Understanding Commercial Auto Liability Insurance

Commercial auto liability insurance protects businesses from financial losses when company vehicles cause accidents. This coverage handles medical bills, property damage, and legal costs that result from at-fault incidents.

We at Select Risk Insurance Group see many business owners confused about what commercial auto insurance covers. The right policy protects your company’s assets and keeps operations running smoothly after vehicle-related accidents.

What Commercial Auto Liability Insurance Covers

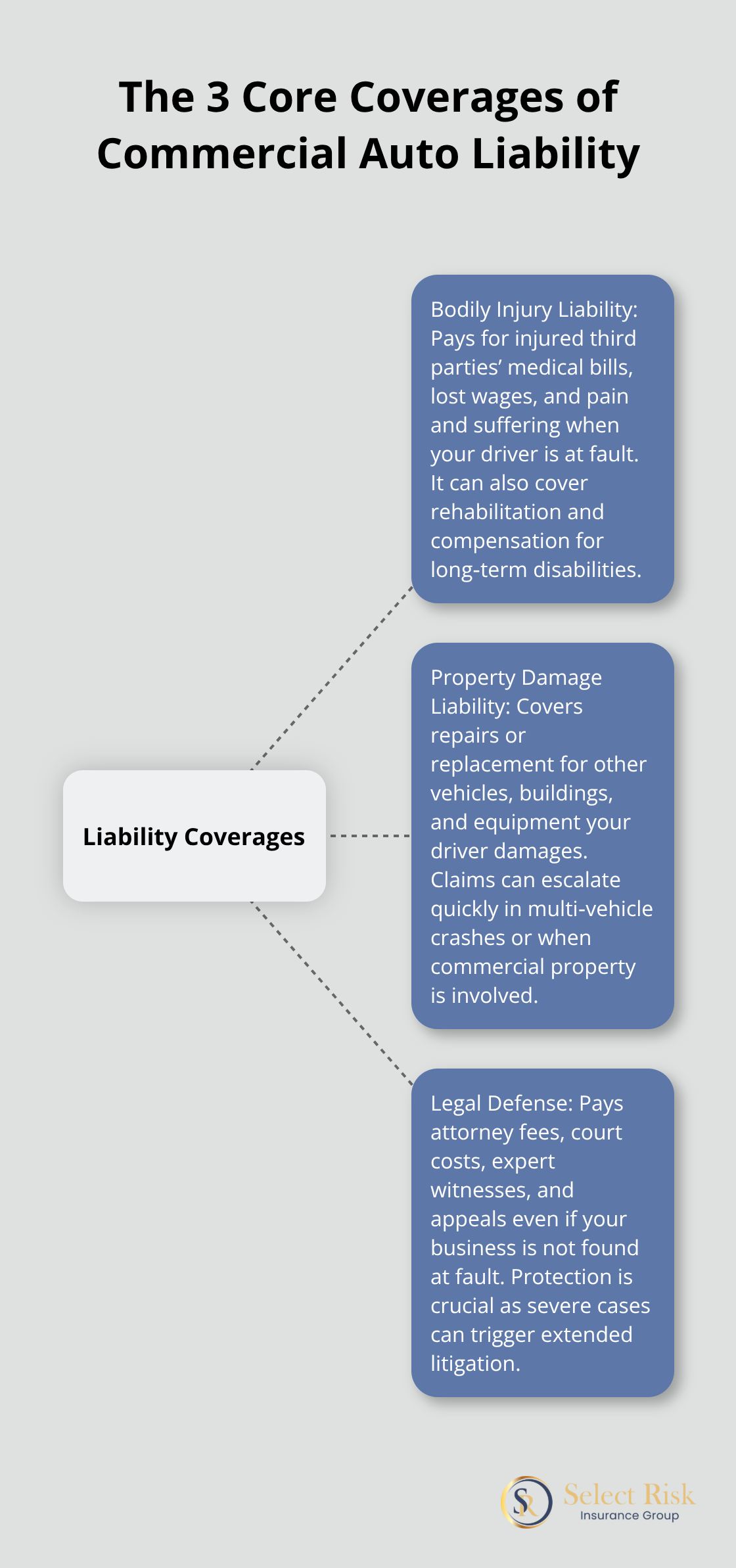

Commercial auto liability insurance provides three distinct types of protection that work together to shield your business from financial disaster. When your company vehicle causes an accident, this coverage steps in to handle the aftermath.

