Non-Owned Commercial Auto Insurance Explained

Many business owners wonder: does commercial auto insurance cover personal use when employees drive their own vehicles for work? The answer involves understanding non-owned commercial auto insurance.

This specialized coverage protects your business when employees use personal cars for company tasks. We at Select Risk Insurance Group see Louisiana businesses face significant liability gaps without this protection.

What Does Non-Owned Commercial Auto Insurance Actually Cover

Non-owned commercial auto insurance protects your business when employees drive vehicles you don’t own for work purposes. This coverage applies to personal cars, rental vehicles, and borrowed vehicles used during business activities.

Primary Protection Against Business Liability

The insurance provides liability protection when an employee causes an accident while driving for your company. According to Insureon data, the average policy limit among their policyholders reaches $1 million, which shows how businesses protect against substantial claims. Louisiana businesses face particular risks because state minimum liability requirements may not cover severe accidents that involve company activities.

Secondary Coverage After Personal Insurance

Your non-owned coverage activates only after the employee’s personal auto insurance limits are exhausted. This secondary protection prevents your business from facing lawsuits when personal policies fall short. The Hartford provides hired and non-owned auto coverage, which demonstrates its widespread necessity across the country.

Distinct from Standard Commercial Auto Policies

Standard commercial auto insurance covers vehicles your business owns, leases, or finances. Non-owned coverage fills the gap for vehicles you don’t control but still use for business. Progressive (the nation’s number one commercial auto insurer based on SNL Financial’s 2023 data) shows that businesses need both types of protection. The distinction matters because personal auto policies typically exclude business use, which leaves dangerous coverage gaps when employees run errands or visit clients.

Understanding what this insurance covers helps you identify whether your business needs this protection, but knowing who specifically requires this coverage will help you make the right decision.

Which Businesses Must Have Non-Owned Coverage

Restaurants, construction companies, and delivery services face the highest risk when employees drive personal vehicles for work. Louisiana businesses often discover their massive liability exposure only after an accident occurs. The national average monthly cost for commercial auto insurance reaches $216, but non-owned coverage costs significantly less while it protects against lawsuits that can destroy your business.

