Key Underwriting Factors Affecting Your Truck Insurance Rates

Truck insurance rates vary dramatically based on specific risk factors that underwriters evaluate. We at Select Risk Insurance Group see how these truck underwriting factors directly impact premiums for commercial operators.

Understanding what insurers examine helps trucking businesses prepare better applications and potentially secure lower rates.

Driver Experience and Safety Record

Driver experience stands as the most influential factor in truck insurance underwriting. Insurers consistently reward experienced commercial drivers with lower premiums because statistics prove their reduced claim frequency. Drivers with over ten years of commercial driving experience typically receive rates 20-30% lower than newcomers to the industry. The Federal Motor Carrier Safety Administration data shows that drivers with less than two years of experience are involved in accidents at rates nearly three times higher than veteran drivers. Insurance underwriters examine not just total years behind the wheel, but specific commercial vehicle experience, CDL endorsements, and specialized training certifications.

Motor Vehicle Records Shape Premium Calculations

Your driving record extends beyond commercial violations to include personal vehicle infractions. A single DUI conviction can increase truck insurance premiums significantly, as insurers require no DUI convictions in the past 7 years for preferred rates. Moving violations within the past three years carry significant weight in underwriting decisions. Speeding tickets, following too closely, and improper lane changes signal risk to insurers. Companies with drivers who maintain clean records for five consecutive years often qualify for substantial fleet discounts. Background checks now include credit scores in many states, as research correlates poor credit with higher claim rates.

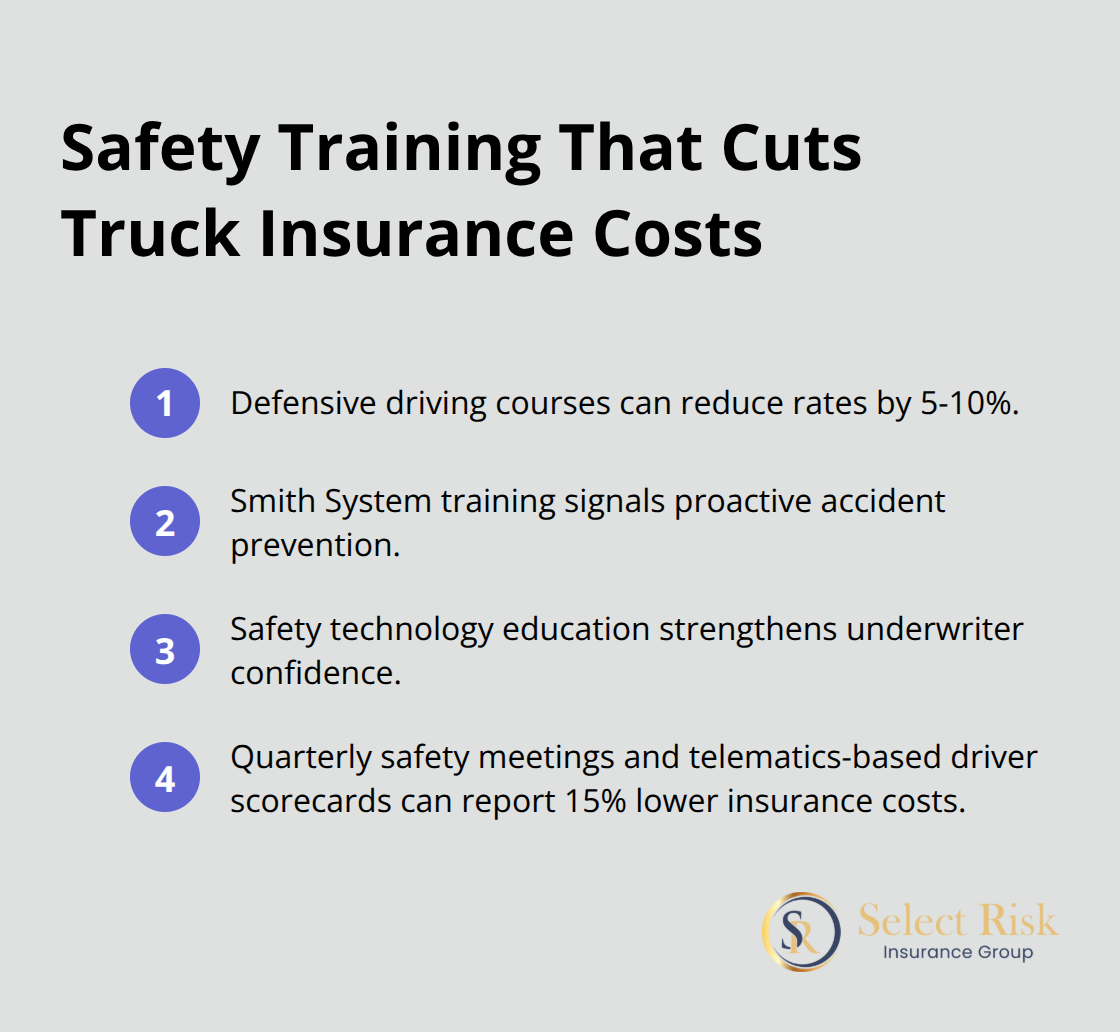

Safety Training Creates Measurable Rate Reductions

Professional safety certifications translate directly into premium savings. Drivers who complete defensive driving courses through the National Safety Council see average rate reductions of 5-10%.

