Owner-Operator Insurance Essentials Every Trucker Should Know

Starting your own trucking business means navigating complex insurance requirements that can make or break your operation. Owner-operator insurance isn’t just about meeting legal minimums-it’s about protecting your livelihood and investment.

At Select Risk Insurance Group, we see too many independent truckers struggle with coverage gaps that cost them thousands. The right insurance strategy separates successful owner-operators from those who fail within their first year.

What Insurance Requirements Must Owner-Operators Meet?

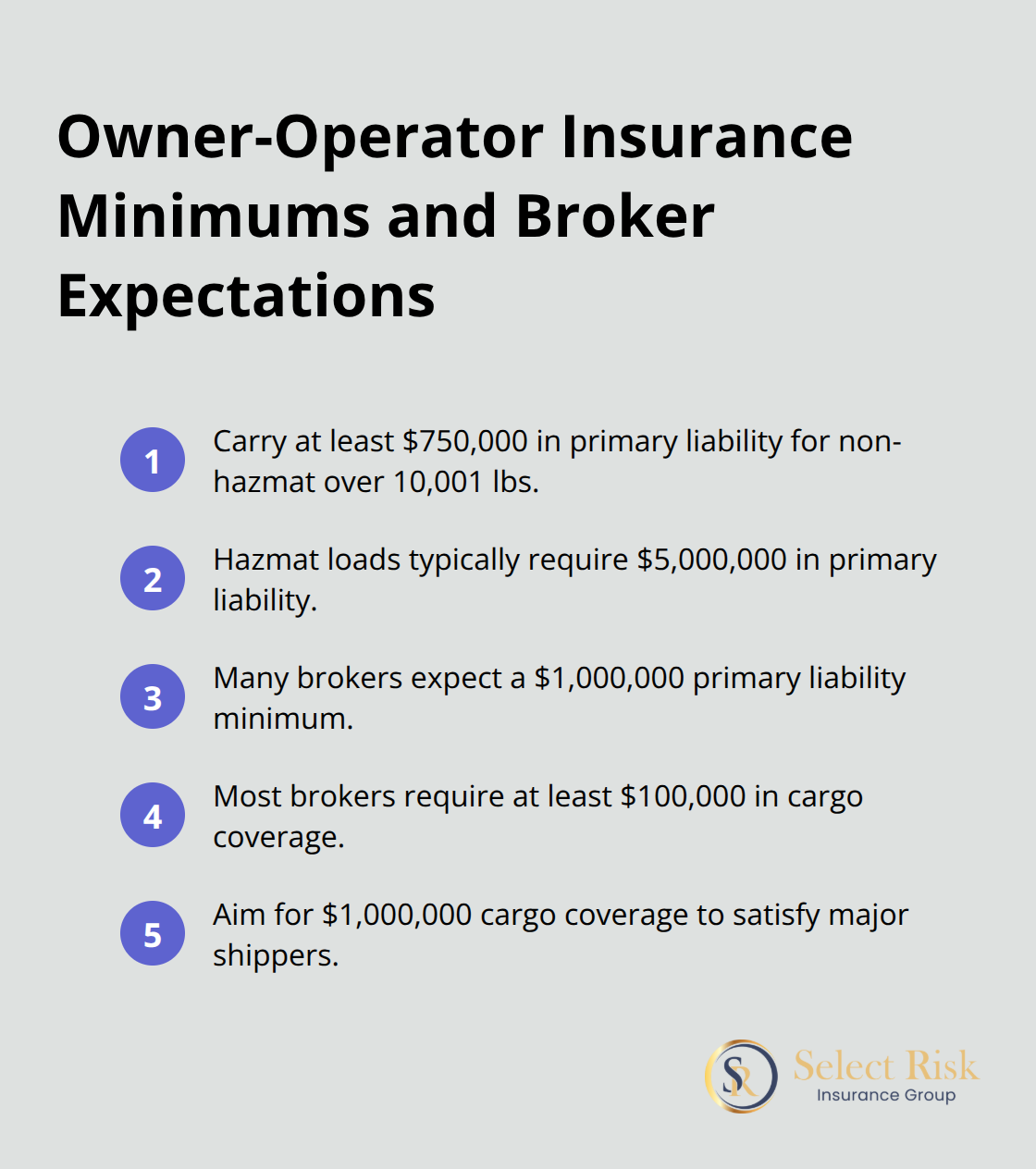

The FMCSA mandates that owner-operators carry a minimum of $750,000 in primary liability coverage for non-hazmat freight over 10,001 pounds. This amount jumps to $5 million for hazmat loads, and most brokers refuse to work with operators who carry less than $1 million minimum. These represent legal requirements that determine your ability to operate legally, not mere suggestions.