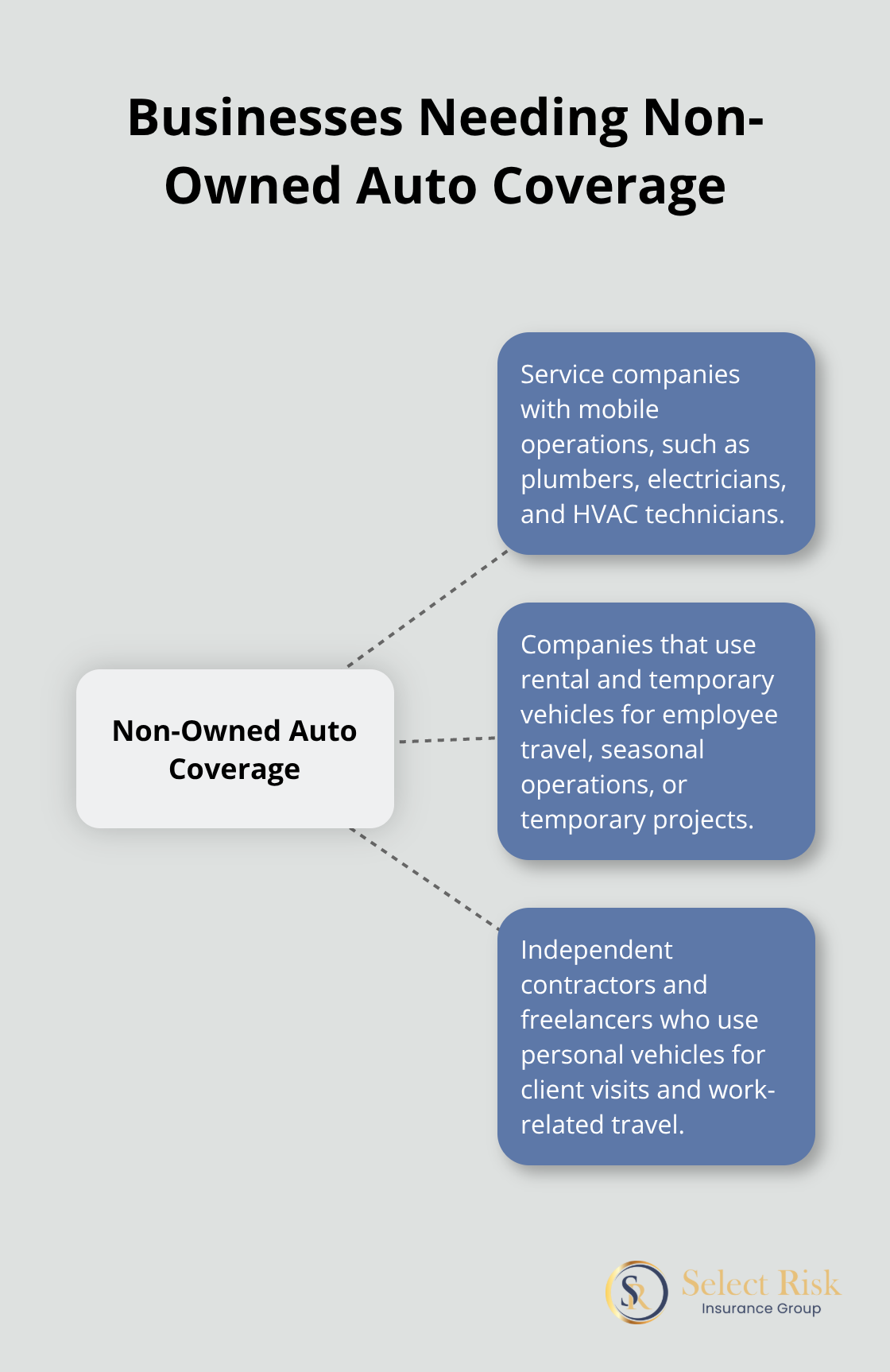

Service Companies with Mobile Operations

Plumbers, electricians, and HVAC technicians who send employees to job sites with personal trucks need this protection immediately. These contractors average $272 monthly for their commercial auto insurance according to 2024 data, but non-owned coverage adds minimal cost for maximum protection. Real estate agents drive clients to properties, home healthcare workers visit patients, and repair technicians make service calls-all activities create liability for their employers. Leavitt Group (the 18th largest independent property and casualty insurance broker according to Insurance Journal) reports that businesses without clear vehicle use policies face the highest claim rates.

Companies That Use Rental and Temporary Vehicles

Businesses that rent vehicles for employee travel, seasonal operations, or temporary projects must secure hired auto coverage. Marketing firms send teams to trade shows, seasonal retailers expand delivery capacity, and companies replace fleet vehicles during maintenance-all situations require this protection. The average policy limit of $1 million among Insureon policyholders reflects the serious financial risks these situations create. Small businesses often rent vehicles and assume their general liability covers everything, but rental car accidents can generate claims that exceed $500,000 in severe injury cases.

Independent Contractors and Freelancers

Solo contractors who use personal vehicles for client visits face unique exposure because personal auto policies typically exclude business use. Consultants travel to client offices, photographers transport equipment to events, and freelance writers conduct interviews at various locations. These professionals often work without the safety net of employer-provided coverage, which makes non-owned protection essential for their financial security.

The specific coverage details and limitations of non-owned policies determine how well they protect your business in different accident scenarios.

Coverage Details and Limitations

Non-owned commercial auto insurance provides specific liability protection that covers bodily injury and property damage when employees cause accidents while they drive personal vehicles for work. The coverage responds with limits that typically range from $1 million to $2 million per occurrence, according to Insureon data that shows average policy limits among their policyholders. Louisiana businesses need these high limits because medical costs from severe accidents regularly exceed $500,000, and property damage claims can reach similar amounts when commercial vehicles or expensive equipment suffer damage.

Major Exclusions That Leave You Exposed

This insurance will not cover physical damage to the employee’s personal vehicle, medical expenses for injured employees, or cargo damage that occurs during business trips. The policy excludes coverage when employees use vehicles for personal errands unrelated to work, even during business hours. Workers’ compensation handles employee injuries, but your non-owned policy stops payment when the accident involves criminal activity, racing, or vehicles that operate outside the United States. Most importantly, coverage only activates after the employee’s personal auto insurance pays its limits first, which means you face direct exposure if their personal policy has lapsed or carries minimum state limits.

