Commercial Auto Insurance for Uber Black Drivers

Uber Black drivers face unique insurance challenges that standard personal auto policies simply can’t handle. The luxury vehicle requirements and commercial nature of the service create significant coverage gaps.

We at Select Risk Insurance Group see many drivers struggling with commercial auto insurance rates that don’t match their specific needs. Louisiana’s regulations add another layer of complexity to an already confusing landscape.

Why Personal Auto Insurance Fails Uber Black Drivers

Personal Auto Policies Exclude Commercial Use

Personal auto insurance policies contain explicit exclusions for commercial activities, which makes them worthless for Uber Black drivers. These policies specifically exclude coverage for livery or receiving compensation for driving. Insurance companies like State Farm and Allstate routinely deny claims once they determine the accident occurred during rideshare activities.

Personal policies simply weren’t designed for the commercial risks that Uber Black operations create.

Uber’s Insurance Gaps Leave Drivers Vulnerable

Uber provides limited coverage that creates dangerous gaps for drivers. Their policy only activates during active rides with passengers, which leaves drivers unprotected while they wait for ride requests or drive to pickup locations. This coverage gap can last hours during slow periods and exposes drivers to significant financial risk.

Uber’s liability coverage starts at $1 million per incident, but their comprehensive and collision coverage requires a $2,500 deductible. More concerning, Uber’s insurance acts as secondary coverage, which means your personal insurance must respond first. Since personal policies exclude commercial use, drivers face complete coverage denial.