Smith System training certification (recognized industry-wide) demonstrates commitment to accident prevention techniques. Electronic logging device compliance training has become mandatory, but additional safety technology education shows proactive risk management to underwriters. Companies that invest in quarterly safety meetings and driver scorecards based on telematics data report 15% lower insurance costs compared to businesses without structured safety programs.

Your truck’s physical characteristics and maintenance history form the next major category that underwriters scrutinize when they calculate your premiums.

Vehicle and Equipment Considerations

Truck age dramatically affects insurance rates, with older vehicles potentially needing more frequent repairs due to wear and tear from age. Underwriters view trucks manufactured after 2015 as significantly safer due to mandatory electronic stability control systems and improved brake technology. Freightliner Cascadia and Volvo VNL models consistently receive the lowest rates because their advanced safety systems reduce accident frequency according to Federal Motor Carrier Safety Administration crash data. Peterbilt and Kenworth trucks command premium prices but often qualify for specialized coverage programs that offset higher initial costs. Engine size matters too – trucks with engines over 500 horsepower face higher liability premiums due to increased stop distances and potential accident severity.

Safety Technology Delivers Immediate Rate Cuts

Electronic devices reduce premiums by 8-12% when paired with driver monitor systems. Forward collision warning systems cut rates by an additional 10-15% because they prevent a significant portion of rear-end collisions based on Insurance Institute for Highway Safety studies. Lane departure warning technology offers 5-8% discounts, while adaptive cruise control provides another 3-5% reduction. Dash cameras with GPS tracking create the strongest impact (reducing premiums by 15-20%) while providing legal protection during claims. Telematics systems that monitor harsh braking, rapid acceleration, and speeding patterns allow insurers to offer usage-based pricing that rewards safe driving behaviors in real-time.

Maintenance Records Prove Operational Excellence

Documented maintenance schedules directly influence underwriting decisions, with companies that maintain detailed service records receiving 10-15% rate reductions. Pre-trip inspection logs demonstrate proactive safety management to insurers, while roadside breakdown frequency correlates strongly with accident rates. Trucks with annual Department of Transportation inspections that show zero violations qualify for additional discounts. Regular tire replacement records indicate proper load management, reducing liability exposure for blowout-related accidents that can be costly for insurers. Refrigerated truck operators face additional equipment breakdown risks that require specialized coverage considerations.

The cargo you haul and where you operate create the next layer of risk assessment that underwriters examine when they calculate your insurance costs.

