Commercial Auto Insurance for Turo Hosts

Turo hosts face unique insurance challenges that standard personal auto policies simply don’t cover. When you rent your vehicle through car-sharing platforms, you’re operating a business that requires commercial protection.

Why do I need commercial auto insurance? The answer lies in coverage gaps that could leave you financially exposed during rental periods. We at Select Risk Insurance Group see Louisiana hosts struggle with these complex insurance requirements daily.

What Insurance Coverage Do Turo Hosts Actually Need?

Personal auto insurance policies contain specific exclusions that make them inadequate for Turo operations. The Insurance Information Institute reports that small business owners often lack adequate commercial auto insurance, which exposes them to significant financial risks. Standard personal policies typically exclude coverage when vehicles generate income, and this leaves hosts vulnerable during rental periods.

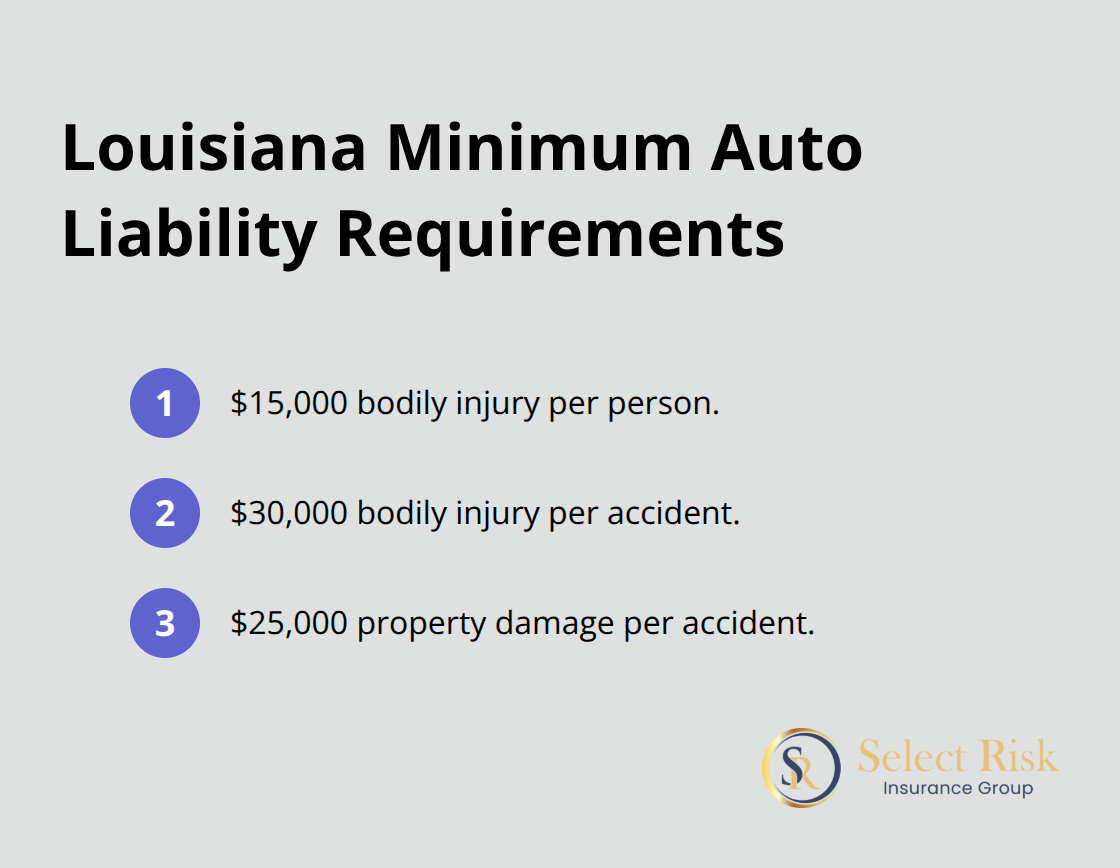

Louisiana state law requires minimum liability coverage of $15,000 per person and $30,000 per accident for bodily injury, plus $25,000 for property damage. These limits prove insufficient for commercial rental operations where claims often exceed personal policy limits.

Louisiana Car Sharing Insurance Requirements

Louisiana treats car-sharing differently than traditional rentals and requires hosts to maintain continuous insurance coverage throughout rental periods. The state mandates that peer-to-peer car-sharing platforms provide liability coverage, but this protection often includes high deductibles that range from $500 to $3,000.