Louisiana State Requirements Create Additional Complications

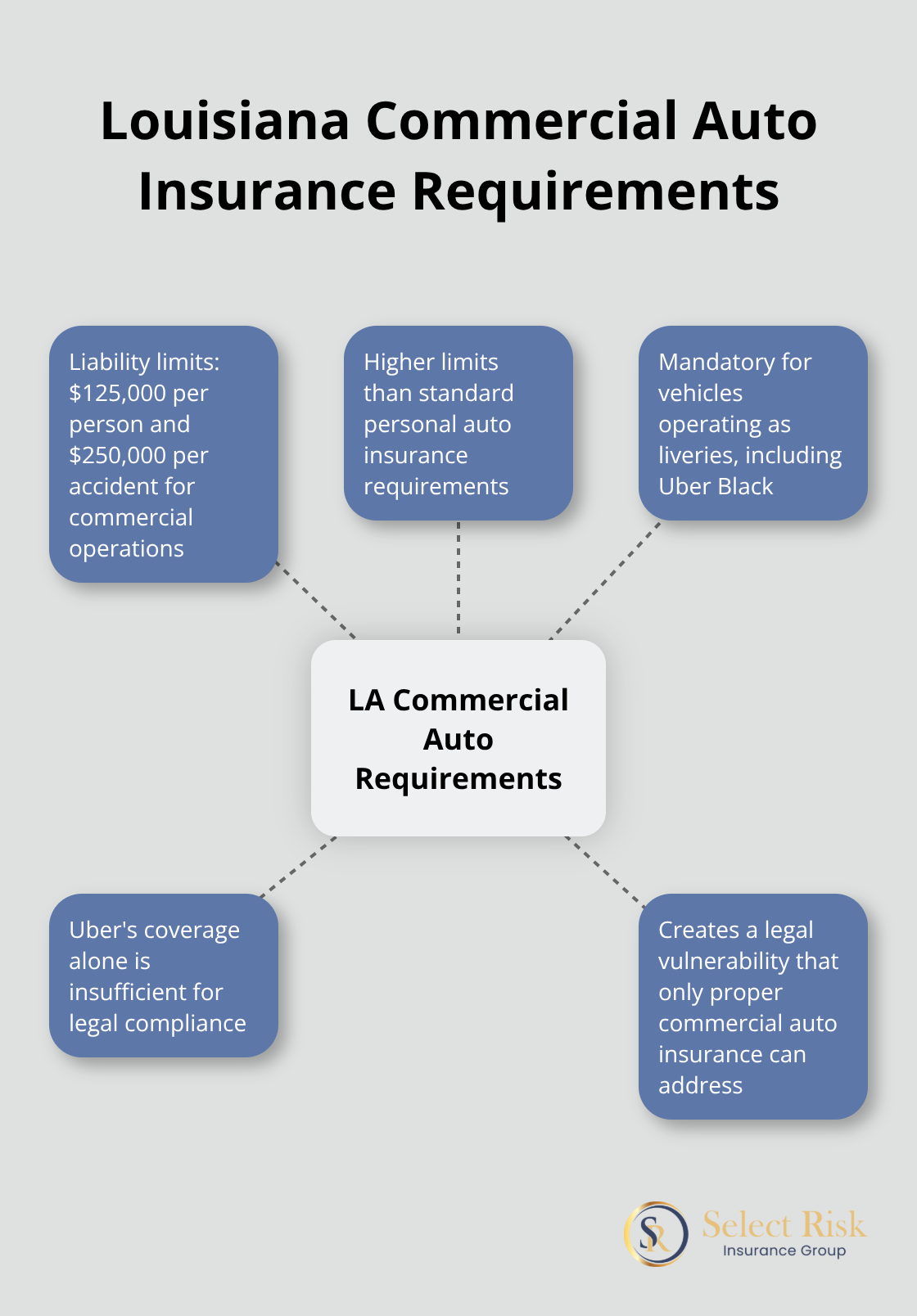

Louisiana requires commercial auto insurance for vehicles that operate as liveries, which makes Uber’s coverage insufficient for legal compliance. The Louisiana Department of Insurance mandates minimum liability limits of $125,000 per person and $250,000 per accident for commercial operations (significantly higher than standard personal auto requirements).

These state requirements mean Uber Black drivers cannot rely on the platform’s insurance alone. The gap between Uber’s coverage and Louisiana’s commercial vehicle standards creates a legal vulnerability that only proper commercial auto insurance can address.

Commercial auto insurance options specifically designed for luxury rideshare operations offer the comprehensive protection these drivers need.

What Commercial Auto Options Work for Uber Black Drivers

Progressive Rideshare Coverage Falls Short for Luxury Operations

Progressive offers rideshare endorsements in 47 states, but their coverage caps at standard vehicle values and excludes luxury car operations like Uber Black. Their rideshare endorsement only covers vehicles worth up to $50,000, while Uber Black requires luxury vehicles that often exceed $60,000. Progressive charges monthly premiums that start at $25 for rideshare endorsements, but this coverage becomes worthless when your BMW or Mercedes gets totaled during commercial use.

State Farm and Geico follow similar patterns with rideshare endorsements that explicitly exclude luxury livery services. These major carriers treat Uber Black differently from standard rideshare because of the commercial livery classification.