Business Operations and Risk Assessment

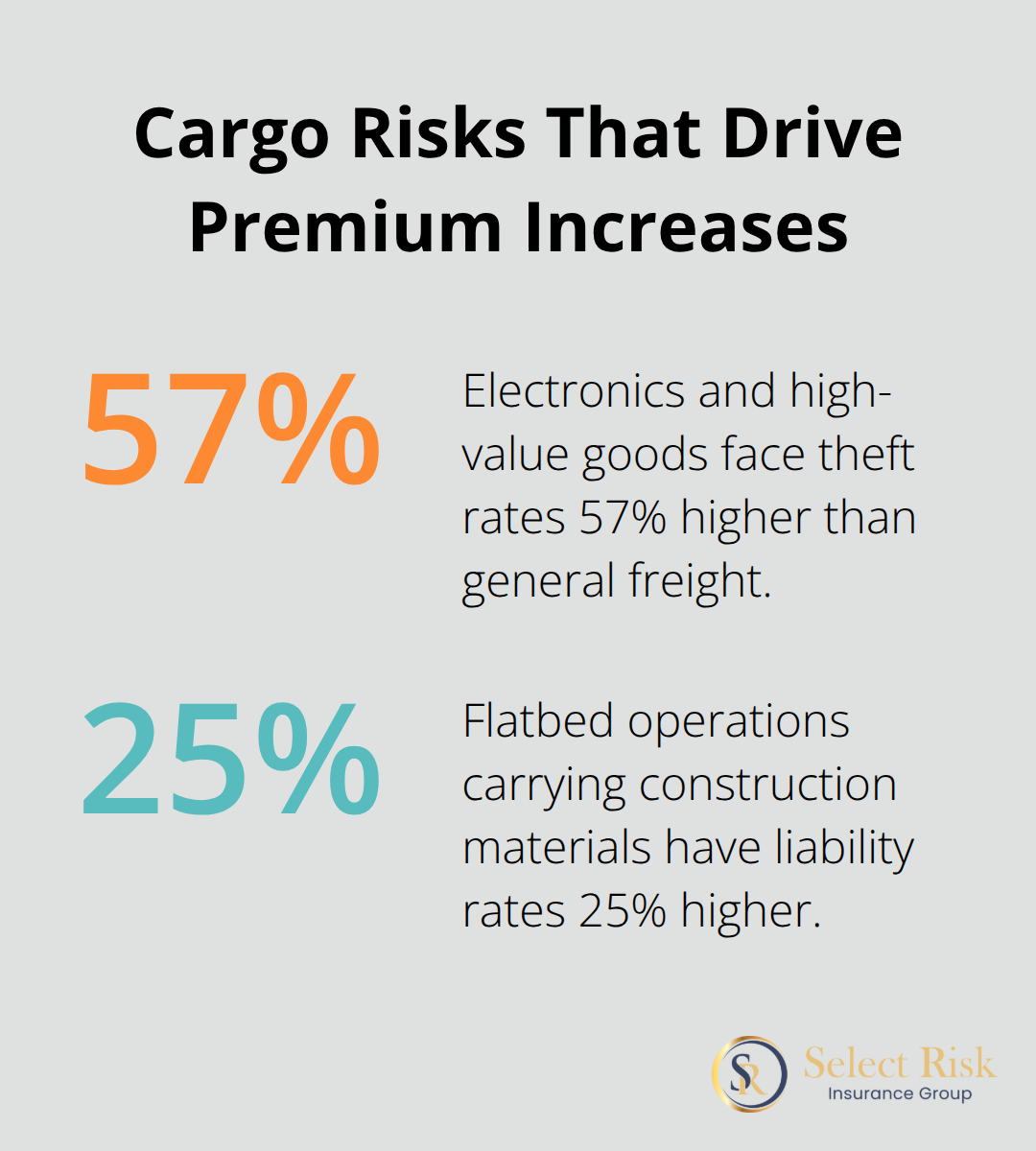

Cargo type creates the largest premium variations in truck insurance, with hazardous materials carriers seeing significant rate increases due to specialized risk factors. Electronics and high-value consumer goods face theft rates 57% higher than general freight, which forces insurers to increase cargo coverage premiums accordingly. Food and beverage transport requires specialized temperature-controlled equipment that increases breakdown risks, while automotive parts transport involves strict delivery schedules that pressure drivers toward unsafe behaviors.

Flatbed operations that carry construction materials face 25% higher liability rates due to load securement challenges and object risks that Federal Motor Carrier Safety Administration statistics link to increased accident severity.

Geographic Routes Determine Risk Exposure Levels

Interstate operations across multiple states carry premiums 15-20% higher than intrastate operations due to different state regulations and increased exposure time. Urban routes through cities like Los Angeles, Chicago, and New York command rate increases of 30-40% because traffic density creates higher accident frequencies. Weather-prone corridors (including Interstate 80 through Wyoming and Interstate 10 through Texas during hurricane season) face seasonal surcharges of 10-15%. Cross-border operations into Mexico require specialized coverage that doubles standard liability premiums, while Canadian operations need additional medical payment coverage that increases costs by 8-12%. Companies that limit operations to rural highways in low-crime areas achieve the lowest geographic risk ratings from underwriters.

Annual Mileage Patterns Shape Premium Calculations

Trucks that log over 100,000 miles annually face rate increases of 20-25% compared to regional operations under 50,000 miles because exposure time directly correlates with claim frequency. Weekend and night operations carry 15% surcharges due to reduced visibility and higher fatigue risks that Insurance Institute for Highway Safety research connects to accident rates. Seasonal operations like agricultural transport during harvest periods create concentrated risk exposure that requires specialized coverage adjustments. Owner-operators who lease to multiple carriers throughout the year face higher rates than single-contract haulers because inconsistent safety oversight increases underwriter concerns about operational control and driver supervision standards.

