Why For-Hire Truck Insurance is Essential for Your Business

For-hire trucking operations face significant financial and legal risks that can destroy businesses overnight. Without proper insurance coverage, a single accident or cargo loss can result in bankruptcy.

We at Select Risk Insurance Group see trucking companies struggle with complex insurance requirements daily. The right coverage protects your business from devastating liability claims and keeps you compliant with federal regulations.

What Insurance Coverage Does Federal Law Require for For-Hire Truckers?

FMCSA Minimum Coverage Standards

The Federal Motor Carrier Safety Administration establishes strict insurance requirements that for-hire truckers must follow. Property carriers who operate vehicles with a Gross Vehicle Weight Rating under 10,001 pounds must maintain minimum liability insurance. Companies that transport hazardous materials face a $1,000,000 minimum requirement, while those who haul explosives or radioactive materials need $5,000,000 in coverage.

Household goods carriers require $750,000 in liability plus $5,000 in cargo insurance. These federal mandates determine whether you can legally operate your business. The FMCSA does not treat these as optional guidelines – they represent absolute requirements for market entry.

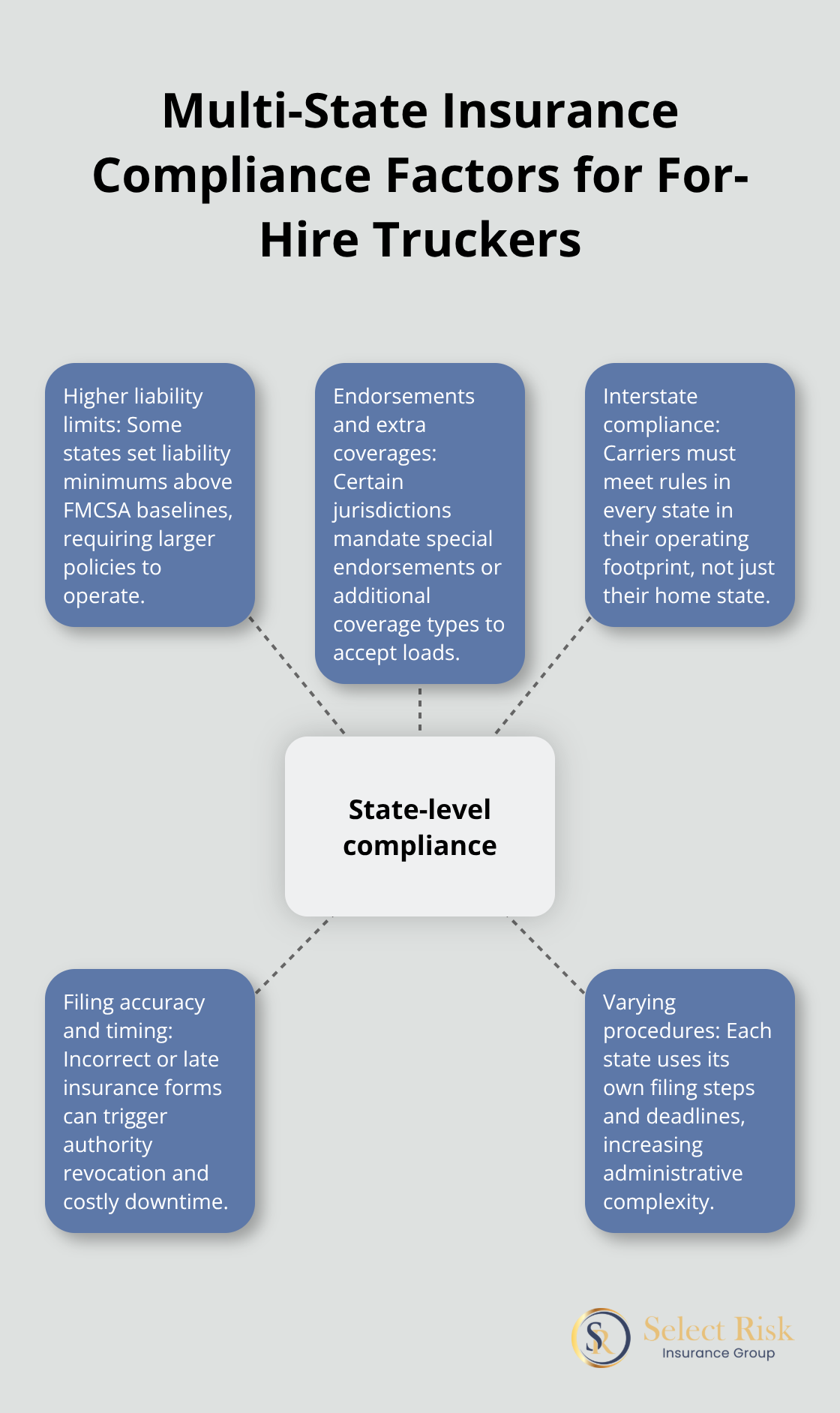

State Requirements Create Additional Complexity

States impose additional insurance requirements that exceed federal minimums, which creates a complex regulatory environment. Some states require higher liability limits than the FMCSA mandates, while others demand specific endorsements or additional coverage types. Interstate carriers must comply with requirements in every state where they operate, not just their home state.