The Federal Motor Carrier Safety Administration will not issue your MC number without proof of adequate liability and cargo insurance. Most freight brokers require at least $100,000 in cargo coverage, though we recommend $1 million to match what major shippers demand.

Federal Insurance Certificate Process

Your insurance provider must file Form MCS-90 with the FMCSA, which serves as your financial responsibility endorsement. This document proves you meet federal insurance requirements and remains active as long as you maintain coverage. The certificate process typically takes 3-5 business days to complete once your policy activates.

You must maintain continuous coverage and file updated certificates within 30 days of any policy changes. Interstate carriers face stricter requirements than intrastate operators, with some states mandating additional coverage types like uninsured motorist protection.

State-Specific Coverage Variations

State requirements vary significantly across the country. California demands higher minimums than federal standards (often requiring $1 million baseline coverage), while Texas follows federal minimums exactly. Florida requires additional personal injury protection, and New York mandates higher cargo coverage limits for certain freight types.

These variations create compliance challenges for owner-operators who cross state lines regularly. You must meet the highest requirement of any state where you operate, making federal minimums insufficient for most interstate operations.

Strategic Coverage Beyond Legal Minimums

Minimum coverage represents financial suicide in today’s litigation environment. A single accident can easily exceed $750,000, which leaves you personally liable for the difference. Successful owner-operators carry $1 million in primary liability as their baseline, with many choosing $2 million when they haul high-value freight.

Commercial general liability should complement your primary coverage. This protection typically costs $500-800 annually but shields you against premises liability and cargo handling claims. In 2023, 5375 large trucks were involved in fatal crashes, which makes adequate coverage a business necessity rather than an option.

These foundational requirements set the stage for understanding the specific types of coverage that protect your operation most effectively.

What Coverage Types Protect Your Business Best?