Commercial Auto Policies Provide Complete Protection

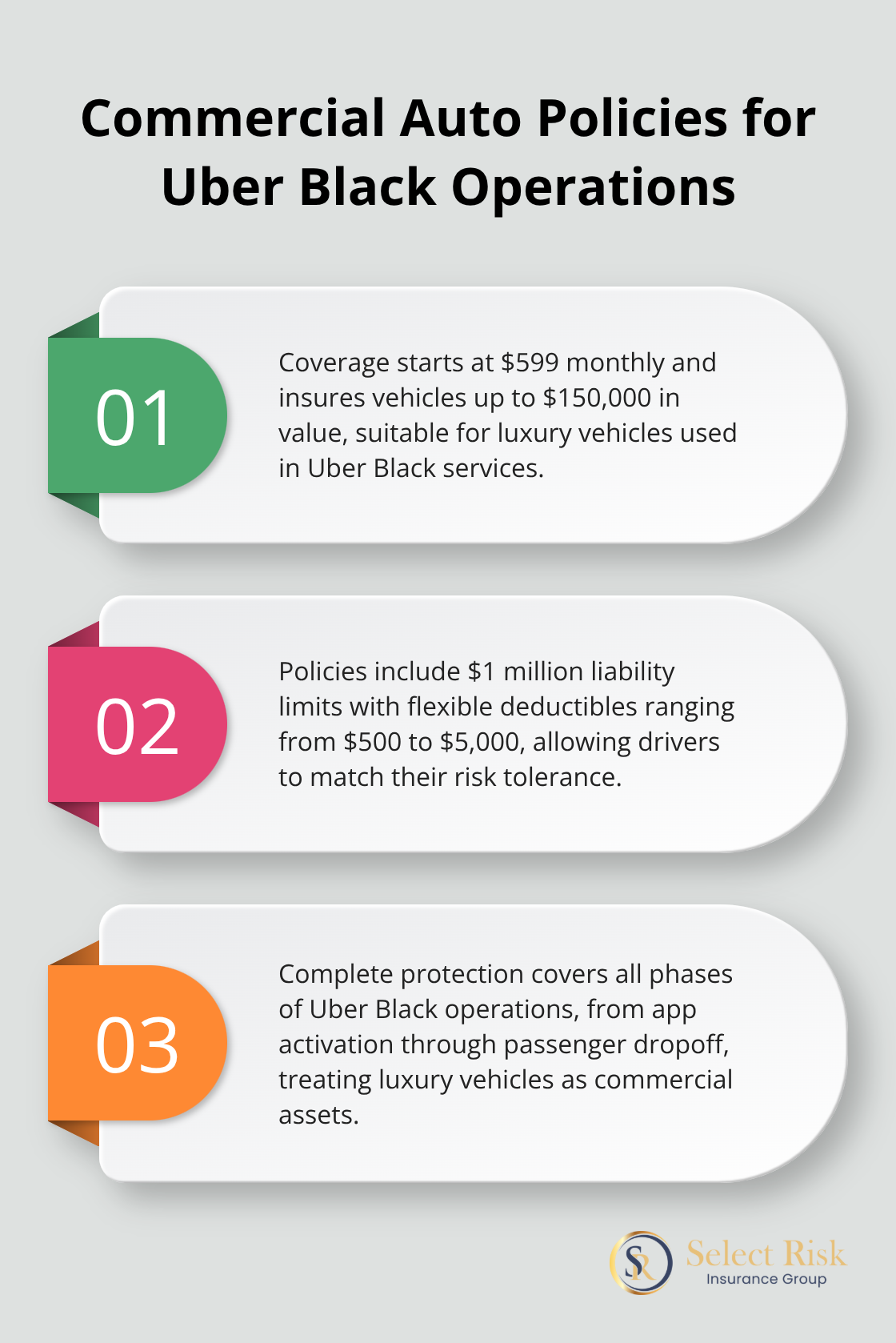

Commercial auto policies from carriers like American Business Insurance start at $599 monthly for Uber Black operations and cover vehicles up to $150,000 in value. ABI insures over 50,000 commercial vehicles nationwide and offers same-day certificate issuance for immediate compliance. Their policies include $1 million liability limits with deductibles that range from $500 to $5,000 (which gives drivers flexibility to match their risk tolerance).

Commercial policies cover all phases of Uber Black operations, from app activation through passenger dropoff. Unlike rideshare endorsements, these policies treat your luxury vehicle as a commercial asset that deserves full protection.

Hybrid Solutions Create Dangerous Coverage Holes

Some drivers attempt to mix personal policies with commercial endorsements, but this approach creates liability gaps that insurance companies exploit during claims. Insurance adjusters routinely investigate rideshare accidents to determine coverage phase, and any ambiguity results in claim denial. Drivers should find out what insurance policies the TNC has to protect drivers and passengers, and how much liability coverage those policies offer.

These coverage gaps become particularly expensive when luxury vehicles sustain damage during the gray areas between personal and commercial use (which happens frequently during Uber Black operations).

Understanding these insurance limitations helps drivers make informed decisions about premium costs and coverage strategies that actually protect their investment.