Insurance forms that carriers file incorrectly or late can result in immediate revocation of authority within 20 days of application. Each state maintains its own filing procedures and deadlines (which vary significantly across jurisdictions).

Penalties That Can Destroy Your Business

The FMCSA will revoke authority for insurance violations, which effectively shuts down operations immediately. Fines can reach tens of thousands of dollars, while accidents without adequate coverage expose you to unlimited personal liability. Carriers who face million-dollar lawsuits often declare bankruptcy because they attempted to reduce insurance costs.

These severe consequences make proper coverage selection and maintenance a top priority for any serious trucking operation. The financial protection that comprehensive insurance provides becomes even more important when you consider the specific risks that for-hire truckers face daily.

How Does For-Hire Truck Insurance Protect Your Bottom Line

For-hire trucking operations face catastrophic financial exposure that extends far beyond vehicle repairs. Cargo losses alone can reach hundreds of thousands of dollars per incident, while third-party liability claims routinely exceed $1 million. The American Transportation Research Institute reports that the average cost of a truck crash with a fatality reaches $3.6 million, with property damage crashes that average $91,112. These figures demonstrate why basic liability coverage falls short of business asset protection.

Cargo Coverage Prevents Business-End Losses

Motor truck cargo insurance becomes mandatory when you transport high-value goods like electronics, pharmaceuticals, or machinery. Many freight brokers require $100,000 minimum cargo coverage before they award contracts, while some demand $250,000 or more. Electronics shipments can exceed $500,000 per load, which makes inadequate cargo coverage a recipe for bankruptcy. Theft, collision damage, and temperature failures in refrigerated units destroy cargo value instantly and leave carriers responsible for full replacement costs without proper coverage.

Third-Party Claims Create Unlimited Liability Exposure

Commercial truck accidents generate massive liability claims that destroy unprotected businesses. Medical expenses for serious injuries often exceed $1 million per person, while property damage to multiple vehicles and infrastructure can reach similar levels. The Federal Motor Carrier Safety Administration provides comprehensive crash statistics through their annual reporting system. Wrongful death settlements frequently exceed $5 million, while permanent disability cases can reach $10 million or more.