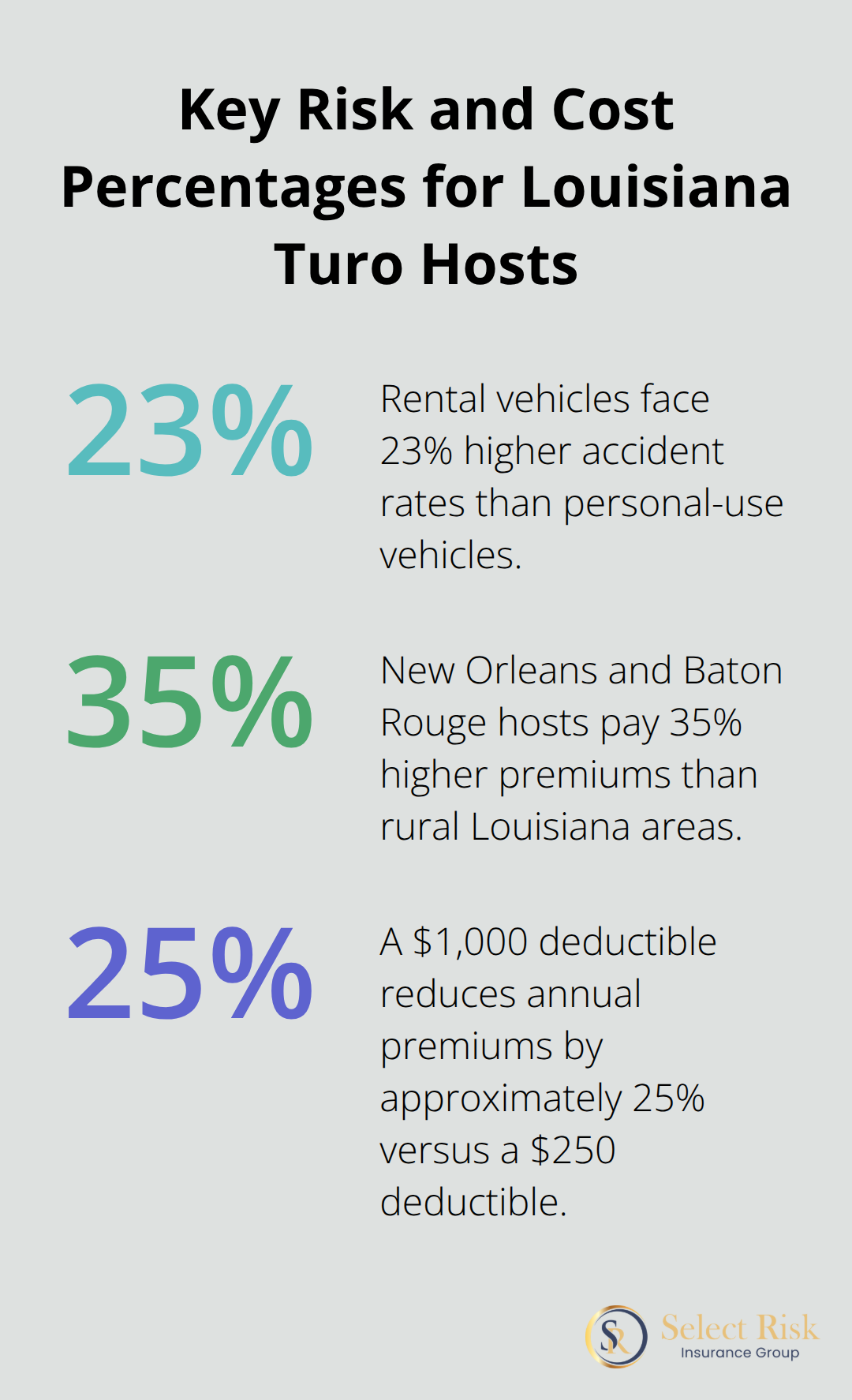

Louisiana hosts must verify their personal policies don’t contain commercial use exclusions before they list vehicles. The National Association of Insurance Commissioners found that rental vehicles face 23% higher accident rates than personal-use vehicles, which makes adequate coverage essential for financial protection.

Critical Coverage Gaps That Cost Hosts Money

Turo’s platform insurance creates dangerous coverage gaps during vehicle transitions and pickup periods. The National Highway Traffic Safety Administration data shows rental vehicles experience more frequent claims, yet many hosts operate without understanding their exposure during Period 1 coverage (when renters have booked but not yet taken possession).

Commercial auto policies eliminate these transition gaps while they provide consistent protection. Hosts without proper commercial coverage face average out-of-pocket expenses of $4,200 per incident when personal policies deny claims for commercial use.