Bodily Injury Protection for Third Parties

Bodily injury liability covers medical expenses, lost wages, and pain and suffering for injured third parties when your driver causes an accident. Non-fatal injuries with days away from work average $27,033 per incident, while fatalities cost an average of $2.8 million. However, serious injuries push costs much higher. A single traumatic brain injury can generate medical bills exceeding $500,000, while spinal cord injuries often cost over $1 million in lifetime care.

This protection extends beyond immediate medical costs. It covers rehabilitation expenses, lost income for accident victims, and compensation for permanent disabilities. The coverage also handles pain and suffering awards, which courts frequently set at two to three times the medical expenses in severe injury cases.

Property Damage Coverage for Other Vehicles and Structures

Property damage liability handles repairs or replacement costs when your driver damages other vehicles, buildings, fences, or equipment. These claims average $5,700 per incident according to Insurance Information Institute data, but costs escalate quickly in multi-vehicle accidents. Commercial trucks that strike multiple cars can generate property damage claims exceeding $100,000 in a single incident.

The coverage extends beyond vehicle repairs to include damaged infrastructure, commercial buildings, and specialized equipment. A delivery truck that crashes into a restaurant’s storefront faces property damage claims that include building repairs, lost inventory, and business interruption costs (often reaching $200,000 or more).

Legal Defense Costs and Court Expenses

Legal defense coverage pays attorney fees, court costs, and settlement negotiations even when your business bears no fault. Defense costs alone reach $100,000 to $300,000 in serious accident cases before any settlement or judgment. This coverage activates immediately when someone files a lawsuit against your company, regardless of liability determination.

Nuclear verdicts against commercial defendants have increased 300% since 2010, making legal protection more valuable than ever. The coverage handles expert witness fees, accident reconstruction costs, and appeals processes that can extend litigation for years.

These three coverage types work together, but their effectiveness depends entirely on the limits you select and how well they match the actual risks your business faces on the road.

When Your Business Needs Commercial Auto Liability Insurance

Your business needs commercial auto liability insurance the moment you own, lease, or regularly use vehicles for business operations. Every state mandates minimum liability coverage for commercial vehicles, with requirements that range from Alabama’s $25,000 per person limit to California’s $750,000 requirement for interstate carriers. These minimums rarely provide adequate protection for modern businesses that face large verdicts with a nearly 1,000% increase in truck crash cases.

Company-Owned Vehicle Requirements

States classify any vehicle used primarily for business as commercial, which triggers higher insurance requirements than personal auto policies. Texas requires $30,000 per person and $60,000 per accident for commercial vehicles, while passenger transport companies need $1.5 million in coverage. Vehicle weight also matters – Indiana mandates $1 million coverage for commercial vehicles over 10,000 pounds and $5 million for hazardous materials transport. We recommend coverage limits of at least $1 million per occurrence regardless of state minimums, as the average commercial auto claim now exceeds $180,000.

Employee Vehicle Use Creates Hidden Liability

Your business faces liability when employees drive personal vehicles for work tasks, even if you don’t own the vehicle. This exposure requires hired and non-owned auto coverage, which costs roughly 10% of your owned auto premium but protects against million-dollar lawsuits. Employees who make deliveries, attend client meetings, or run business errands create vicarious liability that standard personal auto policies won’t cover. Companies that use independent contractors or subcontractors need contingent auto liability coverage, as contractor insurance gaps can leave your business exposed to third-party claims.