What Drives Commercial Auto Insurance Costs

Luxury Vehicle Values Set Premium Foundations

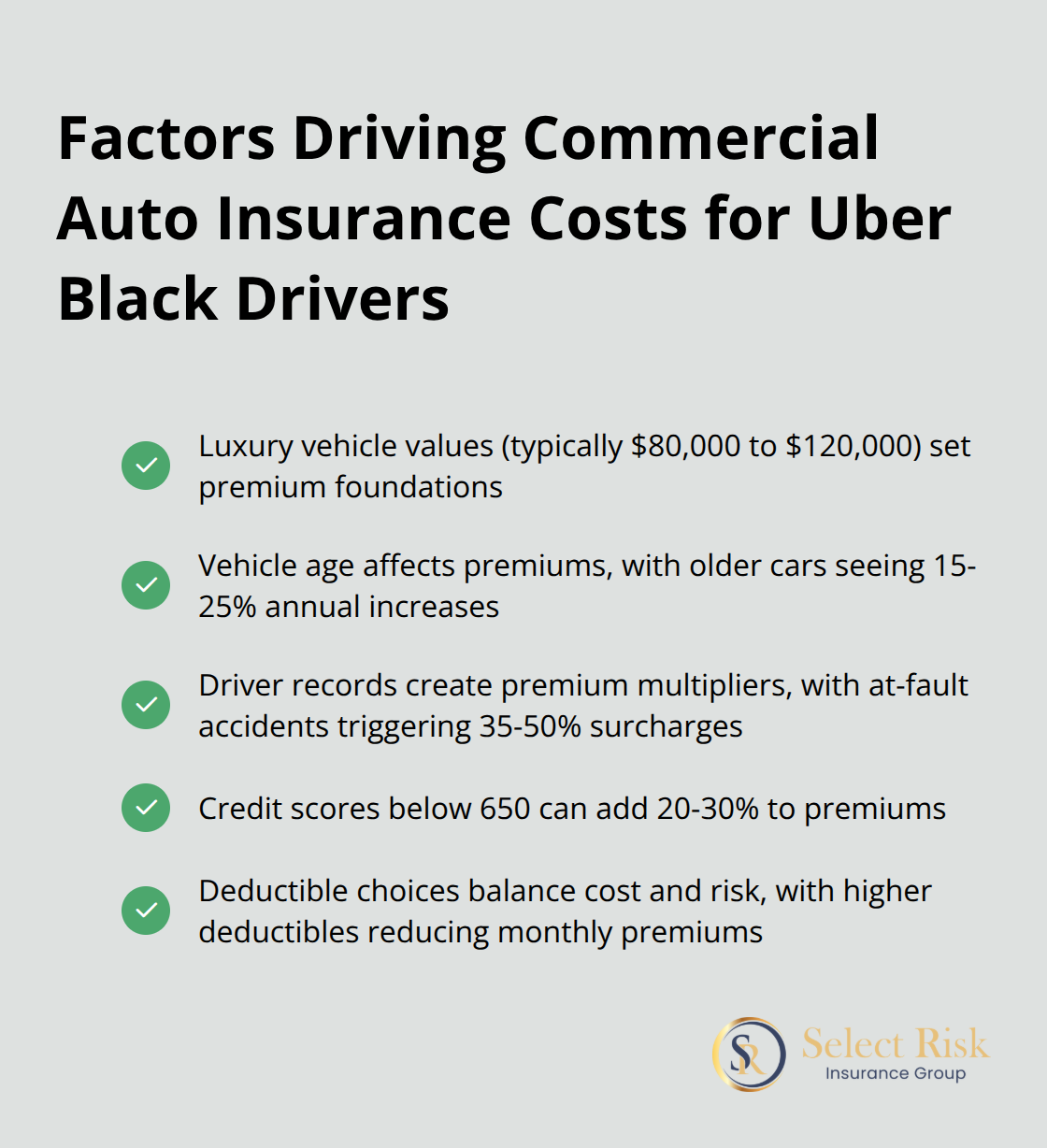

Luxury vehicle values push commercial auto premiums to levels that shock most Uber Black drivers. Mercedes S-Class and BMW 7 Series vehicles that qualify for Uber Black typically cost $80,000 to $120,000, which drives monthly commercial premiums from $599 to over $1,200. American Business Insurance bases premiums on replacement costs, and a $100,000 luxury sedan costs 40% more to insure than a $60,000 vehicle. Vehicle age matters significantly – cars over three years old see premium increases of 15-25% annually as depreciation accelerates repair costs.

Driver Records Create Premium Multipliers

Commercial carriers scrutinize records more aggressively than personal auto insurers. Rideshare drivers commonly have higher commercial auto insurance coverage requirements than other vehicles on the road, while at-fault accidents trigger 35-50% surcharges. Uber Black drivers need 4.85-star ratings and clean records, but insurance companies apply additional commercial standards. DUI convictions make commercial coverage nearly impossible to obtain (with most carriers requiring five years of clean history before they consider applications). Credit scores below 650 add another 20-30% to premiums because commercial auto insurance policies treat drivers as business operators.

Deductible Strategies Balance Cost and Risk

Smart Uber Black drivers choose $2,500 deductibles to reduce monthly premiums by $150-200 while they maintain reasonable out-of-pocket exposure. Lower $500 deductibles increase premiums substantially without they provide proportional value for professional drivers who understand vehicle maintenance. Coverage limits of $1 million liability represent the minimum acceptable protection, but drivers who operate in high-litigation areas like New Orleans should consider $2 million limits that cost only 15% more. Comprehensive coverage with $1,000 deductibles protects against theft and vandalism that luxury vehicles attract more frequently than standard cars.

Final Thoughts

Uber Black drivers in Louisiana must obtain commercial auto insurance to operate legally and protect their luxury vehicle investments. Personal auto policies and rideshare endorsements fail to cover the commercial nature of luxury livery services. This leaves drivers exposed to significant financial risk when accidents occur during commercial operations.

Commercial auto insurance rates for Uber Black operations start at $599 monthly but provide comprehensive protection that covers all phases of operation. Louisiana’s commercial vehicle requirements make this coverage mandatory rather than optional. Drivers who attempt to operate with inadequate insurance face claim denials and potential legal violations (which can result in suspended operations and financial penalties).

We at Select Risk Insurance Group help Uber Black drivers navigate Louisiana’s complex insurance landscape. Our independent agency represents multiple carriers to find competitive commercial auto solutions that match your specific needs and budget. Contact Select Risk Insurance Group for personalized guidance through the commercial insurance process and quotes from carriers that specialize in luxury rideshare operations.