Commercial Auto Insurance Estimate Calculator Guide

Commercial auto insurance costs can vary dramatically between businesses, making accurate estimates essential for budget planning. A commercial auto insurance estimate calculator helps business owners get preliminary pricing before speaking with agents.

We at Select Risk Insurance Group see many companies struggle with unexpected insurance costs because they skip this planning step. Getting reliable estimates upfront prevents budget surprises and helps you make informed coverage decisions.

How Commercial Auto Insurance Calculators Work

Commercial auto insurance calculators process your business information through algorithms that mirror insurance company underwriting systems. These tools analyze vehicle type, annual mileage, operating radius, driver records, and coverage preferences to generate premium estimates. Most calculators provide low, mid, and high premium ranges rather than single numbers, which gives you a realistic cost projection before you contact agents.

The Data Behind Your Estimates

Insurance calculators pull from massive databases of claims data and actuarial tables. Vehicle class heavily influences rates, with heavier commercial trucks costing significantly more than vans due to damage potential. Your annual mileage directly impacts risk calculations – businesses that drive over 50,000 miles annually face substantially higher premiums than those under 25,000 miles.

Operating radius matters too. Interstate operations increase costs compared to local delivery routes within a 50-mile radius. The calculator weighs these factors against historical loss data to predict your premium range.

Algorithm Limitations and Accuracy Ranges

Calculator estimates typically fall within 15-20% of actual quotes, but several factors create gaps between initial estimates and final rates. Insurance companies conduct detailed driver record checks, vehicle inspections, and loss history reviews that calculators cannot perform. Your three-year claims history significantly impacts final rates – even one at-fault accident can increase premiums by 25-40% beyond calculator estimates.

State regulations and carrier-specific underwriting guidelines influence final rates in ways generic calculators cannot predict. Each insurer applies different weight to risk factors (such as driver age versus vehicle type), which explains why quotes vary between carriers even with identical information.

What Calculators Cannot Assess

Standard calculators miss several critical factors that affect your actual premium. They cannot evaluate your specific business operations, safety programs, or driver training protocols. Vehicle maintenance records, garage locations, and security measures also remain invisible to these tools.

Most importantly, calculators cannot account for carrier appetite – some insurers actively seek certain business types while others avoid them entirely. This market dynamic significantly impacts both availability and rates, making the next step of gathering actual quotes from multiple carriers essential for accurate budget planning.

