Independent Contractor Insurance in Louisiana Explained

Louisiana independent contractors face unique insurance challenges that can make or break their business success. The state’s specific regulations and industry requirements create a complex landscape that demands careful navigation.

We at Select Risk Insurance Group understand these local complexities. This guide breaks down the essential coverage types, state-specific requirements, and cost-saving strategies every Louisiana contractor needs to know.

What Insurance Coverage Do Louisiana Independent Contractors Actually Need?

General Liability Insurance Forms Your Foundation

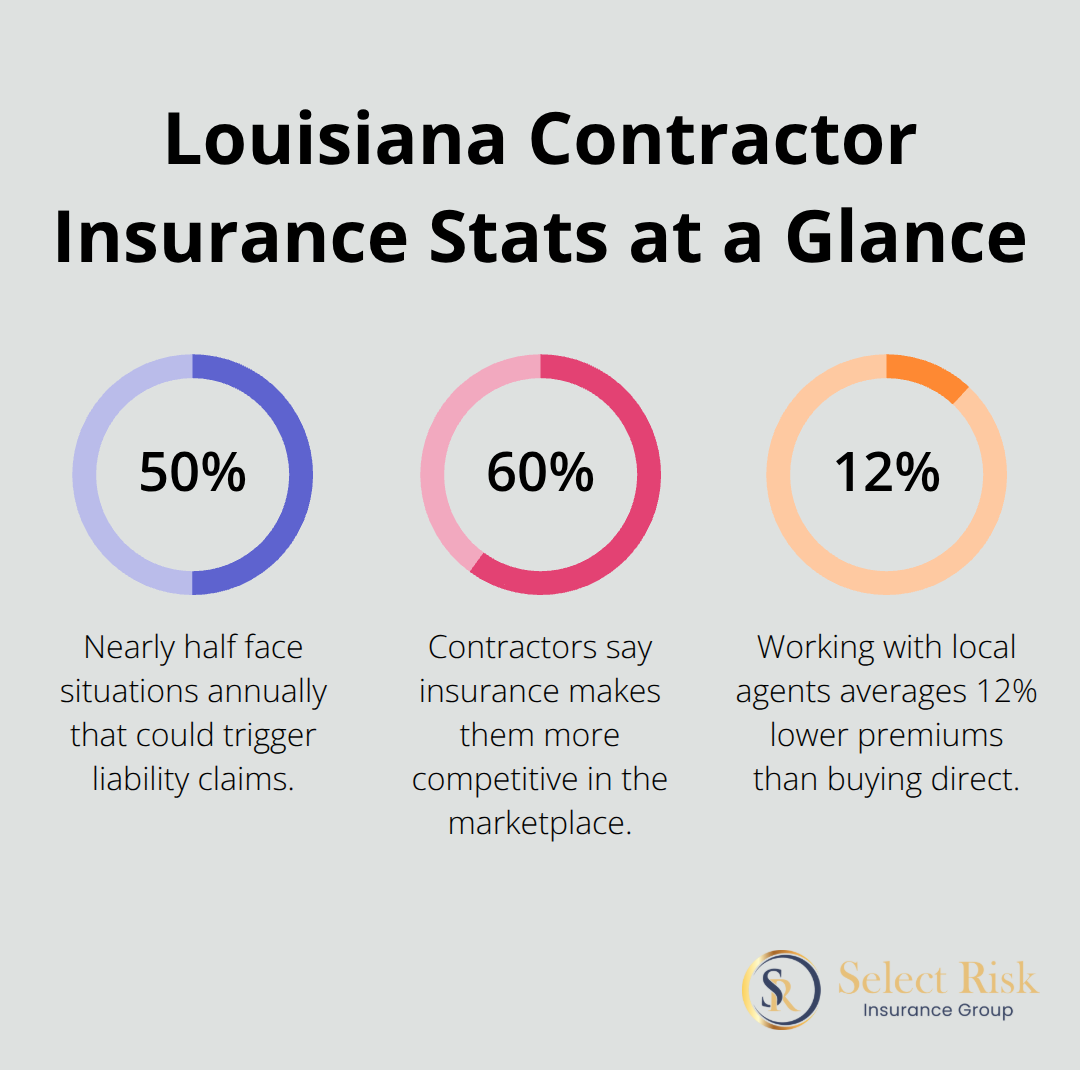

General liability insurance stands as your first line of defense against costly lawsuits. Louisiana contractors face average monthly premiums of $47 for this coverage, but the protection extends far beyond the cost. This insurance covers bodily injury claims when someone gets hurt at your worksite, property damage from your operations, and personal injury lawsuits (including defamation claims). The National Association of Insurance Commissioners reports that nearly 50% of independent contractors experience situations annually that could trigger liability claims. Louisiana requires minimum coverage of $500,000 per occurrence and $1,000,000 aggregate for most contractor work.

We recommend higher limits because construction accidents often exceed these minimums, and legal defense costs alone can drain your business finances.

Professional Liability Protects Against Service Failures

Professional liability insurance, also called errors and omissions coverage, protects when your work fails to meet client expectations. Louisiana contractors pay an average of $70 monthly for this protection, which covers negligence claims, missed deadlines, and design errors. The coverage becomes mandatory for licensed professionals like architects and engineers, but smart contractors in all trades secure this protection. A 2023 survey found that 60% of independent contractors believe insurance makes them more competitive in the marketplace. Professional liability insurance demonstrates your commitment to quality work and gives clients confidence when they hire you. This coverage handles legal costs and damages when clients claim your services caused financial losses, even if you followed industry standards perfectly.

Workers Compensation Requirements Apply Selectively

Louisiana law mandates workers compensation insurance for independent contractors who hire employees, but exempts true independent contractors who work alone. Monthly costs average $59 in Louisiana, covering medical treatment and lost wages for work-related injuries. The Louisiana Workforce Commission requires injury reports within 24 hours (making proper coverage essential for compliance). Independent contractors who use subcontractors must verify their workers compensation status or risk liability exposure. Many contractors mistakenly assume they need this coverage when they work solo, but Louisiana’s House Bill 705 clarifies that true independent contractors who operate alone remain exempt. However, the moment you hire help, even temporarily, this protection becomes legally required and financially necessary.