Fleet Operations Demand Comprehensive Protection

Businesses that operate multiple vehicles face exponentially higher risks and stricter state oversight. Commercial fleets with USDOT numbers require minimum $750,000 coverage in most states, with some jurisdictions that demand $5 million for specific cargo types. Fleet operators also need physical damage coverage for collision and comprehensive protection, as replacement of a single commercial vehicle costs $40,000 to $80,000 on average. Smart fleet managers use telematics systems to monitor driver behavior, which can reduce premiums by 15% to 25% while they improve safety records.

The coverage requirements and liability exposures your business faces directly impact what you’ll pay for commercial auto insurance premiums.

Factors That Affect Commercial Auto Liability Insurance Costs

Commercial auto insurance premiums depend on three primary factors that insurers evaluate to determine your business risk profile. Understanding these cost drivers helps you make informed decisions about coverage and budget planning.

Driver Records and Experience Levels

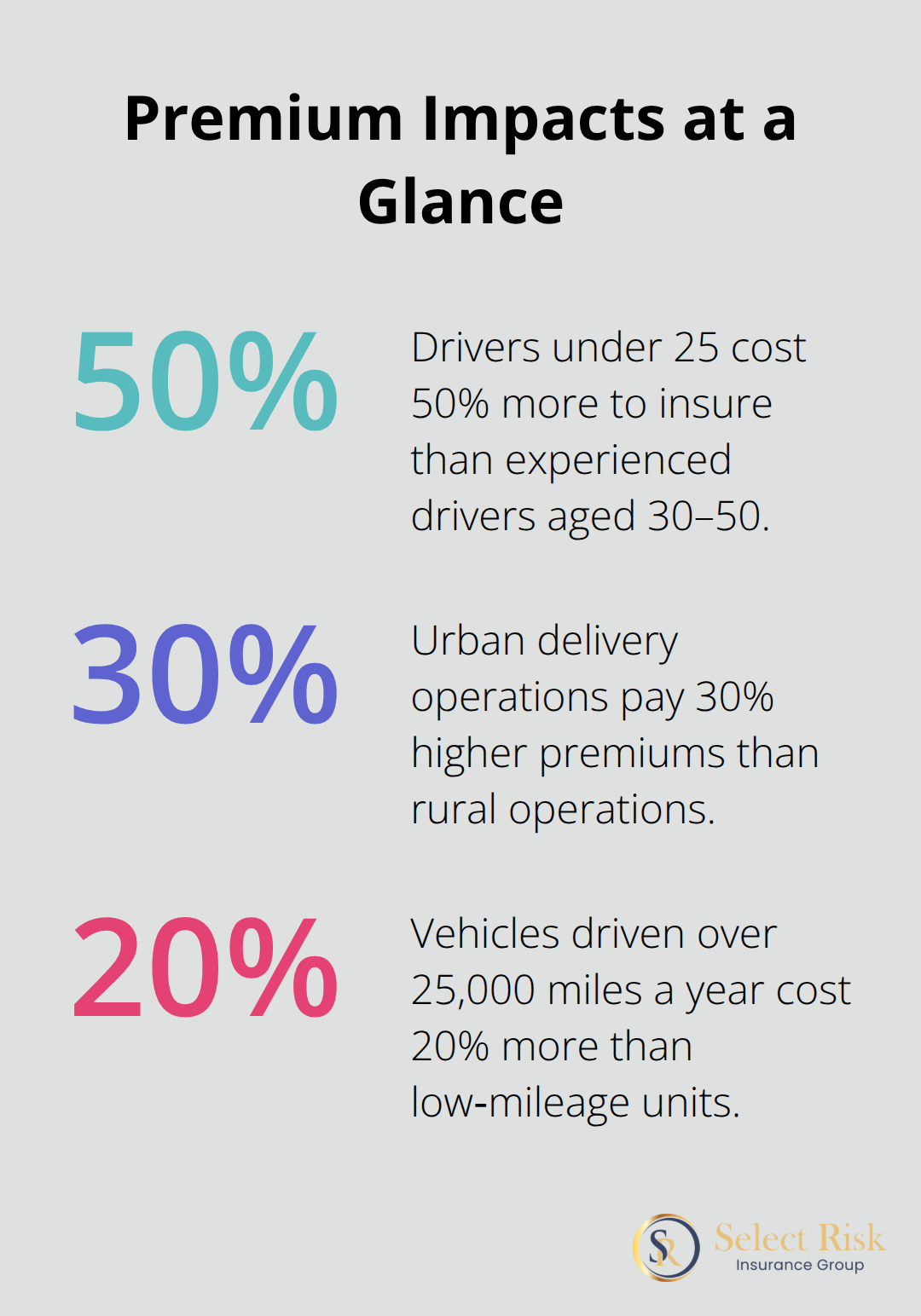

Driver records carry the most weight in pricing decisions. Insurers analyze the past three to five years of driving history for every employee who operates company vehicles. A single DUI conviction increases premiums by 40% to 60%, while multiple moving violations can double your rates.

Clean driving records with zero claims over three years qualify for preferred pricing that saves 15% to 25% annually. Age matters significantly too – drivers under 25 cost 50% more to insure than experienced drivers between 30 and 50 years old (according to Insurance Information Institute data).

Companies can reduce costs by implementing driver training programs and regular motor vehicle record checks. Some insurers offer additional discounts for businesses that maintain driver safety programs or use telematics to monitor driver behavior.

Vehicle Types and Usage Patterns

Heavy-duty trucks cost three times more to insure than standard pickup trucks due to their damage potential and higher claim severity. Delivery vehicles that operate in dense urban areas face premiums 30% higher than rural operations because of increased accident frequency.

Mileage directly impacts rates – vehicles driven over 25,000 miles annually cost 20% more than low-mileage fleet units. The type of cargo you transport also affects pricing, with hazardous materials requiring specialized coverage and minimum financial responsibility requirements established in the 1980s.