How Do You Get Accurate Calculator Estimates

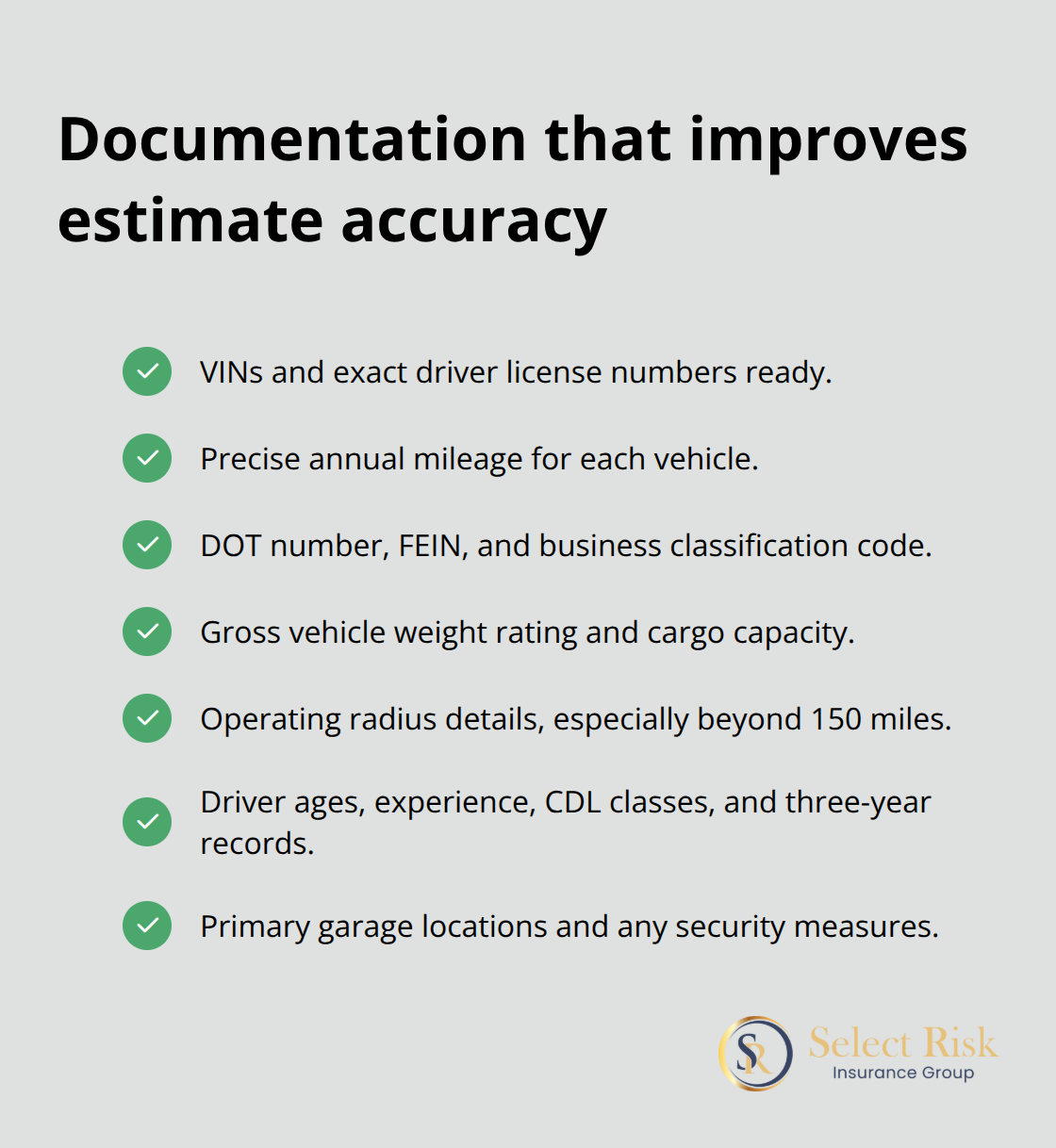

Successful commercial auto insurance calculations require specific preparation and attention to detail. Vehicle identification numbers, exact driver license numbers, and precise annual mileage figures produce the most reliable estimates. You must gather your Department of Transportation number, FEIN, and business classification code beforehand to save time and improve accuracy.

Driver records from the past three years (including violation dates and claim amounts) significantly impact your estimates. Clean records earn substantially lower rates than those with violations or claims.

Essential Documentation for Precise Estimates

Your calculator results depend heavily on accurate vehicle specifications and usage data. Commercial trucks require gross vehicle weight ratings, cargo capacity, and radius of operation details. The Hartford’s FleetAhead data shows that vehicles operating beyond 150-mile radius face premium increases of 15-30%.

Business location affects rates substantially – urban areas with higher crime rates increase comprehensive coverage costs by 20-50% compared to rural locations. Driver ages, experience levels, and CDL classifications must be exact. Insureon data reveals that drivers under 25 or over 65 create premium variations of up to 35% from standard rates.

Critical Input Errors That Cost Money

The most expensive mistakes involve underreporting annual mileage or misclassifying vehicle usage. You cannot list a delivery truck as occasional use instead of commercial hauling – this can invalidate coverage entirely. Nationwide’s underwriting guidelines show that mileage underestimation by just 10,000 miles annually can result in 20% premium increases during policy audits.

Never round down gross vehicle weights or passenger capacities – these factors directly determine liability exposure. You must include all secondary drivers or part-time operators to avoid coverage gaps that calculators cannot detect. State-specific requirements vary dramatically, so confirm your operating states before calculation to prevent costly oversights that emerge during final underwriting.

These preparation steps set the foundation for meaningful estimates, but even perfect data entry cannot guarantee accuracy without understanding the broader factors that shape your final rates.

What Drives Your Commercial Auto Premium Costs

Vehicle specifications create the foundation of your insurance rates, with gross vehicle weight as the primary cost multiplier. Commercial auto insurance costs vary significantly by industry type and vehicle classifications. Commercial trucks over 26,000 pounds generate premiums 300-400% higher than cargo vans under 10,000 pounds. Your operating radius compounds these costs significantly – interstate operations increase rates by 25-35% compared to local delivery within 50 miles. Annual mileage creates exponential cost increases beyond 75,000 miles yearly, with high-mileage fleets facing premium surcharges of 40-60% above standard rates.

Driver Records Shape Your Risk Profile

Your three-year claims history determines premium calculations more than any other single factor. Insureon research reveals that businesses with clean records secure rates 35-50% lower than those with violation histories. One DUI conviction increases commercial premiums by 65-85%, while speeding violations above 15 mph over the limit add 20-30% to base rates. Driver age demographics significantly impact costs – operators under 25 or over 65 create premium variations up to 35% from standard rates (with younger drivers typically facing the highest increases). Geographic location multiplies these effects, with urban areas producing 20-50% higher comprehensive coverage costs than rural locations due to theft and accident frequency.