Commercial Auto Policy Benefits

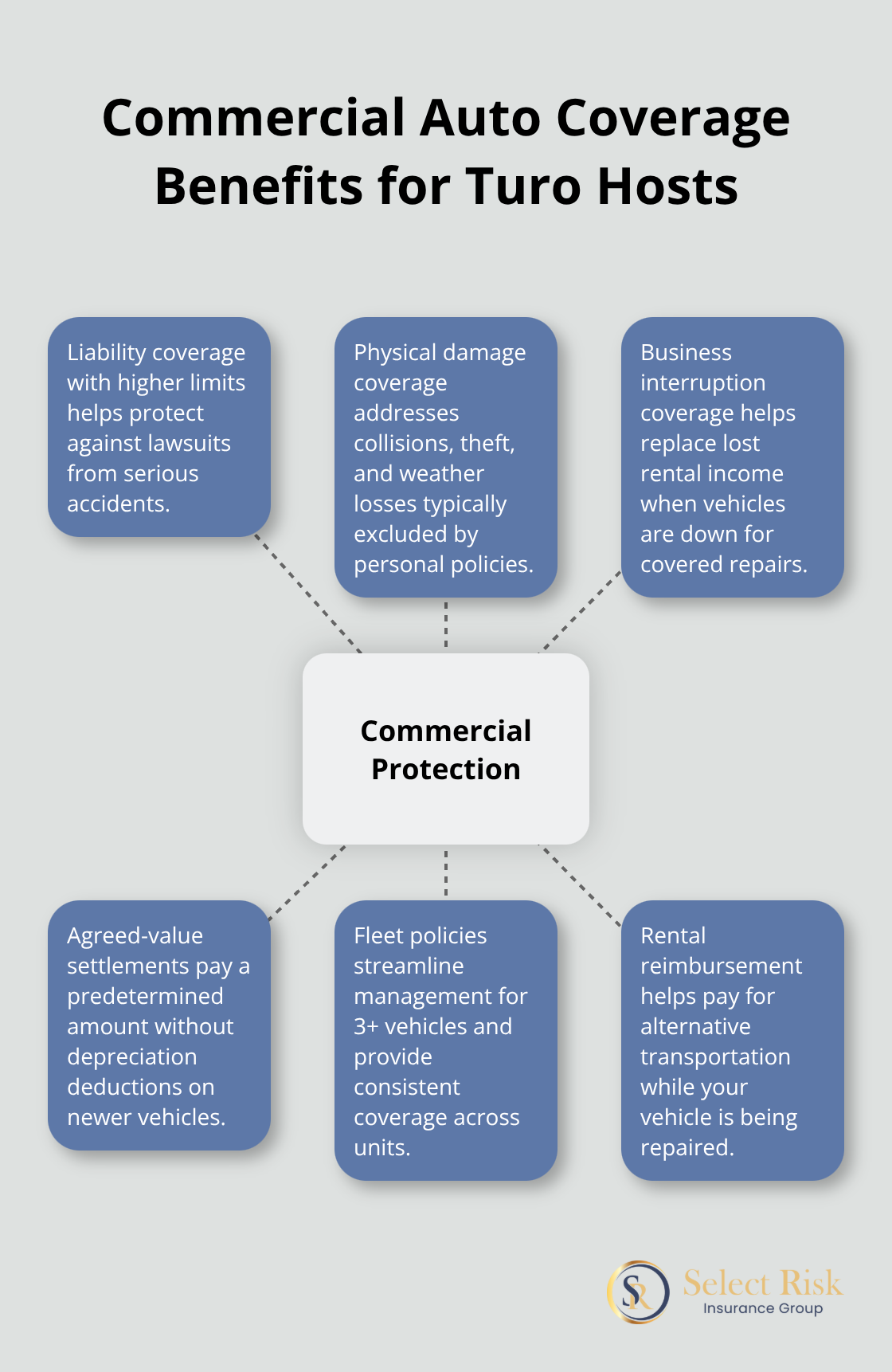

Commercial auto insurance addresses the unique risks that Turo hosts face daily. These policies cover liability, physical damage, and business interruption losses that personal policies exclude. Commercial coverage also provides higher liability limits that protect hosts against lawsuits from serious accidents.

The next step involves understanding specific commercial auto insurance options and how different policy structures can protect your Turo business investment.

Which Commercial Auto Policies Work Best for Turo Hosts

Commercial general liability policies protect Turo hosts against third-party claims that exceed vehicle damage costs. These policies cover bodily injury and property damage claims when renters cause accidents that surpass standard auto liability limits. The average commercial general liability policy costs between $400 and $800 annually for Turo operations and provides coverage from $1 million to $2 million per occurrence. This protection becomes essential when accident claims involve multiple vehicles or serious injuries that reach six-figure settlements.

Commercial Auto Coverage That Protects Your Business

Commercial auto policies for Turo hosts must include comprehensive and collision coverage with agreed-value settlements rather than actual cash value. Agreed-value policies pay the predetermined amount without depreciation deductions, which protects hosts from losses on newer vehicles. Fleet policies work best for hosts with three or more vehicles because they reduce administrative costs and provide consistent coverage across all units.

Commercial policies average $1,800 to $2,400 per vehicle annually but eliminate the coverage gaps that cost hosts thousands in denied claims. Physical damage coverage should include rental reimbursement that pays for alternative transportation while your vehicle undergoes repairs.