Claims History Impact on Future Rates

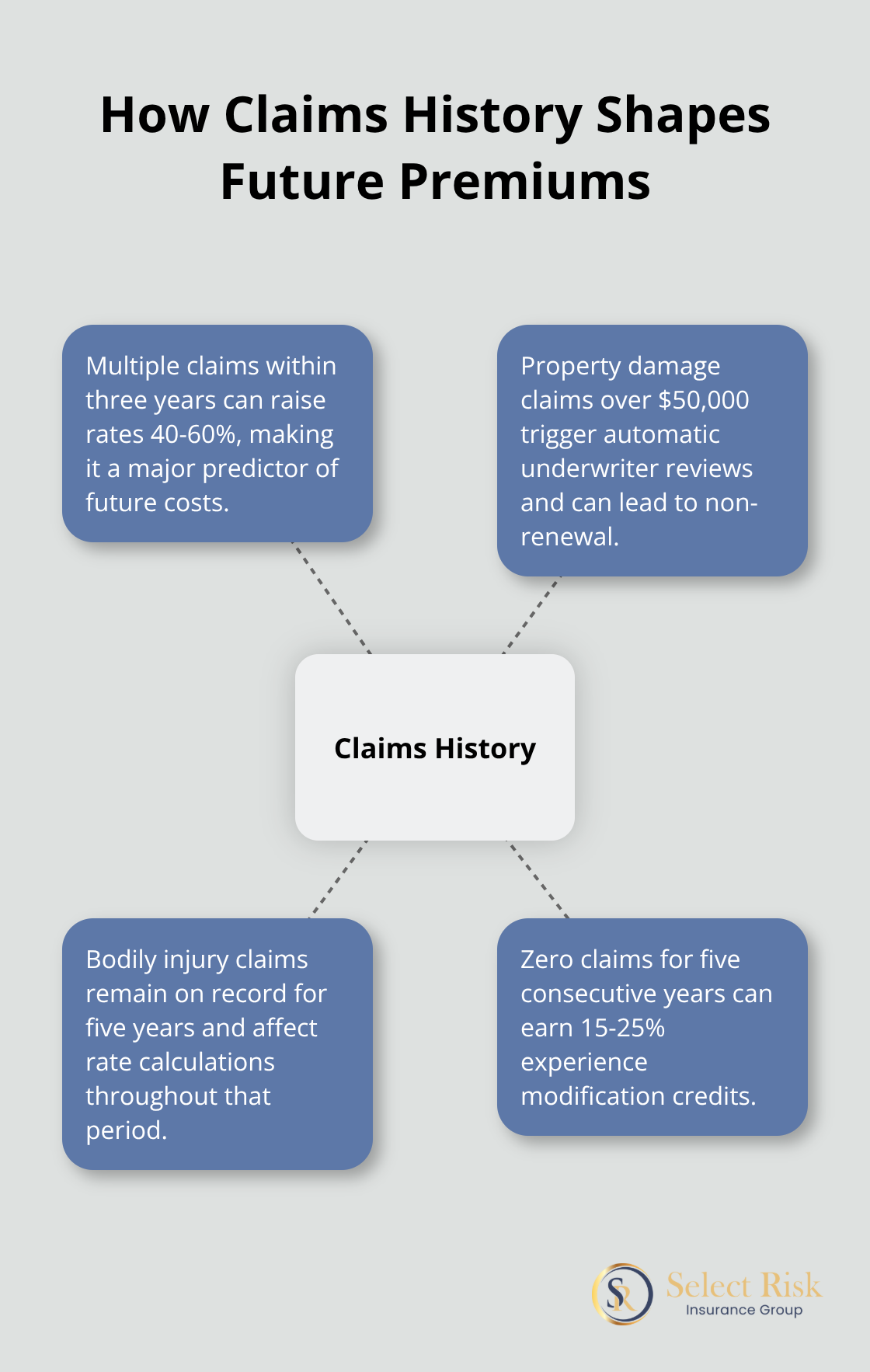

Previous claims create the strongest predictor of future insurance costs, with companies that file multiple claims within three years facing rate increases of 40-60%. Property damage claims over $50,000 trigger automatic underwriter reviews that can result in policy non-renewal or substantial premium increases. Bodily injury claims (regardless of fault determination) remain on insurance records for five years and influence rate calculations throughout that period.

Companies with zero claims for consecutive five-year periods qualify for substantial experience modification credits that reduce premiums by 15-25% below standard rates, making it essential to understand commercial auto insurance costs when planning your coverage strategy.

Final Thoughts

Truck underwriting factors create significant premium variations across the commercial transportation industry. Driver experience remains the strongest rate determinant, with veteran operators achieving 20-30% lower costs than newcomers. Vehicle age and safety technology installations deliver immediate discounts of 8-20%, while maintenance documentation proves operational excellence to underwriters.

Cargo type and geographic operations shape risk profiles dramatically. Hazardous materials and high-value electronics face substantial rate increases, while interstate operations cost 15-20% more than local routes. Annual mileage over 100,000 triggers additional surcharges, and claims history impacts rates for five years (with effects lasting throughout that entire period).

Smart trucking businesses focus on driver training, vehicle maintenance, and safety technology investments to improve their insurance profiles. Clean driving records, documented maintenance schedules, and zero claims periods create the strongest foundation for competitive rates. We at Select Risk Insurance Group help Louisiana trucking companies navigate these complex underwriting factors to secure optimal coverage at competitive rates.