Understanding these basic coverage types sets the stage for navigating Louisiana’s specific insurance requirements, which vary significantly based on your industry and the type of work you perform.

What Insurance Requirements Must Louisiana Contractors Meet?

Louisiana contractors must navigate state-specific insurance mandates that extend beyond basic coverage recommendations. The Louisiana State Licensing Board for Contractors requires general liability insurance with minimum limits that vary by project type and contractor classification. Commercial auto insurance becomes mandatory when you use vehicles for business purposes, with minimum liability coverage of $1,000,000 per occurrence for automobile liability insurance. These state minimums fall dangerously short of real-world claim costs, which average $43,000 for bodily injury claims according to the Insurance Information Institute.

Industry-Specific Mandates Create Additional Requirements

Different construction trades face distinct insurance requirements based on risk exposure and state regulations. Electrical contractors must carry professional liability insurance to maintain their licenses, while plumbers need inland marine coverage for expensive equipment. HVAC contractors who work on commercial projects often face contractual requirements for commercial umbrella insurance with $2,000,000 limits. The Louisiana Department of Transportation and Development mandates specific bonds and insurance requirements for highway contractors, which include builders risk insurance for projects that exceed $50,000. Roofing contractors face the highest insurance costs, with premiums that reach 40% above standard rates due to weather-related claims exposure.

Compliance Failures Trigger Severe Financial Penalties

Louisiana imposes harsh penalties for insurance compliance failures that can destroy contractor businesses overnight. Operations without required coverage result in immediate license suspension and fines that start at $500 for first offenses, then escalate to $2,500 for repeat violations. The Louisiana Workforce Commission conducts regular audits of contractor insurance status, and misclassification penalties compound quickly when workers compensation coverage lapses. ACORD certificates must remain current and accurately reflect coverage limits (as outdated certificates void contract protections and expose contractors to personal liability). Smart contractors maintain insurance documentation with their state authority and update coverage before renewals to prevent gaps that trigger automatic penalties.