Vehicle age and safety features influence premiums as well. Newer vehicles with advanced safety systems often qualify for discounts, while older commercial vehicles without modern safety equipment face higher rates.

Coverage Limits and Deductible Amounts

Your coverage limits and deductible selections control the final pricing element. Minimum state limits might save money upfront but expose your business to catastrophic losses. $1 million combined single limit policies cost only 15% more than basic coverage but provide substantially better protection.

Raising physical damage deductibles from $500 to $2,500 reduces premiums by 25% to 35%. This strategy requires adequate cash reserves for self-insurance of smaller claims but can generate significant annual savings for businesses with good safety records.

Split limit policies (such as $100,000/$300,000/$100,000) typically cost less than combined single limit policies but may leave gaps in coverage during severe accidents involving multiple victims.

Final Thoughts

Adequate commercial auto liability coverage protects your business from financial ruin when accidents occur. The right policy handles medical bills that average $27,033 for non-fatal injuries, property damage claims that average $5,700, and legal defense costs that reach $300,000 in serious cases. Understanding what does commercial auto insurance cover helps you select appropriate limits that match your actual risk exposure.

Start with minimum $1 million combined single limits regardless of state mandates, as nuclear verdicts have increased 300% since 2010. Consider your industry risk profile, vehicle types, and employee records when you select coverage options. Regular policy reviews protect against coverage gaps as your business evolves (annual assessments help identify new exposures from fleet expansion, route changes, or employee additions).

We at Select Risk Insurance Group work with multiple carriers to find competitive rates that match your specific business requirements. Our independent agency approach means we can compare options across different insurers to secure comprehensive protection at the best available prices. Contact our team to review your current coverage and identify potential improvements that protect your business assets while managing insurance costs effectively.