Revenue Protection Keeps Operations Active

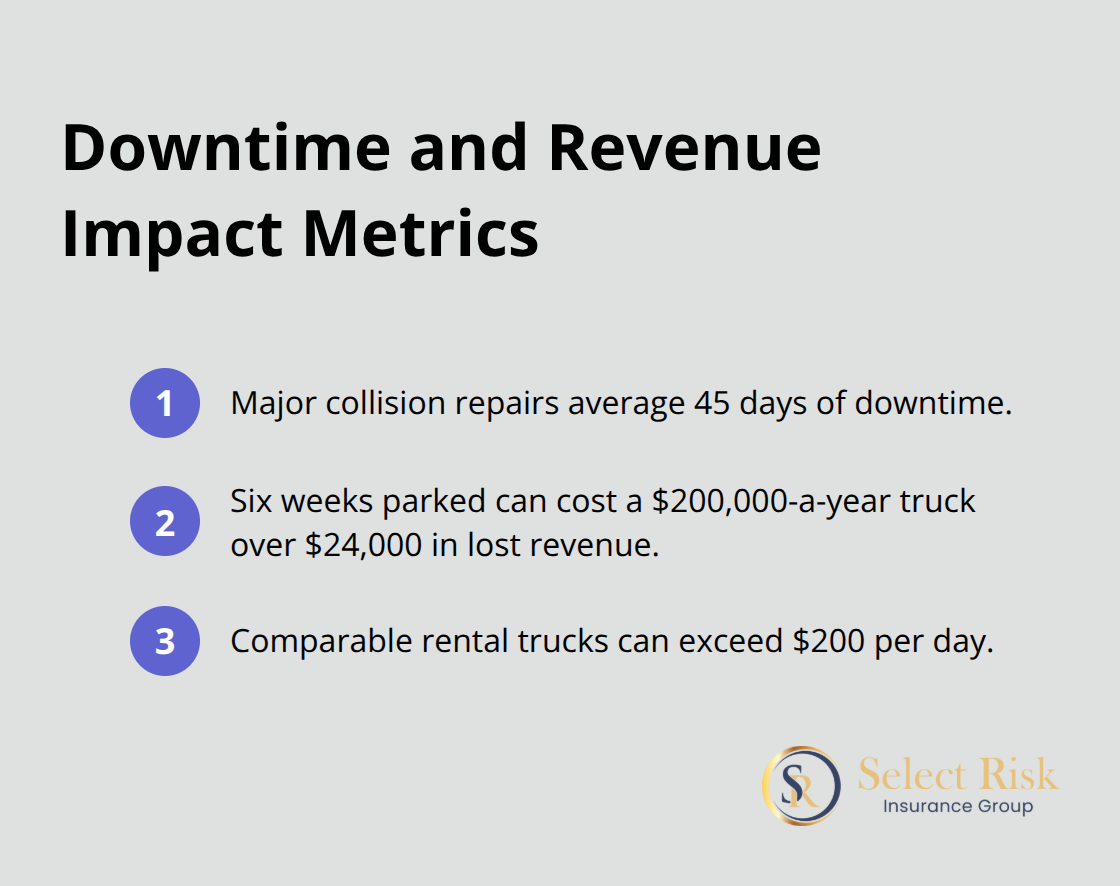

Business interruption coverage replaces lost income when accidents sideline your equipment for extended periods. Commercial truck repairs average 45 days for major collision damage, while total losses can take months to replace. A single truck that generates $200,000 annual revenue loses over $24,000 during a six-week repair period (based on standard downtime calculations). Rental truck coverage maintains operations during repairs, though rental costs can exceed $200 per day for comparable equipment.

These financial protection benefits work together with specific insurance types that address the unique risks for-hire truckers face in their daily operations.