These state requirements represent just the foundation of your insurance obligations. The actual costs of comprehensive coverage depend on multiple factors that can dramatically impact your premium calculations and overall insurance investment.

How Much Will Your Contractor Insurance Actually Cost?

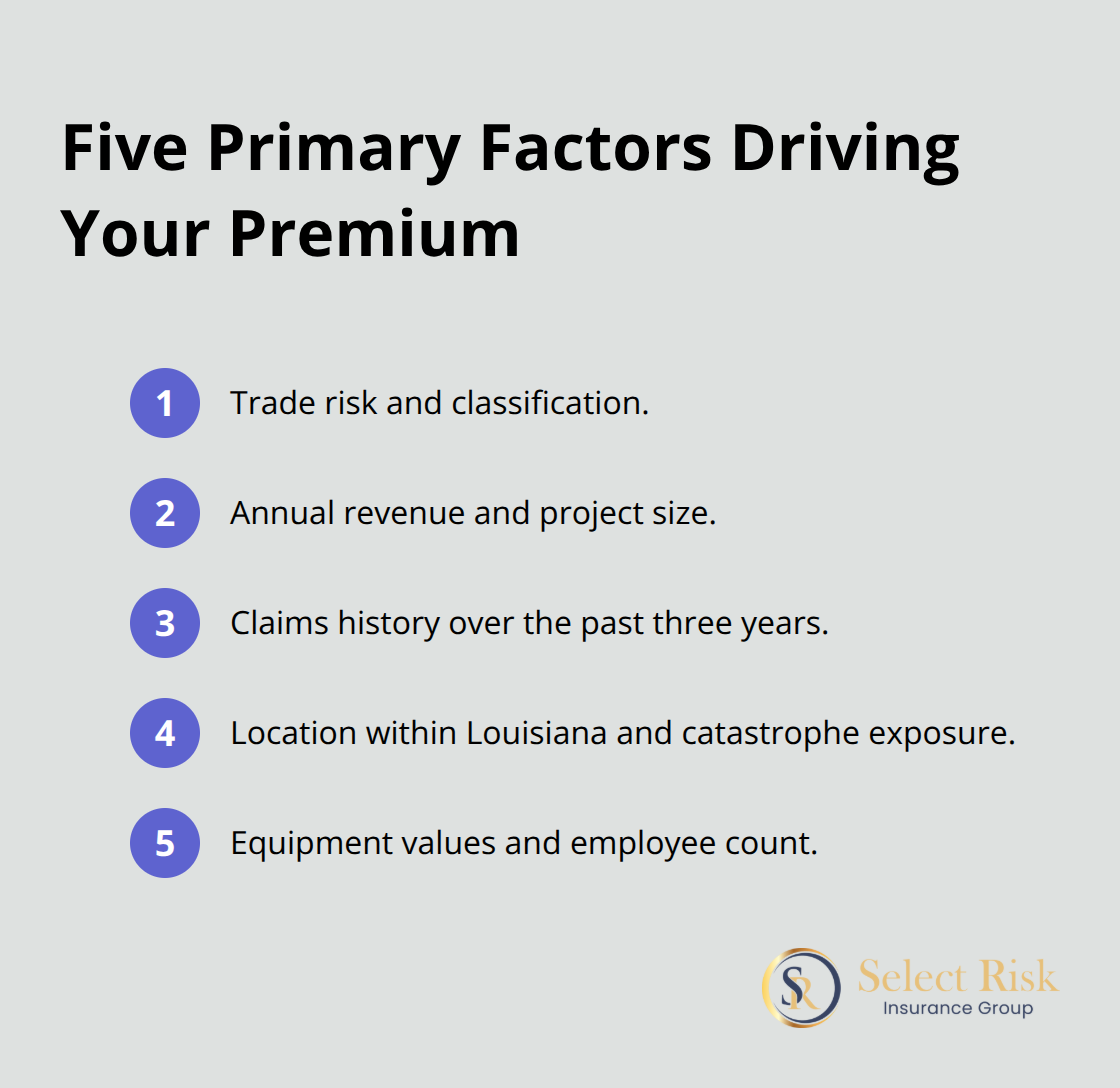

Insurance premiums for Louisiana contractors depend on five primary factors that insurers evaluate ruthlessly. Your industry classification drives the biggest cost variations, with roofing contractors who pay 40% more than general contractors due to weather exposure and claim frequency. Annual revenue directly impacts premiums because higher revenue suggests larger projects and greater liability exposure.

Claims history creates the most dramatic premium swings, with contractors who filed claims in the past three years who face increases of 25-50% compared to clean records. Geographic location within Louisiana matters significantly, as contractors in hurricane-prone coastal parishes pay substantially more than those in northern parishes. Equipment values and employee counts round out the calculation, with each additional worker who typically adds $400-600 annually to workers compensation costs.

Multi-Policy Packages Cut Costs by 15-25%

Multiple insurance policies with one carrier generate automatic discounts that Louisiana contractors routinely overlook. Business Owner’s Policies combine general liability and commercial property insurance at costs 20% below separate policies, while commercial auto insurance added to current coverage typically saves another 10-15%. Recommended contractor bundles cost approximately $607 per month or $7,280 yearly for combined BOP, workers’ comp and professional liability coverage. We recommend contractors secure quotes for comprehensive packages rather than shop individual policies separately. Payment methods also impact total costs, with annual payments that reduce premiums by 5-8% compared to monthly installments that include processing fees. Contractors who maintain continuous coverage without lapses qualify for loyalty discounts that increase over time and reach 10% after three claim-free years. The Louisiana Independent Insurance Agents Association reports that contractors who work with local agents average 12% lower premiums than those who buy direct from national carriers, primarily because local agents understand state-specific requirements and can match contractors with carriers that specialize in Louisiana risks.

Smart Shopping Strategies Maximize Value