Coverage Structure Controls Your Budget

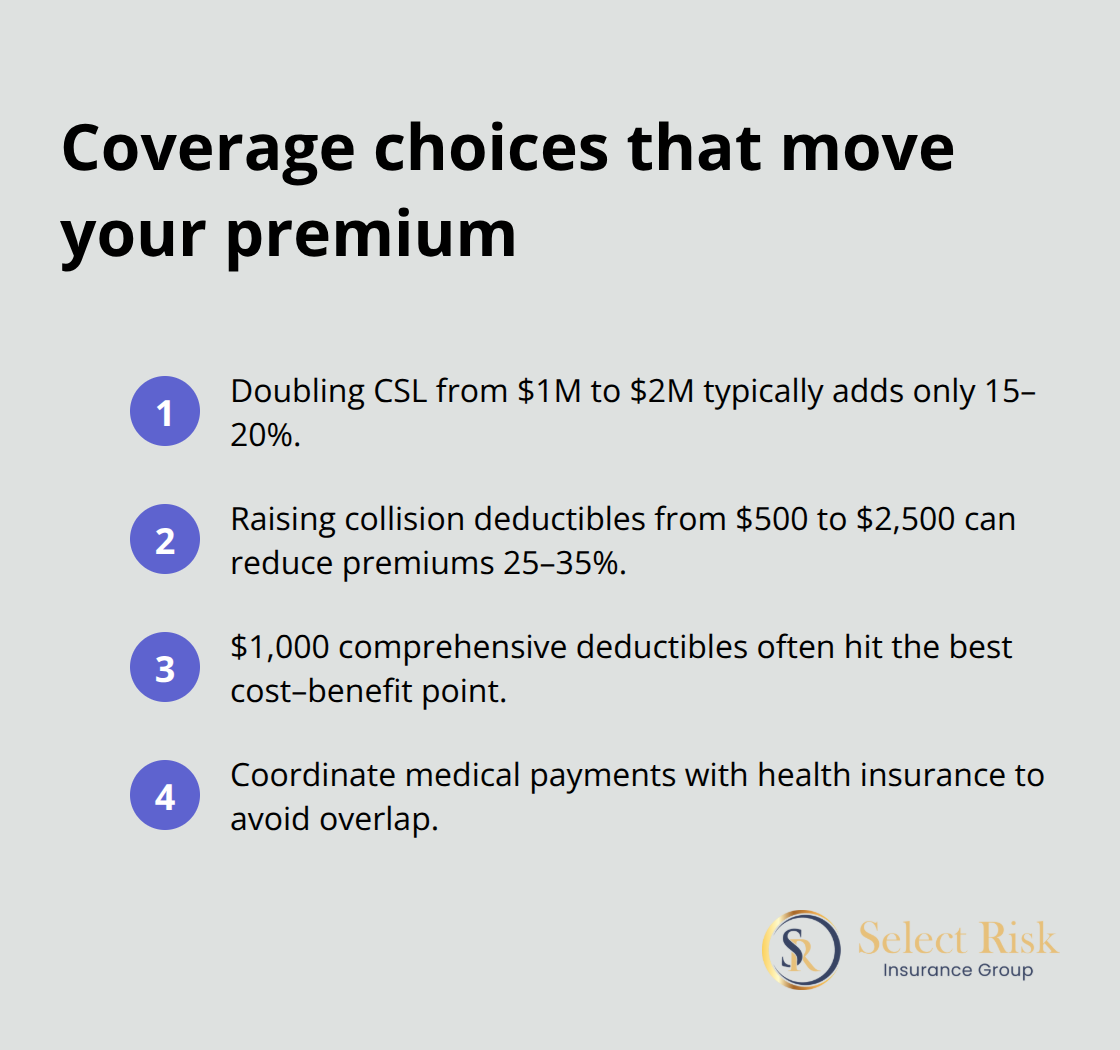

Liability limits directly correlate with premium costs, but the relationship follows predictable patterns. Increasing coverage from $1 million to $2 million Combined Single Limit typically adds only 15-20% to premiums, making higher limits cost-effective protection. Deductible selection creates immediate savings opportunities – raising collision deductibles from $500 to $2,500 reduces premiums by 25-35% annually.

Comprehensive deductibles follow similar patterns, with $1,000 deductibles offering optimal cost-benefit ratios for most commercial operations. Medical payments coverage coordination with existing health insurance prevents costly overlaps that inflate premiums unnecessarily (particularly important for businesses with comprehensive employee health plans).

Final Thoughts

Commercial auto insurance estimate calculators provide valuable budget insights that help businesses avoid costly surprises during policy shopping. These tools deliver preliminary cost ranges within 15-20% accuracy, which allows you to establish realistic insurance budgets before you contact agents. The data-driven approach helps identify major cost factors like vehicle weight, annual mileage, and operating radius that significantly impact your premiums.

However, a commercial auto insurance estimate calculator cannot replace professional consultation when your business requires specialized coverage or operates in high-risk industries. Complex fleet operations, interstate hauling, or businesses with challenging loss histories need expert analysis that generic calculators cannot provide. Professional agents access carrier-specific programs and risk management solutions that reduce costs beyond calculator capabilities.

Use your calculator results as the foundation for informed discussions with insurance professionals. We at Select Risk Insurance Group help Louisiana businesses navigate complex commercial auto insurance decisions with personalized solutions from multiple carriers (including specialized programs for high-risk operations). Contact qualified agents to transform your calculator estimates into comprehensive coverage that protects your business operations while optimizing costs through proper risk management and carrier selection strategies.