Deductible Structure and Cost Management

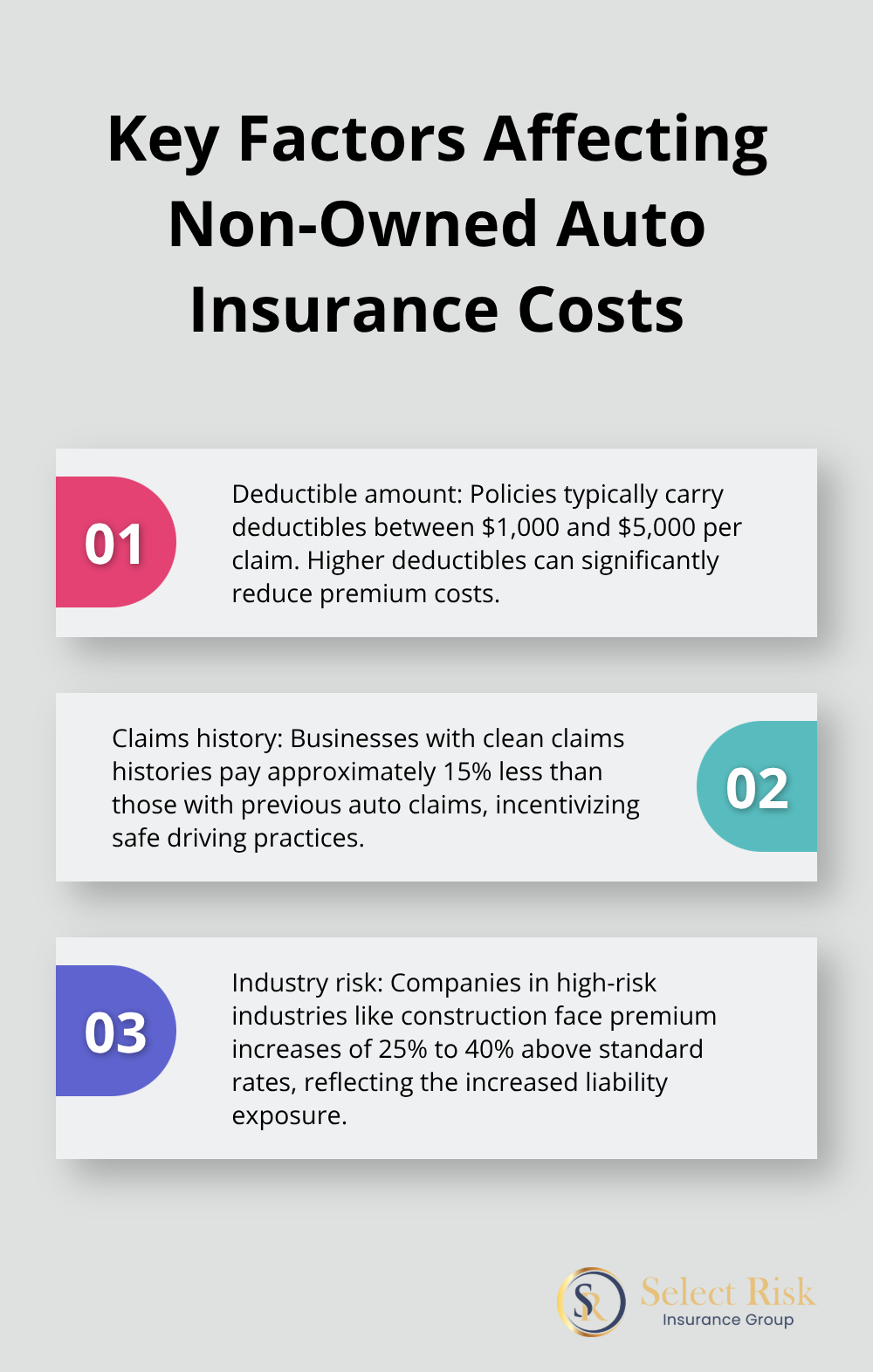

Non-owned auto policies typically carry deductibles between $1,000 and $5,000 per claim, with higher deductibles that reduce your premium costs significantly. The Hartford and Progressive offer these policies as endorsements to general liability coverage, which keeps costs lower than separate policies. Businesses with clean claims histories pay approximately 15% less than those with previous auto claims, while companies in high-risk industries like construction face premium increases of 25% to 40% above standard rates.

Premium Factors That Affect Your Costs

Annual premium payments reduce total costs by 8% to 12% compared to monthly installments (a strategy that saves money immediately). Companies that maintain strict driver qualification standards can lower their rates through most insurers’ risk management credit programs. Employee demographics particularly affect costs, with age, driving experience, credit history, and vehicle type being factors that influence the rates and increase your overall policy expense.

Final Thoughts

Louisiana businesses that ask “does commercial auto insurance cover personal use” often discover they need non-owned coverage to protect against employee vehicle accidents. This specialized insurance prevents lawsuits from destroying your company when personal auto policies fall short during work-related activities. The cost of non-owned coverage represents a fraction of potential lawsuit damages, especially when accidents involve serious injuries or expensive property damage.

We at Select Risk Insurance Group understand Louisiana’s unique business risks and work with multiple carriers to find you comprehensive coverage at competitive prices. Our independent agency status allows us to compare policies from various insurers and select the protection that fits your specific operations and budget requirements. Businesses without this protection face direct liability exposure that can reach hundreds of thousands of dollars in a single claim.

A coverage analysis of your current policies and employee vehicle use patterns starts your protection process. Select Risk Insurance Group provides personalized insurance solutions that address your liability gaps while maintaining competitive rates through our carrier relationships (which gives you more options than captive agents). Contact us today to review your non-owned auto insurance needs and secure the protection your Louisiana business requires before an accident occurs.