Request quotes from at least four different carriers because premium variations exceed 30% for identical coverage among competitors. Focus on coverage limits and deductibles rather than just premium costs, as inadequate limits create false savings that disappear when claims occur. Schedule annual policy reviews six weeks before renewal dates to allow sufficient time for carrier comparison and coverage adjustments.

Maintain detailed records of safety training, equipment maintenance, and project specifications because insurers reward contractors who demonstrate proactive risk management with preferred rates which can reduce premiums by up to 15%. Professional contractors should also consider specialized coverage options that address their specific trade requirements and risk exposures.

Final Thoughts

Louisiana independent contractors face insurance requirements that demand immediate attention and professional guidance. General liability insurance with $500,000 minimum coverage, professional liability protection, and workers compensation compliance form the foundation of your risk management strategy. These requirements become more complex when you factor in industry-specific mandates and state penalties that start at $500 for first violations.

Local insurance experts who understand Louisiana’s regulatory landscape provide significant advantages over national carriers. We at Select Risk Insurance Group represent multiple financially sound insurance companies, which allows us to offer comprehensive coverage at competitive prices throughout Louisiana. Our Lafayette-based team understands the specific challenges that face independent contractors in our state and can navigate the complex requirements that vary by parish and industry.

Your next step involves securing proper independent contractor insurance Louisiana coverage before you face a claim or compliance audit. Schedule consultations with qualified agents, gather quotes from multiple carriers, and prioritize adequate coverage limits over low premiums. The cost of comprehensive protection remains minimal compared to the financial devastation that follows inadequate coverage (making proper coverage a smart business investment). Contact Select Risk Insurance Group today to review your current coverage and identify gaps that could threaten your business operations.

![General Contractor Insurance in Louisiana [2025 Guide]](https://selectriskgroup.com/wp-content/uploads/emplibot/General-Contractor-Insurance-in-Louisiana-_2025-Guide__1764976093-80x80.jpeg)