage proves vital when clients claim your work failed to meet specifications or caused consequential damages. Mistakes happen even to experienced contractors, and this insurance shields you from claims that your workmanship caused financial losses. The coverage extends beyond simple accidents to include allegations of negligence or failure to complete work according to agreed standards.

Commercial Auto Insurance Completes Your Protection

Commercial auto insurance costs vary by vehicle type but typically runs $150 to $300 monthly for work trucks. This coverage protects against accidents while you drive to job sites and covers theft of tools stored in vehicles. Personal auto policies specifically exclude business use, which means that even a simple drive to a client’s home without commercial coverage voids your protection entirely. The financial consequences of this gap can devastate your business when accidents occur during work-related travel.

These three insurance types work together to create comprehensive protection, but the real financial impact becomes clear when you examine what happens to handymen who operate without adequate coverage.

What Financial Disasters Await Uninsured Handymen

Uninsured handymen face catastrophic financial exposure that destroys businesses and personal wealth within months of a single incident. Legal defense costs alone average $15,000 to $50,000 per lawsuit according to Small Business Administration data, and these expenses accumulate before any settlement or judgment. Property damage claims escalate quickly beyond most handymen’s financial capacity, with water damage from faulty repairs averaging $13,954 in payouts. The construction industry reports that 30% of small contractors face lawsuits annually, which makes exposure to these costs a statistical certainty rather than a remote possibility.

Legal Defense Expenses Drain Resources Immediately

Attorney fees consume business revenue from the moment a claim gets filed, regardless of fault or ultimate outcome. Louisiana attorneys charge $200 to $400 per hour for construction litigation, with simple cases that require 50 to 100 hours of legal work. Expert witness fees add another $5,000 to $15,000 per case, as technical testimony becomes necessary to defend handyman work quality. Court costs, depositions, and case preparation expenses compound these figures and create financial pressure that forces many uninsured contractors to settle valid defenses rather than fight through trial. The Insurance Information Institute reports that defense costs often exceed actual damage awards, which means uninsured handymen pay twice the amount that insured competitors would face.

Property Damage Claims Exceed Most Business Budgets

Water damage represents the most expensive risk that handymen face, with claims that routinely exceed $50,000 when pipes burst or roofs leak after repairs. Electrical mistakes trigger house fires that cost $100,000 to $300,000 in damages (according to National Fire Protection Association data). Structural damage from improper installations can reach $200,000 or more when foundations shift or walls collapse. These claims destroy personal assets when handymen lack adequate coverage, as courts hold business owners personally liable for damages their work causes.

Business Income Stops During Legal Battles

Lawsuits paralyze handyman operations as time shifts from revenue work to legal proceedings and stress management. Complex cases drag on for 18 to 36 months, during which handymen struggle to maintain client relationships while they manage legal obligations. Reputation damage from public legal proceedings reduces new client acquisition by 40% to 60% according to industry surveys and creates a downward spiral that outlasts the actual lawsuit resolution. Many handymen exhaust personal savings and business credit lines to maintain operations during litigation, which leaves them financially vulnerable even after favorable case outcomes.

Final Thoughts

Louisiana handymen face severe financial risks when they operate without proper insurance coverage. State regulations demand specific coverage types, and violations result in hefty penalties that can destroy businesses. Workers’ compensation becomes mandatory with your first employee, while general liability coverage of $1 million protects against the $15,000 to $50,000 legal defense costs that bankrupt uninsured contractors.

Smart contractors secure handyman insurance Louisiana coverage before they face claims or legal challenges. We at Select Risk Insurance Group help Louisiana handymen find comprehensive coverage that meets state requirements and client expectations. Our team works with multiple insurance carriers to provide competitive quotes for general liability and workers’ compensation policies.

The right insurance protects both your business operations and personal assets from catastrophic losses. Select Risk Insurance Group provides personalized insurance solutions that shield handymen from lawsuit costs and property damage claims. Monthly premium costs pale in comparison to the financial devastation that uninsured contractors face when accidents occur (or lawsuits arise from their work).