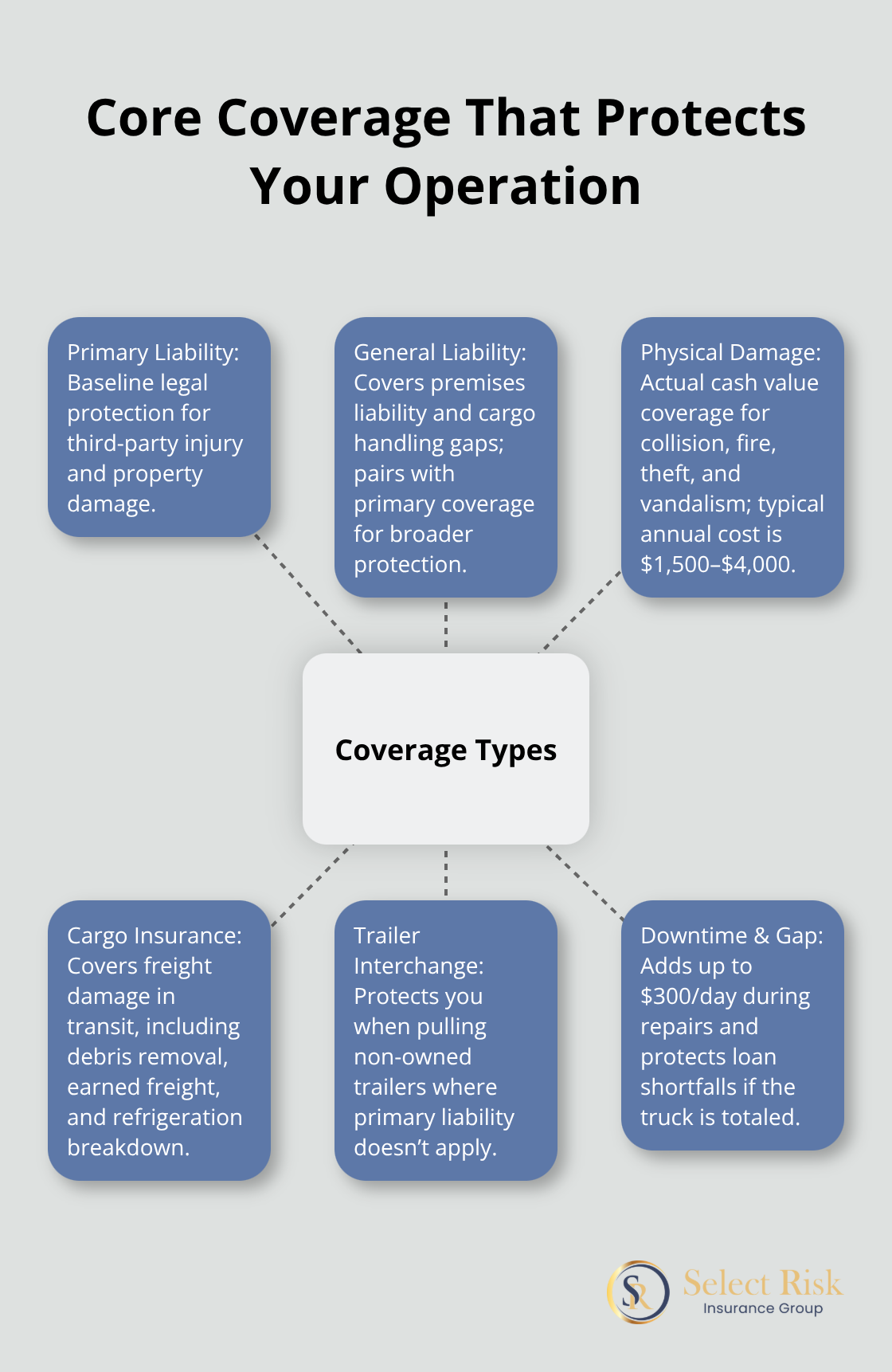

Primary liability insurance forms the foundation of your protection, but general liability insurance complements it by covering premises liability and cargo handling incidents that primary coverage excludes. Carriers offer premium savings of 10-15% when you combine both coverages with the same provider compared to separate policies. Physical damage coverage protects your truck and trailer against collision, fire, theft, and vandalism on an actual cash value basis, with annual costs that typically range from $1,500-4,000 based on your equipment value and deductible choice.

Physical Damage Coverage Decisions That Matter

Physical damage insurance becomes mandatory if you finance your truck, but your deductible choice affects your premium significantly. A $2,500 deductible versus $1,000 can reduce your annual premium by $800-1,200, though you accept higher out-of-pocket costs per claim. Combined deductibles apply when both tractor and trailer suffer damage in the same incident (you pay only the highest deductible rather than separate amounts). Additional downtime coverage provides up to $300 daily for repair delays, while gap coverage protects against loan balance shortfalls if your truck gets totaled.

Cargo Insurance Requirements You Cannot Ignore

Motor truck cargo insurance covers your liability for freight damage during transit, with most brokers that demand $100,000 minimum coverage though $1 million provides better protection. This coverage includes debris removal costs, earned freight protection, and refrigeration breakdown coverage for temperature-sensitive loads. Cargo claims present significant financial risks due to increasing operational costs and growing liability concerns in the trucking industry. Trailer interchange coverage becomes necessary if you pull non-owned trailers (it protects against damage liability that your primary coverage excludes).

Additional Protection Options Worth Consideration

Breakdown coverage handles towing and labor costs during unexpected mechanical failures, which provides peace of mind for long-haul operations. Personal property insurance protects items in your truck that other policies exclude, with coverage limits from $2,000 to $5,000 available. Rental reimbursement coverage offers up to $300 per day for replacement vehicles while your truck undergoes repairs, with total limits of $9,000 per policy period.

These coverage decisions directly impact your monthly expenses, which makes understanding cost factors and money-saving strategies your next priority.