Gap Coverage That Prevents Financial Disasters

Period X insurance specifically targets peer-to-peer rentals and fills the dangerous coverage gaps between personal policies and platform protection. This specialized coverage operates during transition periods when vehicles move between personal use and rental status. Standard gap insurance won’t work for Turo operations because it only covers loan balances, not business interruption losses.

Turo hosts need commercial gap coverage that includes loss of rental income protection, which pays up to 80% of projected rental earnings while vehicles remain out of service. Smart hosts combine this with excess liability coverage that provides $5 million in protection above their primary commercial auto limits.

Fleet Management and Technology Integration

Modern commercial auto policies for Turo hosts include GPS tracking capabilities that monitor vehicles throughout rental periods. These systems provide real-time location data and can send alerts when vehicles leave designated areas (geofencing alerts help prevent unauthorized use). Built-in tracking devices also help with theft recovery and provide evidence for insurance claims when accidents occur.

Fleet management features allow hosts to add or remove vehicles online with 24/7 account access for policy changes. The technology integration helps hosts maintain better control over their rental operations while meeting insurance requirements that traditional policies cannot address.

Understanding the cost factors and coverage considerations will help you select the right commercial auto insurance structure for your specific Turo operation and budget requirements.

How Much Does Commercial Auto Insurance Cost for Turo Hosts

Commercial auto insurance premiums for Turo hosts depend on vehicle value, rental frequency, and location within Louisiana. Premium calculations start with your vehicle’s agreed value, annual mileage estimates, and rental days per month. Insurance companies apply a multiplier system where every 10 rental days monthly increases your base premium by 15-20%.

Hosts who operate luxury vehicles worth over $40,000 face premiums from $2,800 to $4,200 annually, while economy vehicles typically cost $1,400 to $2,100 per year. New Orleans and Baton Rouge hosts pay 35% higher premiums than rural Louisiana areas due to increased theft and accident rates. Commercial auto claims for rental vehicles average higher amounts compared to personal use claims.

Premium Factors That Drive Your Costs

Vehicle age and safety ratings significantly impact your commercial auto premiums. Certain vehicles qualify for lower premiums due to higher safety ratings, with vehicles earning top safety awards potentially reducing premiums by 10-15%. Your personal credit score also affects commercial auto rates, with excellent credit scores reducing premiums by up to 20% compared to poor credit ratings.

Annual mileage projections matter more for Turo operations than personal policies because rental vehicles accumulate miles faster. Hosts who accurately estimate annual mileage avoid mid-term premium adjustments that can increase costs by 25-30% when actual usage exceeds projections.

Smart Deductible Strategies That Save Money

Commercial auto deductibles for Turo hosts should balance monthly premium savings against potential out-of-pocket expenses. A $1,000 deductible reduces annual premiums by approximately 25% compared to $250 deductibles, but hosts must maintain cash reserves for multiple potential claims.

The claims process requires immediate notification within 24 hours and detailed documentation. This includes police reports, renter information, and vehicle condition photos. Most commercial insurers process Turo-related claims within 7-10 business days when proper documentation exists. Hosts who maintain detailed rental logs and pre-trip inspection photos experience faster claim resolution times.

Revenue Protection Prevents Business Disasters

Business interruption coverage pays 75-85% of projected rental income while vehicles undergo repairs after covered claims. This protection costs an additional $200-400 annually but prevents income losses that average $1,800 per month for popular rental vehicles.

Revenue protection activates after a 48-hour wait period and continues for up to 30 days during repair periods. Hosts must provide rental history documentation and market rate comparisons to establish income baselines for coverage calculations. Loss of use coverage works differently because it only pays predetermined daily amounts rather than actual income percentages, which makes revenue protection the superior choice for active Turo operations.

Final Thoughts

Why do I need commercial auto insurance as a Turo host? The answer becomes clear when you consider the financial risks that personal policies simply won’t cover. Louisiana hosts who operate without proper commercial protection face average losses of $4,200 per incident when claims get denied. We at Select Risk Insurance Group understand the complex insurance landscape that Turo hosts navigate daily.

Independent agents who specialize in commercial auto coverage provide access to multiple insurance carriers and competitive options. These professionals compare policies from different companies to find coverage that matches your specific rental operation needs. Louisiana Turo hosts should take immediate action to protect their business investments and review their current personal auto policy exclusions.

The commercial auto insurance market continues to evolve to meet car-sharing demands, but hosts cannot afford to wait for perfect solutions. Contact experienced commercial insurance professionals who understand peer-to-peer rental risks and can structure policies that eliminate dangerous coverage gaps (these gaps cost hosts thousands in denied claims). Select Risk Insurance Group offers comprehensive commercial auto insurance solutions designed specifically for Louisiana business owners who need reliable protection.