Which Insurance Types Do For-Hire Truckers Need Most

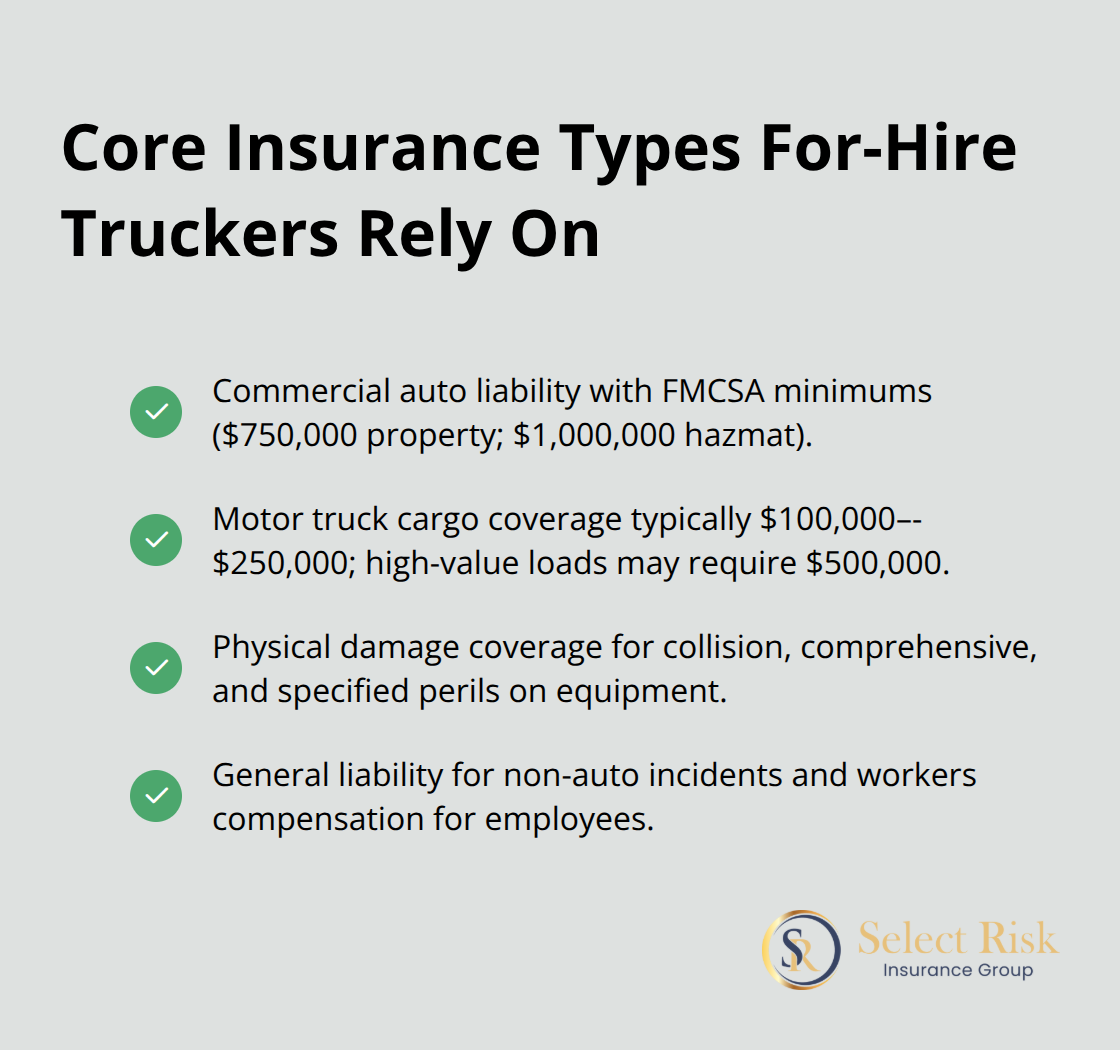

For-hire truckers need four essential insurance types that work together to protect against the industry’s highest-risk exposures. Commercial auto liability insurance forms the foundation with FMCSA-mandated minimums of $750,000 for property carriers and $1,000,000 for hazmat transporters, though smart operators carry $2,000,000 or more since truck accidents can result in significant settlements. Motor truck cargo insurance protects shipments with coverage that typically ranges from $100,000 to $250,000 per occurrence, while many electronics and pharmaceutical loads require $500,000 limits due to cargo values that routinely exceed those amounts.

Commercial Auto Liability Forms Your Foundation

Commercial auto liability insurance covers damages you cause to other people and property during accidents. The FMCSA sets minimum requirements at $750,000 for most property carriers, but this amount proves inadequate for serious accidents. Major trucking companies carry $2,000,000 to $5,000,000 in liability coverage because lawsuits from fatal accidents often exceed $3 million. Your liability policy also covers legal defense costs, which can reach $100,000 even for accidents where you bear no fault.

Physical Damage Coverage Protects Your Equipment Investment

Physical damage insurance covers collision, comprehensive, and specified perils for trucks that cost $150,000 to $200,000 new. Progressive reports that the average mechanical repair cost for commercial trucks reached $542 in 2020, while major collision repairs often exceed $50,000 and total losses can reach six figures. Deductibles range from $1,000 to $10,000 (with higher deductibles reducing premiums by 15-25 percent annually). Reefer breakdown coverage becomes essential for refrigerated units, as temperature failures can destroy entire loads worth hundreds of thousands of dollars within hours.

Cargo Insurance Protects Client Shipments

Motor truck cargo insurance covers damage or loss to freight you transport for customers. Most freight brokers require minimum cargo coverage of $100,000 before they award contracts, while high-value shipments demand $250,000 or more. Electronics loads often exceed $500,000 in value, making adequate cargo limits essential for contract eligibility. Cargo policies cover theft, collision damage, fire, and other perils that can destroy shipment value instantly.

General Liability and Workers Compensation Complete Protection

General liability insurance covers non-auto incidents like slip-and-fall accidents at loading docks, with standard limits of $1,000,000 per occurrence. Workers compensation becomes mandatory when you hire employees, with rates that vary from $2 to $15 per $100 of payroll depending on job classifications and state requirements. Owner-operators need non-trucking liability and bobtail coverage for personal use of their commercial vehicles, as standard policies exclude coverage when trucks operate without cargo or outside dispatch (these gaps can create significant liability exposure). Understanding commercial auto insurance costs helps you budget effectively for these essential coverages.

Final Thoughts

For-hire trucking operations cannot survive without comprehensive insurance coverage that meets federal mandates and protects against catastrophic financial losses. The FMCSA requires minimum liability coverage of $750,000 to $5,000,000 depending on cargo type, while smart operators carry higher limits since truck accidents routinely generate multi-million dollar settlements. Motor truck cargo insurance, physical damage coverage, and general liability protection work together to shield your business from the industry’s most devastating risks.

Proper insurance coverage creates long-term business stability by preventing single incidents from destroying years of hard work. Companies with adequate protection can focus on growth and operations instead of worrying about bankruptcy from unexpected accidents or cargo losses. The average truck crash with fatality costs $3.6 million (making comprehensive coverage an investment in business survival rather than an optional expense).

We at Select Risk Insurance Group help for-hire trucking companies navigate complex insurance requirements while finding competitive rates from reputable carriers. Our independent agency approach allows us to compare multiple options and build customized protection packages that fit your specific operations and budget. Contact Select Risk Insurance Group today to secure the comprehensive coverage your trucking business needs to operate safely and profitably for years to come.