How Much Can You Save on Premiums

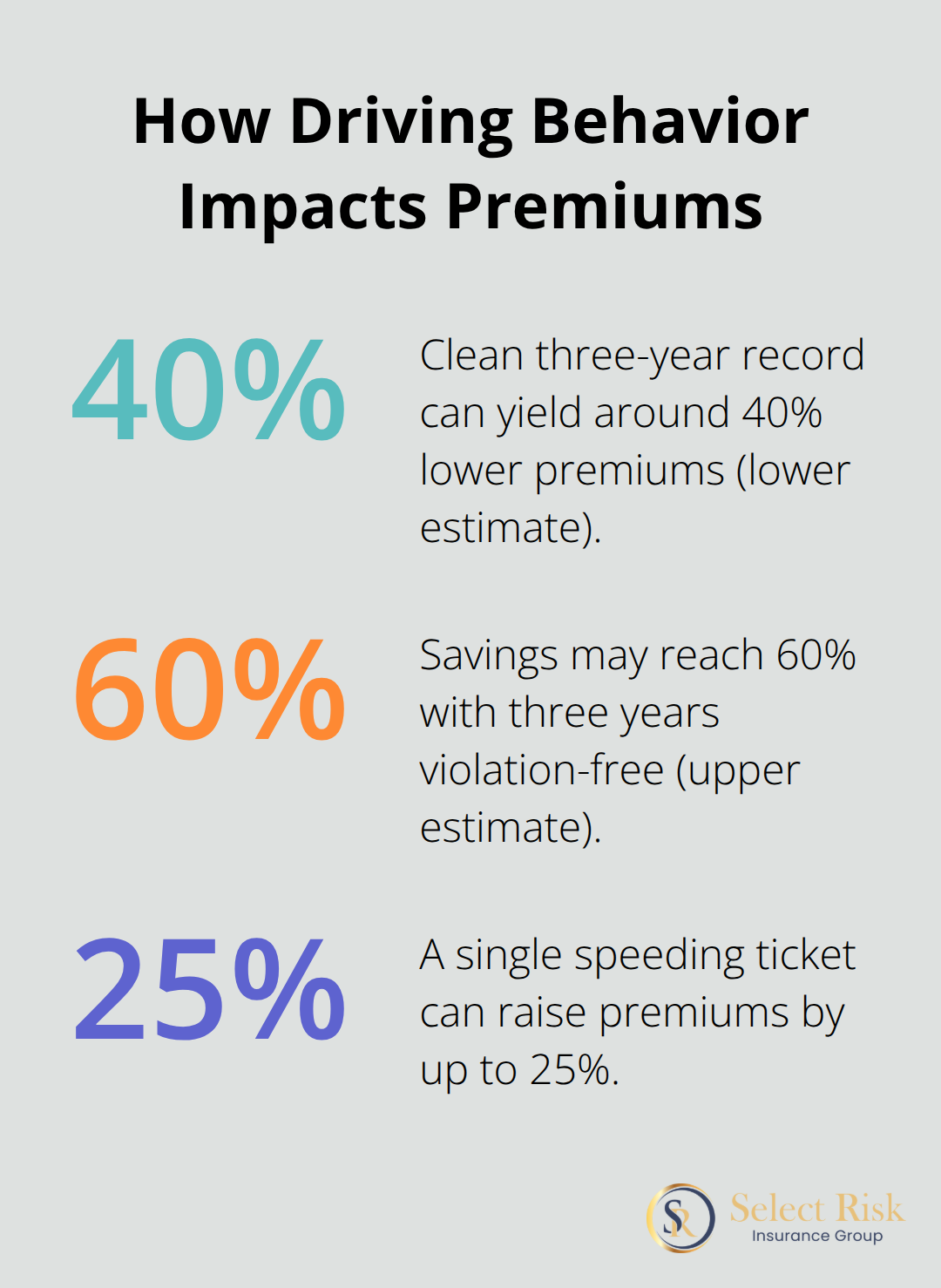

Your driving record carries more weight than any other factor in determining insurance costs. Owner-operators with clean records for three years pay 40-60% less than those with recent violations or accidents. A single speeding ticket increases premiums by 15-25%, while a preventable accident can double your rates for up to five years. New operators without commercial driving history face the highest rates, often paying $2,000-3,000 monthly until they establish a clean track record.

Experience Levels That Insurance Companies Reward

Insurance companies categorize drivers into risk tiers based on commercial driving experience. Operators with less than two years of experience pay premium rates that can exceed $1,800 monthly, while those with 5+ years of clean commercial driving history often secure rates below $1,200 monthly. The transition from high-risk to standard rates typically occurs at the three-year mark (assuming no claims or violations). Companies like Progressive and Nationwide offer new operator programs that reduce rates by 20-30% after drivers complete safety training, though these discounts require violation-free records.

Deductible Strategies That Impact Your Bottom Line

Physical damage deductible increases from $1,000 to $5,000 can reduce annual premiums by $1,500-2,500, but this strategy only works if you maintain adequate cash reserves for potential claims. Most successful owner-operators choose $2,500 deductibles as the sweet spot between premium savings and manageable out-of-pocket costs. Avoid deductibles higher than your available cash reserves, as accident repair financing creates additional financial strain.

Payment Methods That Reduce Total Costs

Independent agents often recommend annual premium payments over monthly installments, which eliminates service fees and can save 8-12% on total costs. Monthly payment plans typically include processing fees of $5-15 per transaction (adding $60-180 annually to your insurance expenses). Automatic bank draft payments sometimes qualify for additional 2-3% discounts with certain carriers, though you must maintain sufficient account balances to avoid overdraft penalties.

Shopping Strategies That Maximize Savings

Compare quotes from at least five different carriers, as rates can vary by 30-50% for identical coverage. Independent agents represent multiple companies and can streamline this comparison process while identifying discounts you might miss when shopping directly. Fleet discounts apply when you insure multiple trucks with the same carrier, often reducing premiums by 10-15% per additional vehicle.

Final Thoughts

New owner-operators must secure primary liability coverage at $1 million minimum, physical damage protection for financed equipment, and adequate cargo insurance that meets broker requirements. These three coverage types form your financial foundation and determine your ability to secure profitable loads. Owner-operator insurance decisions you make today will impact your business profitability for years.

Strong relationships with experienced insurance partners pay dividends over time. We at Select Risk Insurance Group help owner-operators navigate coverage decisions while identifying cost-saving opportunities. Independent agents understand the trucking industry’s unique risks and can adjust your coverage as your business grows.

Start your insurance search 30-45 days before you need coverage. Gather your records, business plan details, and equipment information before you request quotes (compare at least five different carriers). Focus on comprehensive protection rather than lowest premiums, as the cheapest policy often creates expensive coverage gaps that threaten your business survival.